Strategists Ponder Sub-1% U.S. Yields

The Federal Reserve’s ready-to-act tone is prompting strategists to fret about just how far U.S. yields could sink.

(Bloomberg) -- The Federal Reserve’s ready-to-act tone Wednesday is prompting strategists to fret about just how far U.S. yields, which are already near historic lows, could sink.

Take Bank of America Corp.’s Bruno Braizinha, for example. His baseline forecast is still mild: 2.05% for 10-year Treasuries in the first quarter of next year, close to the current level of 2%. But he’s entertaining the possibility that the rate could get close to zero by the end of next year.

“Bond yields reflect the fragility of economies,” Braizinha, Bank of America’s director of U.S. rates strategy, said in an interview. Treasuries could rally more because they “will be one of the few developed-world safe havens that retains some value for investors in either our base-case or hypothetical scenario.”

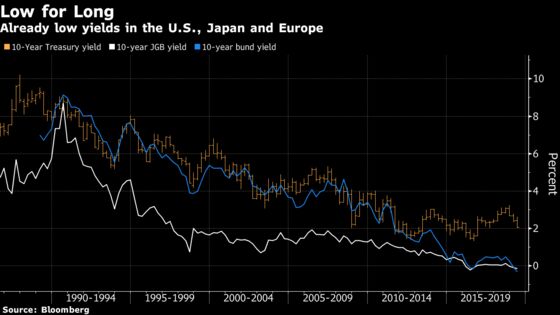

He’s not alone in pondering the possibility things get fraught. Jon Hill at BMO Capital Markets says 10-year notes could “easily” go below 1% in the next 12 to 18 months if the Fed is viewed as taking drastic easing action, while 10- and 30-year rates in Japan and Germany could also move lower.

A day after Fed Chairman Jerome Powell seemed to confirm some strategists’ view that the first rate cut may be 50 basis points, investors continued to pile into bonds, sending the 10-year yield below 2% for the first time since November 2016. The U.S. central bank would join a large chunk of the developed world that’s been adding stimulus, including the European Central Bank and Bank of Japan. Bank of America expects 14 central banks to lower rates this year, including more than one move by those in the U.S, China, Brazil and Russia.

“If we’re in a world where the Fed is seen as returning to the zero lower bound, and then starting another QE program, that could easily be enough to push 10-year yields below 1%,” Hill said in an interview. “Although not our base case, it is possible that scenario could play out in the next 12 to 18 months.”

BMO’s baseline forecast calls for the 10-year Treasury to stay below 2% until inflation accelerates, assuming the Fed starts to cut rates. It sees 1.93% as the lower bound of the yield’s current trend. But if the market starts to price in the prospect of even more rate cuts from the Fed, there would be little to keep the yield from falling through 1.50% once it breaks below 1.65%, according to BMO.

A shift to an easing cycle by the Fed, along with the ECB and BOJ, would put downward pressure on 10-year and 30-year Treasuries, bunds and JGB yields, Hill said. The yield on 10-year German government debt has largely stayed below zero since March, while Japan’s is at minus 0.17%, approaching its July 2016 all-time low of minus 0.3%.

World’s Stockpile of Negative-Yielding Bonds Tops $12 Trillion

Before Thursday, the closely followed 10-year Treasury yield -- which acts as a benchmark for auto loans, credit cards, home mortgages and student debt and also serves as a barometer of investor confidence -- had stayed above 2% since November 2016, when Donald Trump won the U.S. presidential election, leading to a selloff in Treasuries and the biggest rise in the yield in more than half a century.

The yield reached a record closing low of 1.3579% on July 8, 2016. Investors flocked to safety on signs of global stagnation despite the U.S. economy’s strength, confident that the Fed would continue to be on hold with rates, while the ECB and BOJ were using negative rates.

“The 1.35% to 1.50% range for 10-year Treasury yields is rather significant,” given the strong resistance there in 2012 and 2016, Braizinha said. It’s also worth paying attention to the yield difference between 2-year and 10-year Treasuries, which could either follow the pattern of past easing cycles by steepening toward 125 to 150 basis points or converge toward 25 to 50 basis points in a scenario in which the Fed cuts rates to zero, he said. It’s currently about 27 basis points.

Barclays Chief U.S. Economist Michael Gapen sees the 10-year yield at 1.95% through year-end and says getting it below 1% might require a worse-than-average recession similar to the one seen in 2007-2009, “a lot of deflation,” or a Fed yield-curve target. Anne Walsh, chief investment officer of fixed income at Guggenheim Partners, says the yield may be destined for 1.5%, while TD Securities strategists such as Priya Misra say it may drop to 1.30% by the second quarter of 2020, which would be a record low.

A number of strategists had already cut their 2019 forecasts in May, when Treasury yields slid to the lowest levels in more than a year. On Tuesday, the 10-year yield was pushed to the brink of breaching 2% after ECB President Mario Draghi said more stimulus would be needed in the euro region if the outlook doesn’t improve.

“If yields continue to fall globally, that would be under a scenario in which growth is weak, and we would favor higher-quality fixed income and equity investments,” said Tracie McMillion, head of global asset allocation strategy at Wells Fargo Investment Institute, part of a division that oversees $1.8 trillion in assets.

With a forecast of 2% to 2.5% for the 10-year yield through year-end, McMillion says “the market really is trying to balance demand for Treasuries with the potential for some good news on trade.”

--With assistance from Masaki Kondo and James Hirai.

To contact the reporter on this story: Vivien Lou Chen in San Francisco at vchen1@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Nick Baker, Mark Tannenbaum

©2019 Bloomberg L.P.