Traders' Favorite Villains Deserve a Big Thank You

(Bloomberg Opinion) -- So-called soft landings, the idea that economies can lose altitude without going into a slump, are often hoped for – and devilishly hard to pull off. This one has a fighting chance for two reasons: Central banks took prompt action, and things probably weren’t all that bad to begin with.

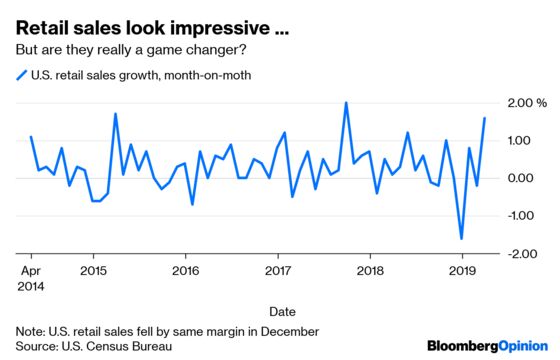

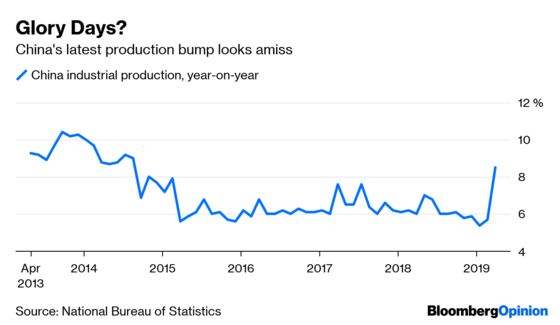

Numbers in the past week have given succor to optimists. Retails sales in the U.S. jumped the most last month since September 2017, while first-time claims for unemployment benefits fell to a fresh 49-year low. A slew of Chinese data suggested government stimulus had arrested a slide in activity around year-end. Australia, a country sensitive to economic fluctuations in China, is even seeing some vitality in its labor market.

A dovish turn from the big central banks played a critical role in the turnaround. The Federal Reserve paused its interest-rate hikes abruptly and sent pretty clear signals it’s not going to restart them soon. The European Central Bank flirted with stimulus; the Bank of Japan sounds more likely to ease than not; and China began loosening the reins long before the Fed did.

Monetary mandarins are everyone’s favorite target when things go awry. Yet they also get flak for being behind the curve or too reticent to withdraw accommodation when times are good. As often as prognosticators skewer central banks for distorting the market, they just as quickly turn around and finger them for failing to listen. Monetary policy has become a first-line defense. Often the second, and third, too. In this instance, the rescuers may have arrived at a scene they never fully departed.

The latest good news should be a lesson to those arbiters of sentiment who break into sweat if gross domestic product varies from consensus forecasts by one-tenth of a percent or so. Too many analysts seem blinded by the scale of the last global recession: In fact, the next downturn may be a moderate one, such as the 2001 trough that people barely remember.

That doesn’t mean some caution isn’t warranted. Some of the exuberance surrounding the Chinese data released last Wednesday was misplaced. If things were so great, Chinese officials wouldn't be discussing further steps to spur demand. Another cut in bank reserve requirements is possible, as is a series of measures to jolt sales of cars and electronics.

Similarly, we shouldn’t be blinded by perkiness in American numbers or assume the Fed's next move will be a resumption of hikes. Top officials have been clear the benchmark rate isn't budging soon. If the economy is doing okay, but not brilliantly – as appears to be the case – and inflation still fails to fire, policymakers may actually trim borrowing costs. That would show the Fed is as worried about undershooting its 2 percent target as overshooting it, and would be a handy bit of insurance to safeguard the long expansion.

We’re coming up on 10 years of that expansion in the U.S., and even the most pessimistic of forecasts have China growing, albeit slowly, for decades into the future. Japan and Europe have skirted around the edges of recession; still, both have central banks armed and ready to prevent the worst.

History students looking at this can’t help but expect the next shoe to drop. Yet it’s entirely possible that it won’t. The next phase of the global economy could simply be a long, unspectacular trudge up a mild incline. That may be the best we can ask for.

To contact the editor responsible for this story: Nisid Hajari at nhajari@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2019 Bloomberg L.P.