The Auto Industry Is Overdue a Bout of Mega-Mergers

The sector desperately needs to consolidate, reduce ruinous levels of competition. By some metrics, takeover targets look cheap.

.jpg?auto=format%2Ccompress&w=200)

(Bloomberg Opinion) -- Love is in the air again among the world’s automotive manufacturers.

The alliance of Renault SA, Nissan Motor Co. and Mitsubishi Motors Corp. aims to restart merger talks in 12 months before moving on to a takeover of Fiat Chrysler Automobiles NV, the Financial Times reported last week. Peugeot-owner PSA Group is also looking to build a partnership with Fiat Chrysler. Nissan Chief Executive Officer Hiroto Saikawa told the deposed alliance chairman Carlos Ghosn in an email last year that he’d been looking at bringing in a fourth manufacturer to the partnership, Bloomberg News’s Ania Nussbaum and Jie Ma reported Monday.

For all the ambition behind such mega-deals, the fissiparous nationalist politics that have plagued the Renault-Nissan relationship seem more likely to win out, as my colleagues Chris Bryant and Anjani Trivedi wrote last week. So why all the desperation to merge?

One underappreciated reason is that the car industry has become dangerously competitive.

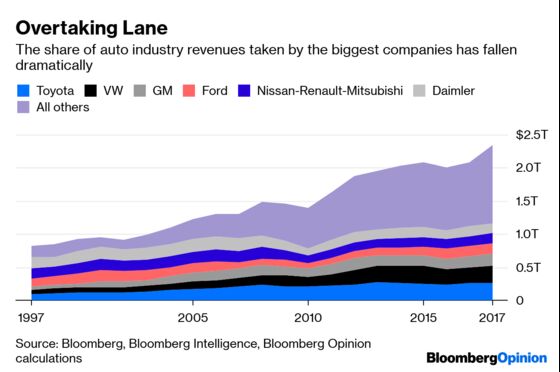

Thanks to the decline of Detroit’s giants, the rise of China’s state-owned joint-venture partners, and the burgeoning success of mid-size car companies, the market share of the top four automotive companies has dropped precipitously over the past two decades. At the turn of the century, those firms accounted for more than two-thirds of industry revenue (levels over 50 percent are typically considered oligopolistic). In 2017, that had fallen to little more than one-third.

Of course, automotive sales are local even if companies are global. Toyota Motor Corp. may only have about 11 percent of global revenue, but it accounts for almost half of unit sales in its home market. Volkswagen AG, the biggest carmaker by worldwide deliveries, sells fewer cars under its own marque in the U.S. than minnows like Kia Motors Corp. or Subaru Corp. A core strategy of General Motors Co. Chief Executive Officer Mary Barra has been to retreat back to the company’s U.S. market by shedding less-profitable overseas units, some of which had been held for nearly a century.

At the same time, carmakers are in a global fight for supremacy – one reason that figures like Ghosn have been such evangelists for a world of pooled manufacturing platforms and modular designs that can minimize the ferocious costs of developing new vehicles. That’s especially crucial in the face of the triple threat from electric vehicles, autonomous driving and shared mobility.

The risks of duplicating capital and research & development expenditure in that environment can be brutal. At BMW AG, Volkswagen and Tata Motors Ltd.’s Jaguar Land Rover, R&D costs have risen to 6 percent or more of sales in recent years, producing some impressive innovations but cutting dangerously deep into profitability.

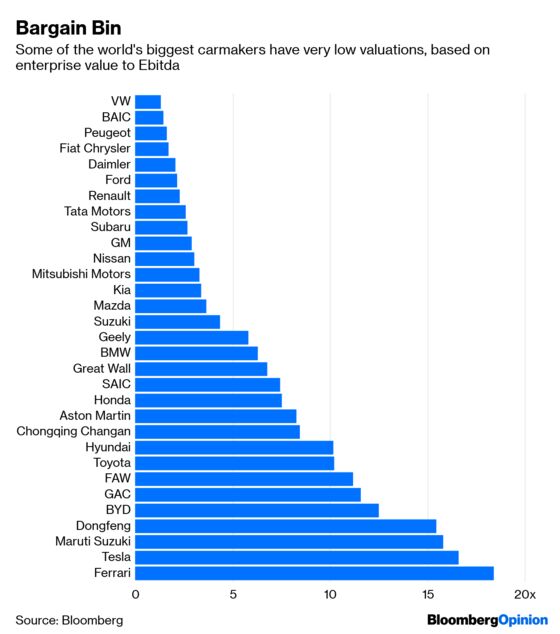

As a result, investors are disenchanted with the industry’s prospects: The equity and debt of PSA, Fiat Chrysler, and Volkswagen could be bought for less than two years of their forecast Ebitda. By comparison, even in its current fallen state Facebook Inc. could be bought for 11.5 times Ebitda.

The flip side of those valuations and the current low cost of debt is that, by traditional metrics, it’s phenomenally cheap to buy a carmaker if you’re prepared to pay cash.

Even before assuming synergies, Nissan could buy Renault at a 70 percent premium and still double its earnings per share by 14 percent in the first year, based on Bloomberg’s merger calculator. Daimler could pay a 30 percent premium for BMW shares and get a deal that was 70 percent accretive. Ford could buy Subaru at the same premium and watch earnings rise by 30 percent in the first year.

Of course, companies don’t take over their rivals just because they’re cheap. If investors hold a dim view of a stock’s prospects, potential acquirers may make the same calculation. What’s different right now, though, is that the industry desperately needs to consolidate and reduce the current ruinous levels of competition. Getting even bigger doesn’t seem such a bad way of bringing about that future.

It’s not clear that this necessary process can easily happen. As we’ve seen with the Renault-Nissan saga, the Trump administration’s automotive tariff proposals, and Daimler’s lukewarm response to an investment from Geely Automobile Holdings Ltd.’s parent, the global car industry seems to be getting more, not less nationalist. Things are likely to get worse before they get better.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.