As Foreigners Flee Turkey Debt, Central Bank Helps Fill Void

Stealth Turkish Easing Stirs Rally in Bonds Dumped by Foreigners

(Bloomberg) -- The Turkish central bank has kicked off its biggest government debt buybacks in over a decade, helping fill a void left by foreigners and adding momentum to the developing world’s strongest bond rally this year.

As part of a program designed to manage the banking system’s liquidity, policy makers purchased about 1.9 billion liras ($318million) of local-currency government bonds through auctions since the beginning of January, equivalent to around a third of total acquisitions last year, according to data on the central bank’s website. Benchmark bond yields have plunged some 200 basis points over the period, outpacing a decline among peers by a factor of four.

In December, the central bank announced plans to almost double the amount of government debt on its balance sheet to 5% of total assets, which currently works out to 33.3 billion liras. According to Bloomberg calculations, it would need to purchase around 17 billion liras of the securities through the end of the year to reach that goal, when redemptions are taken into account.

“We think these transactions, in addition to managing liquidity, will have an effect similar to quantitative easing and will impact financial conditions,” said Erkin Isik, chief economist at QNB Finansbank in Istanbul.

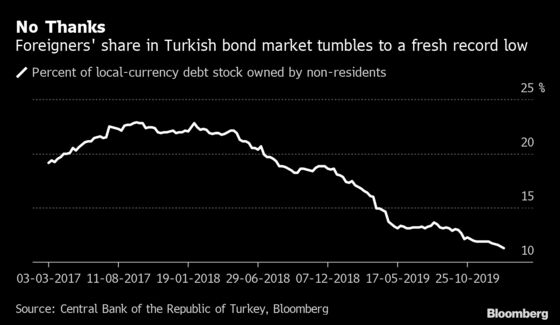

The emergence of the central bank as a buyer has loomed large in a market that foreigners have been abandoning in droves. Data last week showed outside investors sold Turkish bonds for a fifth week running, bringing total outflows over the past year to more than $3.3 billion and driving their share in the local-currency debt market to an all-time low of 11%.

The purchases are intensifying at a time when local pension funds and primary dealers clamor to increase their holdings amid a dearth of long-dated issuance. The Turkish Treasury hasn’t sold a 10-year bond in 18 months and isn’t slated to offer one at least through April, putting downward pressure on government borrowing costs.

Absorbing Risk

“By absorbing interest risk from the market -- in size like it’s doing now -- the central bank is essentially giving banks more room to do other things, like extend loans,” Isik said.

But after five rounds of massive monetary easing, combined with three months of accelerating inflation, Turkey’s real rate now stands below zero, raising concern that the central bank risks loosening its stance more than warranted. President Recep Tayyip Erdogan has repeatedly said that policy rates will fall into single digits this year.

“The rally is, first, unsustainable,” said Lutz Roehmeyer, chief investment officer of Capitulum Asset Management in Berlin. “And, second, foreigners still have big doubts about the economics and politics, even fear non-convertibility of the lira or blocking of bonds in case of U.S. sanctions.”

In an effort to prop up the lira, state banks have flooded the market with dollars at moments of heightened volatility in the currency, a move that prompted S&P Global Ratings to classify Turkey’s foreign-exchange regime on Friday as a “managed float.” Last year, authorities engineered a liquidity squeeze in the offshore swap market to stand in the way of foreign short-sellers.

The yield on Turkey’s 10-year local currency bonds added 1 basis point on Tuesday, trimming this year’s drop to 193 basis points.

International investors are already “out of bonds to sell,” according to Viktor Szabo, an investment director at Aberdeen Asset Management in London.

“For foreigners, Turkish government bonds don’t look like a very attractive proposition,” he said. “The central bank’s inflation-targeting track record is appalling, and the currency is artificially kept so strong.”

To contact the reporters on this story: Constantine Courcoulas in Athens at ccourcoulas1@bloomberg.net;Tugce Ozsoy in Istanbul at tozsoy1@bloomberg.net

To contact the editors responsible for this story: Onur Ant at oant@bloomberg.net, ;Alex Nicholson at anicholson6@bloomberg.net, Paul Abelsky

©2020 Bloomberg L.P.