Sydney Home Bubble Deflates as Loans Revisit 2008 Losing Streak

Australia’s east-coast property bubble is showing signs of deflating at a faster clip

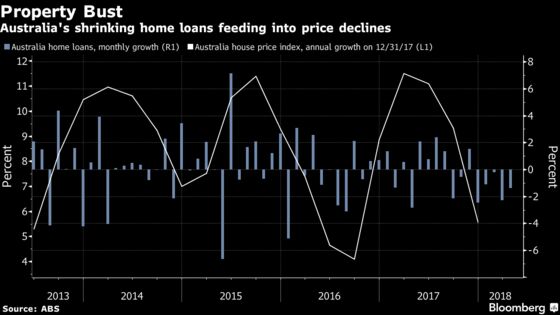

(Bloomberg) -- Australia’s east-coast property bubble is showing signs of deflating at a faster clip as home-lending data recorded the longest losing streak in almost a decade.

Housing finance fell 1.4 percent in April, the fifth straight monthly drop and the longest stretch of declines since September 2008, when Lehman Brothers Inc. collapsed and a month before the Reserve Bank of Australia slashed its key interest rate by a percentage point.

The downturn is most prominent in Sydney where prices slid 4.2 percent in May from a year earlier, when they were rising at an annual pace of 17 percent. Sales at auctions -- a popular way of marketing houses Down Under - have slumped to the lowest since early 2016 in Australia’s biggest city, with only around half of properties successfully selling.

A key factor weighing on Sydney’s market is tighter credit, as regulators force banks to cut back on the riskiest mortgages. Fewer interest-only loans -- which are cheaper in the early years because borrowers don’t repay principal -- means Sydney prices are now out of reach for many investors. Chinese buyers, a previous driver of demand, have also receded due to difficulties in moving cash from the mainland.

For Australian borrowers, there’s little prospect of relief for household income as wage growth has stagnated for the past five years. The economy’s private debt-to-income ratio is also at a record 189 percent, leaving little scope to increase leverage anyway.

Meanwhile, high-income owner-occupiers have less borrowing power due to tighter checks on their real spending levels as part of the mortgage approval process. Previously they could rely on benchmarks that were unrealistically low.

Market bulls point to Australia’s population growth and record-low interest rates -- unchanged at 1.5 percent for almost two years -- as reasons to expect a soft landing in the property market. Others suggest the current downturn is only just getting started, noting the decline after 2003 lasted for more than two years.

For the central bank, a gradual grind down in prices would be helpful in bolstering financial stability, particularly if it doesn’t hit households’ perception of their wealth too hard.

--With assistance from Kimberley Verschuur.

To contact the reporters on this story: Michael Heath in Sydney at mheath1@bloomberg.net;Garfield Reynolds in Sydney at greynolds1@bloomberg.net

To contact the editors responsible for this story: Nasreen Seria at nseria@bloomberg.net, Chris Bourke, Peter Vercoe

©2018 Bloomberg L.P.