Asia's Stocks Post Worst Start to Year Since 2016: Blame China

Hong Kong’s Hang Seng Index tumbled 2.8 percent, its biggest drop in more than two months.

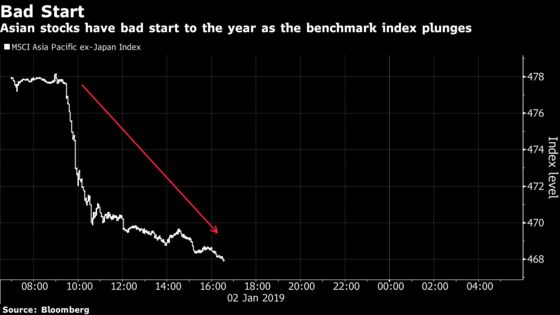

(Bloomberg) -- So much for starting off the new year on the right foot.

The benchmark gauge of Asia-Pacific stocks excluding Japan slumped 1.9 percent at 4:39 p.m. in Hong Kong as traders returned to work in key regions including Hong Kong, China, Taiwan and Korea. Japan markets are closed and reopen on Jan. 4.

Wednesday’s plunge, which is the worst start to the year in three, has one culprit: China’s factory conditions slumped in December. To be precise, the Caixin Media and IHS Markit PMI fell to 49.7 from 50.2, its lowest reading since May 2017.

“Asian markets took a deep dive into negative territory following another disappointing China Caixin manufacturing PMI reading,” said Margaret Yang, market analyst at CMC Markets, in a note to clients. “China manufacturing PMI is falling at a pace faster than economists’ forecast, suggesting global economic slowdown and trade war is hurting the country’s manufacturing activities.”

That sent several key stock gauges across Asia down Wednesday:

- Hong Kong’s Hang Seng Index tumbled 2.8 percent, its biggest drop in more than two months

- The Shanghai-Shenzhen CSI 300 Index dropped 1.4 percent to its lowest close since March 2016

- Benchmarks in Taiwan and Korea declined at least 1.5 percent to snap brief, two-day rallies

- Australia’s S&P/ASX 200 lost 1.6 percent

- U.S. stock-index futures, which rose before China data came through, erased those gains and plunged 1.9 percent

This isn’t the first country to report deteriorating factory conditions across the region’s export-heavy economies with supply chains more tightly interwoven than ever. Taiwan, Malaysia, Vietnam, the Philippines and South Korea were hit by the U.S.-China trade war and a fading technology boom. Earlier Wednesday, Singapore’s economic growth slowed to an annualized 1.6 percent in the fourth quarter and home prices fell for the first time in six quarters.

This year “is going to be a challenging year for everybody, not just China but also globally,” Yang said in an interview with Bloomberg TV. “We are probably off the peak of a cyclical upswing,” with factory conditions slowing down in European countries as well, she said.

Dry Powder

Cliff Tan, MUFG Bank Ltd.’s East Asia head of global markets research, suggests keeping your “powder pretty dry” until at least the end of the first quarter as investor “nervousness” is likely to continue. Jitters primarily reflect earnings revisions that haven’t bottomed out yet, he added.

“With the Fed probably undecided on what it needs to do on the interest-rate front, I don’t see how folks can be too sure about anything,” Tan said.

Focus on Developed Markets

While Asian stocks led market declines last year and appear to be picking up where they left off, it’s developed markets that will be under the microscope in 2019, especially as Democrats take over the House in Congress, said Clive McDonnell, head of equity strategy at Standard Chartered Private Bank in Singapore.

“It’s rather developed markets that are under a little more pressure, given the extent Asia markets declined last year,” McDonnell said. This trend emerged in December when it was the U.S. that drove the downside in markets, he added.

Stomach the Volatility

“The overly pessimistic view that investors have adopted is likely to bleed through into January,” said Kerry Craig, Melbourne-based global market strategist at JPMorgan Asset Management. “Given that a weaker global-growth outlook, and in my view misplaced recessionary fears, are the core of that view, until we see a stabilization or improvement in the economic data from the major economies, China, U.S. and the euro zone, markets may have a tough time.”

Craig suggests that a balanced portfolio of stocks and bonds will likely deliver returns this year, which could be an improvement compared with 2018.

“For investors who can look past the end of this cycle and through to the next, they may be willing to stomach the volatility for the long-run return potential,” he said.

Investors Understand

Martin Lakos, a division director in Macquarie Group’s wealth-management division, says investors are well aware and understand where the increased volatility came from. “Two very distinct periods” of market complacency are the reasons behind the heightened turbulence this year: the lack of volatility for 15 months after U.S. President Donald Trump was elected and then the easing off of choppy moves after the global rout in February.

“And when you put that in perspective for clients, they understand to some extent where this volatility’s been generated from because we’re probably heading back towards more normal levels of volatility,” Lakos said.

Too Soon

For the head of Asia equity strategy at Societe Generale, don’t buy the dip just as yet. Frank Benzimra said that while stock valuations are increasingly becoming more attractive, especially in China, it’s still too early to start buying.

“We stand with our 2019 Asia equity outlook title: too early to add risk. The good news, for Asia assets and beyond, is that we start the year with lower valuation than one year ago,” he said.

--With assistance from Abhishek Vishnoi, Livia Yap and Matthew Burgess.

To contact the reporter on this story: Eric Lam in Hong Kong at elam87@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Divya Balji, Cecile Vannucci

©2019 Bloomberg L.P.