Sydney's Property Plunge Will Be the Central Bank's Biggest Worry

The worst scenario for policy makers would be a multi-year property downturn in Sydney and Melbourne along with stagnant wages.

(Bloomberg) -- Sydney’s plunging house prices are usurping a prolonged wage slump as the key worry for the central bank, with markets now showing more chance of an interest-rate cut than a hike in 2019.

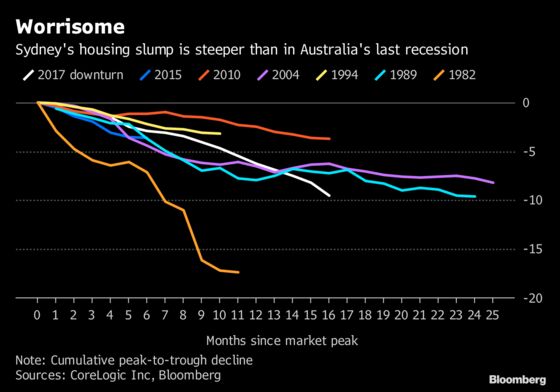

Prices in Australia’s biggest city have tumbled 10 percent and some economists are tipping a similar fall next year. While the central bank isn’t panicking just yet, a 15 percent nationwide drop in prices would cut about A$1 trillion ($720 billion) from the housing stock value. That could deal a major blow to consumption, which props up about 60 percent of the economy.

The wages picture isn’t much brighter than property’s, though the RBA and government say labor shortfalls are emerging in some industries. Pay packets rose 2.3 percent last quarter, a three-year high and inching closer to Governor Philip Lowe’s goal of annual increases with a “3” in front of them. But a reasonable amount of slack remains in the labor market.

In minutes of its last board meeting released Tuesday, the Reserve Bank warned of a trifecta of risks that could disrupt household spending: low growth in household income, high debt levels and declining house prices.

“Since 2016, the RBA’s focus on financial stability has held them back from further rate cuts as they wait for wages and inflation to recover,” said Daniel Blake, a strategist at Morgan Stanley in Sydney, who expects nationwide house prices to drop 10 to 15 percent. “In 2019, we see their focus turning to monitoring the negative wealth effects from a housing market adjustment.”

The housing slump could take some time to unwind. Historically, corrections have been triggered by very tight policy; the cash rate went above 17 percent in the pre-recession downturn, whereas now it’s 1.5 percent. With no scope for deep rate cuts to draw buyers back to the market, and prices still at astronomical levels, it could take some time for affordability to return.

Yet at the same time, the economy is still growing just above its speed limit and the jobless rate is at 5 percent, the lowest in more than six years. Lowe said he suspects unemployment could fall to 4.5 percent without seeing rapid wage growth. With inflation low, the economy is in a relatively healthy position.

“This is to some extent uncharted territory to see this sort of dynamic play out in an environment where -- as of now at least -- the macro economy is traveling at a reasonable place,” RBA No. 2 Guy Debelle said earlier this month. “Nearly all other house price falls have occurred in environments where there’s been recessions and the like.”

The RBA would ideally like to see household incomes start to enjoy a strong, sustainable increase to help the property market find a bottom quicker, and for that to flow through to faster inflation. Such a smooth transition would set the scene for the first rate increase since 2010, but it’s also pretty unlikely.

In a sign that authorities are trying to encourage buyers back into the market, the country’s prudential regulator announced Wednesday that it was removing restrictions on interest-only loans. These are primarily used by investors who have been blamed for crowding out younger buyers from the housing market.

The worst case scenario for policy makers would be a multi-year property downturn in Sydney and Melbourne -- the second-largest city -- along with stagnant wages. That, together with a slowdown in global growth, could force the RBA to deploy its remaining ammunition and push rates toward zero.

Money markets were pricing in a 12 percent chance of a rate cut in the next year as of 4:30 p.m. in Sydney on Wednesday. There was about a 24 percent possibility of a hike by the end of 2020.

To contact the reporter on this story: Michael Heath in Sydney at mheath1@bloomberg.net

To contact the editors responsible for this story: Nasreen Seria at nseria@bloomberg.net, Chris Bourke

©2018 Bloomberg L.P.