Sweden Rebuts Summers After His Critique of Negative Rates

Summers Is Rebutted in Sweden After Criticizing Negative Rates

(Bloomberg) -- Sweden’s central bank has rejected the findings in a study co-authored by former U.S. Treasury Secretary Lawrence Summers that criticized negative interest rates.

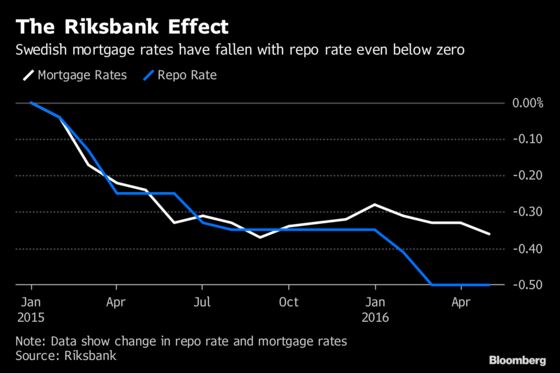

Riksbank First Deputy Governor Kerstin af Jochnick says the study is looking at the wrong data. Based on that data, it drew the conclusion that negative rates are harmful to an economy, because they hurt bank profits and impede lending growth. The review even used Sweden as an example.

But the authors should have looked at actual lending rates in the mortgage market, not listed rates, af Jochnick said in an interview in Stockholm.

“We don’t share the study’s conclusions that mortgage rates haven’t followed the repo rate down,” she said. “We’re almost surprised by how well mortgage rates -- not right away when we change, but over time -- have come down in line with the repo rate.”

The jury is still out on the extent to which negative rates have proved a successful approach to dealing with the economic shock that hit much of the world following the global financial crisis of 2008. Sweden, Switzerland, Japan, Denmark and the euro zone all tested the policy, though their monetary goals varied between galvanizing demand to steering exchange rates.

Sweden’s Riksbank drove its benchmark repo rate below zero in 2015 to avoid deflation, and only last month started tightening policy. Like other central banks, it also bought up large quantities of bonds, drawing criticism it was distorting market prices.

The European Central Bank and International Monetary Fund have also drawn similar conclusions to the Riksbank about the effects of negative rates.

Summers, along with Brown University’s Gauti Eggertsson and Ella Getz Wold, as well as Norges Bank’s Ragnar Juelsrud, said in their paper that because negative central-bank rates aren’t transmitted to overall deposit rates, a model suggests that they are “at best irrelevant, but could potentially be contractionary due to a negative effect on bank profits.”

The study pointed to bank level data that suggested a policy rate of minus 0.5 percent increases borrowing rates by 0.15 percent and reduces output by 0.07 percent.

The Riksbank responded by releasing a table to rebut that assertion. “There are different channels in monetary policy, but when it comes to the study, our assessment is that they’ve probably used data that doesn’t really give a fair representation in their analysis,” af Jochnick said.

Af Jochnick said it’s important to remember that “the rate isn’t just meant to affect the banks’ interest rates. It should also affect developments in the Swedish economy and make sure that inflation remains 2 percent.”

In a response to the Riksbank’s argument, Eggertsson, Getz Wold and Juelsrud said it was important to note that their paper only looks at the transmission through the banking sector, and we “don’t rule out that negative rates have expansionary effects working though other channels.”

Summers made a similar point in a brief telephone interview. “We were careful to state that our analysis considered the banking channel and not other possible channels through which negative interest rates may have benefited the Swedish economy,” the Harvard University professor said.

Eggertsson, Getz Wold and Juelsrud said that they used listed rates since actual bank level rates were unavailable and that there’s usually a close match.

“The assumption is that the relationship between listed and actual rates didn’t change dramatically once the Riksbank went negative,” they said in an email to Bloomberg. “It’s unclear why that would be the case, and it’s indeed surprising and interesting if the Riksbank has uncovered new evidence to the contrary. We encourage them to make those findings public so they can be independently confirmed by other researchers.”

While saying he also looked forward to examining the Riksbank data, Summers said, “there’s no particular reason to expect that the relationship between transactions prices and listed prices would have changed during the negative interest-rate period.”

“I am surprised by this line of criticism,” he added. “Gauti Eggertsson, my co-author, presented the paper at the Riksbank and he reports that these points were not suggested.”

While Eggertsson and his co-authors have released earlier versions of this research, Summers’s appearance as a co-author is new. The Harvard economist is an influential voice in monetary policy circles and has a track record of urging policy makers to contend with a low-growth, low-interest rate future.

The discussion is likely to draw attention in the U.S., where the Federal Reserve is embarking on a conversation about its framework. The Fed has never resorted to negative rates, but research from Fed Board economists shows that its key rate could be around zero about a third of the time going forward. That means that unconventional monetary policies are likely to become part of the toolkit. It’s worth noting, though, that Fed staff looked at negative rates back in 2010 and were unsure whether the central bank had the legal authority to impose them.

“With secular stagnation and declines in neutral interest rates, the issue of negative interest rates is likely to be important in the future and warrant more research and debate,” Summers said in the telephone interview.

In their paper, Summers and his co-authors point to quantitative easing, forward guidance and credit subsidies as potential alternatives to negative rates.

Meanwhile, Sweden’s economy is one of Europe’s strongest, with economic growth above 2 percent, high labor-market participation rates and healthy surpluses.

Af Jochnick says the Riksbank is confident that its policies have “contributed to the good economic development that we have now and that we continue to have.”

“We’re entering a completely different situation in the economy now,” she said. “The economy has peaked and our view is that we’ll continue to have quite good growth. Growth will be somewhat lower, but inflation will be around 2 percent.”

--With assistance from Rich Miller.

To contact the reporters on this story: Amanda Billner in Stockholm at abillner@bloomberg.net;Rafaela Lindeberg in Stockholm at rlindeberg@bloomberg.net

To contact the editors responsible for this story: Jonas Bergman at jbergman@bloomberg.net, Tasneem Hanfi Brögger

©2019 Bloomberg L.P.