The BOJ's Stock Market Distortions Are Coming Under New Scrutiny

The BOJ’s Stock Market Distortions Are Coming Under New Scrutiny

(Bloomberg) -- The Bank of Japan, sometimes dubbed the Tokyo whale for its huge influence on the country’s stock market, may be about to change its habits because it’s taking up too much of the pool.

That’s the speculation after local press reported that the central bank is considering changing how it buys shares through its exchanged-traded fund program. At its two-day meeting starting Monday, Haruhiko Kuroda’s BOJ will discuss reducing investments in ETFs tracking the Nikkei 225 Stock Average, the old blue-chip gauge, because its purchases are having an outsized impact on its companies, the Nikkei newspaper reported last week. Instead, it will buy more funds tracking the broader Topix index, it said.

If the bank decides to take that step, it’s bad news for the share prices of firms such as Fast Retailing Co., the clothing giant run by Tadashi Yanai, as well as for SoftBank Group Corp. and Fanuc Corp. Those three companies have the heaviest weightings in the Nikkei 225. Fast Retailing’s shares, for example, tumbled 8 percent last week on the news, the worst weekly decline since February, and dragged down the Nikkei 225. Where once the company and the index rode high on the BOJ’s largesse, now they’re already experiencing withdrawal symptoms. The Nikkei 225 fell 0.7 percent at the close on Monday and Topix slipped 0.4 percent.

“I have always been bitterly critical of the BOJ buying of Nikkei ETFs,” Nicholas Smith, a strategist at CLSA Ltd. in Tokyo said in an interview. In the Nikkei 225, ranking is determined by the arbitrary measure of the price of one share, unlike most share indexes, where market capitalization is key. “Buying of it is hugely distortive.”

The Bank of Japan, which aims to spend 6 trillion yen ($54 billion) a year on ETFs as part of its stimulus program, owned 3.8 percent of the Japanese stock market as of May 28, according to estimates by Nomura Holdings Inc. The bank holds stakes of more than 10 percent in 27 companies, according to the brokerage, including 19 percent of Advantest Corp., 17 percent of Fast Retailing and 16 percent of TDK Corp.

The central bank’s influence is especially large for companies in the Nikkei 225 that have fewer freely tradable shares, such as Fast Retailing where the billionaire Yanai owns 22 percent, according to CLSA’s Smith. He even asks whether Nikkei Inc. will consider changing the way it calculates the stock gauge to alleviate this issue.

“It is still continuing to have a disproportionate impact on stocks with small floats and low liquidity,” Smith wrote in a note published Jul. 23. “The question is whether this will force a change in the way Nikkei constructs its index.”

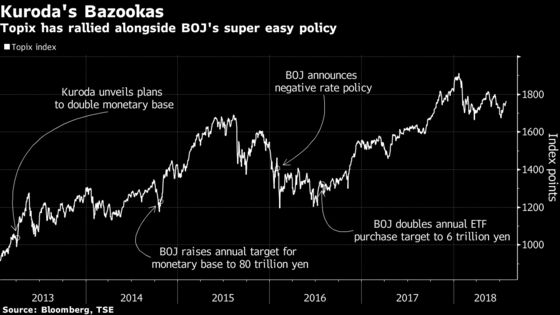

The Bank of Japan has already diverted its stock purchases away from the Nikkei 225 once before. In September 2016, shortly after doubling its annual ETF purchase target, the BOJ said it would purchase fewer Nikkei ETFs and more tracking the Topix. But even with the tilt away from Nikkei-linked funds, the issue seems to be persisting.

Now, “shares with higher weighting in Nikkei 225 -- such as Fast Retailing, SoftBank and Fanuc -- are coming under selling pressure,” said Tomoichiro Kubota, an analyst at Matsui Securities Co. in Tokyo. “But as long as the BOJ keeps the annual amount of ETF purchases unchanged, the overall impact on the market will be limited.”

“There is a good chance that the BOJ could introduce some small, technical tweaks at this meeting,” Bank of America Merrill Lynch analysts led by Izumi Devalier said in a report dated July 27. The central bank could rebalance its ETF purchases from the Nikkei 225 to Topix and change its JGB bond-buying operations “such as widening offer size ranges for its bond purchases and ending the disclosure of bond-buying operation dates.”

While speculation is swirling that the BOJ will tweak its ETF program or allow the 10-year bond yield more scope to move beyond zero percent, most investors expect no big policy changes at the meeting. In that, they’re aligned with economists in a recent Bloomberg survey, all 44 of whom predicted no major change to the bank’s settings for its yield-curve control and asset purchase programs.

“Obviously there are discussions taking place within the BOJ and there are concerns about the side effects of some of the policies, but I don’t personally think that there will be a change this week,” said Jonathan Allum, a strategist at SMBC Nikko Capital Markets Ltd. in London. “I’m not sure that we’re really in the stage of any great change here.”

But on the off chance that the BOJ does signal a shift in policy towards tapering, analysts say the market is bound to take it badly. That would be further bad news for a stock market that has already been sputtering for most of 2018. The benchmark Topix index is down more than 7 percent from a high in January, with foreign investors selling a net 3.8 trillion yen ($34.4 billion) in the country’s stocks in the first half.

The negative impact "could last longer than expected as the policy is the most relaxed easing policy in history," said Hideyuki Suzuki, a general manager at SBI Securities Co. in Tokyo. "There are concerns over whether Japan can handle it as well as the U.S."

And that wouldn’t be the only problem, according to Mikio Kumada, Hong Kong based global strategist at LGT Capital Partners, who said the negative impact on equities would be long-lasting.

"It would also undermine the credibility of the BOJ," Kumada said. "The next time we have a recession, or depression or deflation or some kind of Lehman shock, and the BOJ comes out and says, ‘Oh, we’re going to aim at 2 percent inflation,’ nobody is going to believe them if they start withdrawing now."

--With assistance from Keiko Ujikane and Naoto Hosoda.

To contact the reporters on this story: Min Jeong Lee in Tokyo at mlee754@bloomberg.net;Shiho Takezawa in Tokyo at stakezawa1@bloomberg.net;Abhishek Vishnoi in Singapore at avishnoi4@bloomberg.net;Toshiro Hasegawa in Tokyo at thasegawa6@bloomberg.net

To contact the editors responsible for this story: Divya Balji at dbalji1@bloomberg.net, Tom Redmond

©2018 Bloomberg L.P.