Stronger Budget Result in 2019 Masks Brazil’s Harsh Debt Reality

Stronger Budget Result in 2019 Masks Brazil’s Harsh Debt Reality

(Bloomberg) --

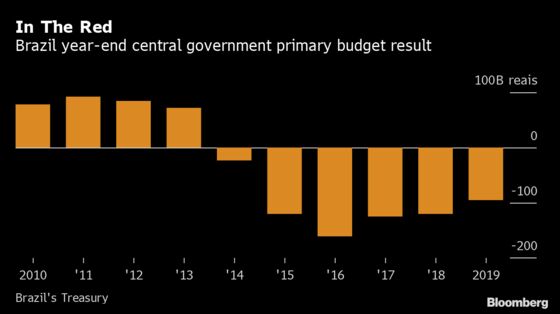

Brazil ended 2019 with the strongest budget result in five years, but its goal of systematically lowering the debt burden is at least three years away and ridden with uncertainty.

Latin America’s largest economy posted a primary budget balance -- which excludes the cost of servicing debt -- of 95.1 billion reais last year, according to Treasury data for the central government released on Wednesday. It was the best performance since 2014, but it was only possible due to extraordinary revenues, including repayments from public banks to the Treasury and an oil auction that yielded 70 billion reais to government coffers.

“The government hasn’t made all the fiscal adjustment it needs to do,” Treasury Secretary Mansueto Almeida told reporters after the data was released, adding that one-time revenues have been shoring up Brazil’s fiscal results since 2016. “The country needs to save an additional 3% of GDP.”

While comprehensive budget data including the performance of states, municipalities and state-owned companies will only be released on Friday, the economy ministry estimates Brazil ended 2019 with a primary budget deficit around 1% of gross domestic product, smaller than the initial forecast for a 1.8% shortfall. A balanced primary budget could become reality before the end of 2022 if additional reforms are approved, special Finance Secretary Waldery Rodrigues said last week.

Since last year’s passage of a substantial pension overhaul, President Jair Bolsonaro’s administration has been pushing measures to increase control over the federal budget and implement new cost cuts. The government is racing against the clock, however, as municipal elections this October may reduce lawmaker appetite for additional belt-tightening measures, including a proposal to lower salaries for new public servants.

“We won a battle with the pension reform, but we didn’t win the war,” said Felipe Salto, director of the Senate’s fiscal studies center, known as IFI. “We need to distinguish between temporary wins and definitive ones.”

Record-Low Rates

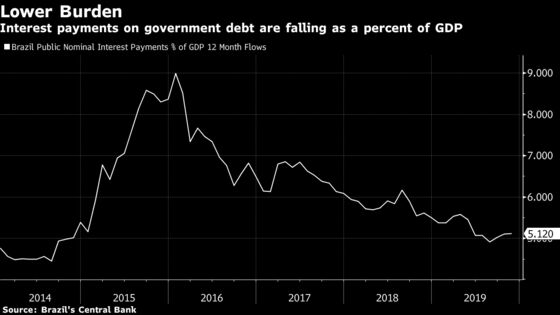

If the fiscal reform drive isn’t sustained, it may be harder for Brazil to keep borrowing costs at the record-low levels that have helped reduce interest payments on debt. The central bank’s monetary easing has been facilitated by austerity measures and a timid recovery, but growth forecasts for this year are increasing in a sign that the benchmark Selic rate may eventually have to rise.

“Half of gross public debt is affected by Selic interest rate,” said Almeida. “If the scenario changes, investors will react and interest rates will go up. Public debt will follow and everything will get worse. That’s why the reform agenda has to advance.”

Any weakening of Brazil’s reform momentum could also inflict damage to its sovereign credit profile, Moody’s Investors Service Inc. senior analyst Samar Maziad wrote in a statement dated Jan. 21. Additional measures are needed to reduce spending rigidity, she wrote.

Navigating Brazil’s notorious budget restrictions has arguably been easier said than done. Roughly 90% of government spending is mandated by the country’s constitution, meaning there’s little leeway to cut spending if not through an exhaustive process of constitutional amendments.

For Jose Franco Medeiros de Moraes, undersecretary for public debt at the Economy Ministry, that means Brazil has no other choice rather moving forward with the current economic agenda, which is focused on reducing mandatory expenses.

“Only fiscal consolidation will be able to keep public debt under control,” he said. “We have to keep working to reduce public spending.”

--With assistance from Rafael Mendes.

To contact the reporter on this story: Martha Beck in Brasilia at mbeck96@bloomberg.net

To contact the editors responsible for this story: Walter Brandimarte at wbrandimarte@bloomberg.net, Matthew Malinowski

©2020 Bloomberg L.P.