(Bloomberg Opinion) -- Standard Chartered Plc’s largest stockholder is unhappy.

While a share repurchase, which may be announced as early as next month, could buy some time, Temasek Holdings Pte won’t be satisfied for too long with a lollipop. Rather, the Singaporean state-owned investor is looking for a more substantial meal: double-digit returns on equity.

Alas, that goal continues to elude CEO Bill Winters. Even after nearly four years of trying to restore the firm to health, StanChart’s return on equity is 6.6 percent. The bank’s stock has fallen 43 percent since Temasek bought a stake in July 2006. Something else – or someone else – is needed to make the company relevant again as a specialist emerging-markets lender.

Temasek, with a roughly 16 percent stake in the London-headquartered bank, is frustrated with the slow pace of turnaround, according to the Financial Times, which said the investor has considered taking a seat on the board. The Singaporeans would prefer someone like Piyush Gupta, CEO of DBS Group Holdings Ltd., ultimately to succeed Winters, the FT added, saying that Temasek isn’t terribly impressed by internal candidates being considered.

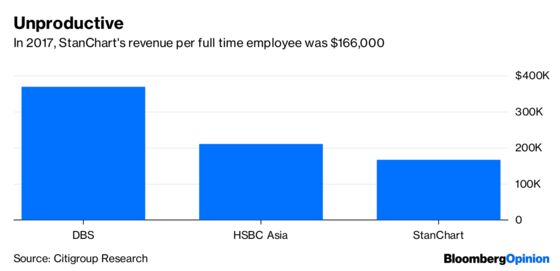

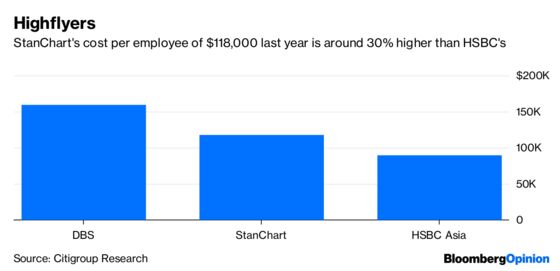

Taking a board seat or sending Gupta over to troubleshoot may not be enough to change StanChart’s culture, which is where its problems lie. StanChart remains a bloated remnant of the British empire with too many employees littered around too many countries (still at 60). At its peak employee count in 2014, before its corporate loan book in India and Indonesia blew up, StanChart had almost 91,000 bankers. Five years later, it has 86,000. If only they were as productive as they are numerous: DBS’s revenue per employee is more than double that of StanChart, according to Citigroup Inc. analyst Ronit Ghose, while costs are only 30 percent more.

The FT reported in October that a fresh round of job cuts is being prepared in Africa and the Middle East, where operating income slumped in the third quarter. A more dramatic shrinkage is needed, perhaps by selling business lines, getting out of unappetizing markets, or laying off overly expensive staff. (StanChart has 3,800 full-time employees in high-cost London, and its salaries in Southeast Asia are well above local rivals’.)

HSBC Holdings Plc has shed more than 85,000 workers since the 2008 financial crisis, and yet it comfortably leads StanChart in Hong Kong, the most important market for both. With the city’s red-hot property prices starting to come off their peaks, lenders’ loan growth is flagging, putting StanChart in a worse position than its bigger rival. The impending arrival of virtual banks in Hong Kong could also spice up competition for deposits.

Bringing in Gupta still makes more sense than promoting an insider who’ll have more of an interest in perpetuating a frustrating matrix of reporting relationships and the slothful bureaucracy of Peter Sands, Winters’s predecessor. Gupta’s digital push, which has paid dividends for Singapore’s biggest lender, would also be welcome at StanChart.

But having presided over consistent growth, can the DBS executive cut a bank to size? After all, Winters, was also an outsider. As a former co-head of investment banking at JPMorgan Chase & Co., he’s no stranger to cutbacks. If someone as well-liked and steadfast as him can’t right the ship, then why should Gupta be any more successful?

Beyond making the bank more efficient, and shaking off large regulatory fines for past indiscretions, StanChart needs to streamline its franchise and simplify its unwieldy structure. Its corporate banking business is quite healthy, and it has strength in cash management, despite tough competition from HSBC and Citigroup. Yet in wealth management, competing in Asia against UBS Group AG and Credit Suisse Group AG – and increasingly the Singaporean banks – seems like a lost cause.

If cost cuts don’t soup up returns, a merger with a superior franchise, one whose shares trade at a more respectable price-to-book value than StanChart’s 0.6 times, may be inevitable. Yet few partners will be happy to tie up with a bank whose employees aren't high on the productivity scales. Temasek is unlikely to attempt a merger of DBS and StanChart; that would bring more disparate risk from around the world to the small city-state than its regulator would tolerate.

StanChart may be “here for good,” as its advertising tagline suggests. Temasek’s question for Winters may be whether his 86,000 bankers are here for good, too.

Some of the increase in the bank's employee count was much-needed compliance staff.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2019 Bloomberg L.P.