(Bloomberg Opinion) -- Bill Winters, the target of the biggest shareholder mutiny at a large British bank in five years, is taking the fight back to his detractors.

The Standard Chartered Plc chief executive officer looks in no mood to throw in the towel on his promise to achieve a double-digit return on tangible equity by 2021. In a world that’s slipping back into low growth, slow inflation and rock-bottom interest rates, that had started to appear a chimera. Noel Quinn, Winters’ counterpart at bigger rival HSBC Holdings Plc, this week abandoned a similar 11%-plus target after missing its goal by 4.6 percentage points.

StanChart, by contrast, posted a 16% jump in third-quarter adjusted pretax profit to $1.24 billion that defied analysts’ expectations of a small decline and pushed return on tangible equity to 8.9%. That’s a 1.6 percentage point increase from a year earlier.

Things could still go south. Winters, who’s been facing an investor revolt over his pay, acknowledged “growing headwinds from the combination of continuing geopolitical tensions and expectations of declining near-term global growth and interest rates."

Operating income from trade financing has slipped this year. And that’s not the only risk. As with HSBC, which took a $90 million charge for Hong Kong this week, the former British colony is StanChart's single-biggest profit engine. StanChart’s fortunes, though, aren’t as tightly tied to the protest-hit city. By risk-weighted assets, Southeast and South Asia are as important to the specialist emerging markets lender as Greater China and North Asia.

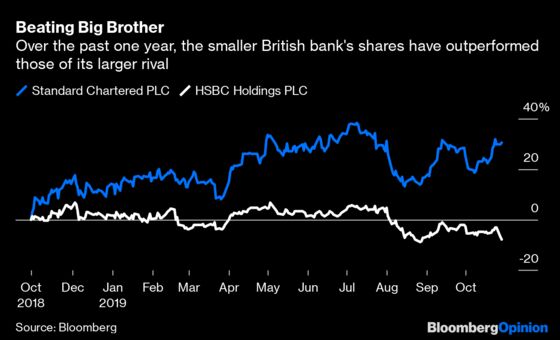

Besides, StanChart is rapidly expanding the footprint of its digital bank in Africa. Investors are excited by the mobile-banking push, which coupled with cost cuts and a share buyback, has propelled StanChart shares close to 30% higher in London over the past year, compared with a near 8% decline in HSBC stock in the same period. However, the bank’s net interest margin, which had perked up to 1.62% in the June quarter, has since declined to 1.56%.

For Winters to swim against the tide of low interest rates could mean lending to more risky customers. That could, in the medium term, jeopardize the boost to shareholder returns from a long and painful fix to the bank’s credit culture. With impairment charges almost 60% higher in the September quarter from the previous three months, lunging for risk may not be a great option even in the short run.

Capital could be another stumbling block. The common equity Tier 1 ratio is down to 13.5%, from 14.5% a year ago. For all its troubles, HSBC has managed to keep this figure above its goal of 14%. If StanChart doubles down on the $1 billion buyback it announced in April to further juice shareholder returns, it could start running thin on resources for future growth. That wouldn’t be very wise, especially since operating income from private banking, which uses little capital, has been flat this year. Not only will Africa require more investment, StanChart also has to open a new virtual bank in Hong Kong next year.

Quinn at HSBC has embarked on a full-blown remodeling of the bank. Winters, by comparison, seems to be on a surer footing. StanChart’s cost-to-income ratio is falling steadily. Growth in cash management isn’t only helping compensate for flagging trade finance, it’s also giving the bank access to sticky corporate deposits.

A recent Financial Times report suggests the StanChart boss might voluntarily accept a pay cut. A peace offering to investors might be a good idea, though on this evidence Winters can argue that he’s earning his keep.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.