Southeast Asian Currencies Face Central Bank Hurdles This Week

Southeast Asian Currencies Face Central Bank Hurdles This Week As Growth Expectations Need To Be Monitored

(Bloomberg) -- A rally in Southeast Asia’s currencies is petering out as a global surge in coronavirus infections tampered vaccine optimism. Policy outlooks by three central banks this week may offer clues for growth expectations.

Bank of Thailand and Bank Indonesia, whose currencies rallied the hardest last week, will be under scrutiny for any signs of alarm at the pace of appreciation and potential dovish tilts that could diminish their yield advantage. Bangko Sentral ng Pilipinas said last Wednesday there’s room to cut its reserve requirement ratios.

“We see two themes driving markets into year-end,” says Divya Devesh, head of Asean and South-Asia FX research at Standard Chartered Plc in Singapore. “Firstly the search for yield and secondly re-rating of growth expectations following vaccine confirmation.”

Global funds have piled into Southeast Asia’s bonds and equity markets as global risk-on sentiment spurred a hunt for higher returns. Inflows into Thai sovereign debt have climbed to the highest in 17 months in November, even though the month is less than half over. Offshore funds are set to be net buyers of Indonesian stocks this month for the first time since May.

Here’s a look at some key currency levels for the region going ahead:

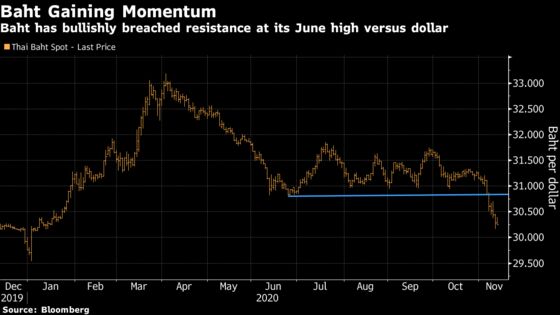

THAILAND:

The baht rose to its highest in 10 months last week, bullishly breaching resistance at its June high and paving the way for further advances. “THB is performing strongly, benefiting both from a return of bond and equity inflows as well as hopes that a vaccine will help boost the tourism industry,” said Mitul Kotecha, senior emerging markets strategist at Toronto Dominion Bank in Singapore. The baht may have difficulty breaching 30 per dollar level in the near-term, he said. It closed at 30.176 on Friday.

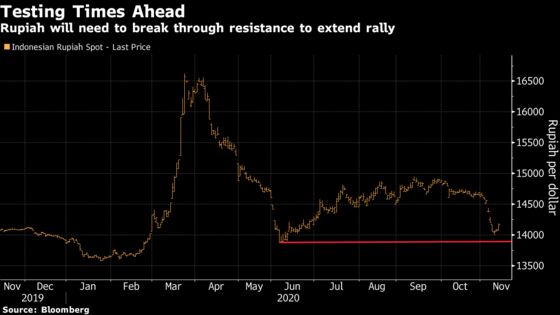

INDONESIA:

The rupiah gained over 3% this month but resistance at 13,878, a June 5 low, remains intact. This level maybe tested if foreign carry trade demand picks up given Indonesian yields are among the highest in the region. Bank Indonesia is expected to keep its key rate on hold at 4% this Thursday. It’s kept rates on hold in its last three meetings to support the rupiah after slashing borrowing costs by 1 percentage point this year.

SINGAPORE:

The Singapore dollar’s nominal effective exchange rate started weakening in mid October providing the currency with room to appreciate into year-end. The trade-reliant economy is expected to get cues from October non-oil domestic exports data this Tuesday, which is seen slowing to 5.1% year-on-year according to a Bloomberg survey.

PHILIPPINES:

The Philippine peso has rallied to be Southeast Asia’s best performer this year, bringing into sight the next psychological level of 48 per dollar. The currency closed at 48.21 on Friday. It has been buoyed by a narrowing trade gap, that’s boosted its current account surplus. Overseas remittances this week will also be watched closely after they unexpectedly dropped last month.

MALAYSIA:

The ringgit’s rally against the dollar has stalled at resistance near 4.10 per dollar. Inflation data later in the month could provide clues on growth prospects after the gauge fell 1.4% from the previous year in September.

Below are the key Asian economic data and events due this week:

- Monday, November 16: RBA Governor Lowe speaks, China industrial production, retail sales, fixed assets ex-rural and 1-year medium-term lending facility, Indonesia trade balance, New Zealand performance services index, Japan industrial production and 3Q GDP, Philippine overseas remittances, Thailand 3Q GDP

- Tuesday, November 17: RBA minutes, Singapore non-oil domestic exports

- Wednesday, November 18: Australia 3Q wage price index, RBA’s Lowe participates in panel, New Zealand 3Q PPI input/output, Japan trade balance, Bank of Thailand rate decision

- Thursday, November 19: Australia employment, Bank Indonesia rate decision, Philippine BoP overall and BSP rate decision

- Friday, November 20: Japan CPI and PMI’s New Zealand credit card spending, China 1-year and 5-year loan prime rate, South Korea PPI, Indonesia 3Q BoP current account balance

©2020 Bloomberg L.P.