Lagarde Faced Reservations About ECB’s Pandemic Purchase Program

Some ECB Officials Had Doubts About Emergency Bond Purchases

(Bloomberg) -- European Central Bank President Christine Lagarde had to overcome reservations from some of her colleagues three weeks ago to push through her emergency response to the coronavirus pandemic.

The account of the March 18 teleconference published Thursday showed how divided officials were about dealing with “severe strains” in financial markets and the advent of Europe’s biggest recession in decades.

Policy makers raised questions over whether the ECB needed a new program to provide support to the 19-nation euro area, and whether long-established rules on bond purchases needed to be thrown overboard to highlight the institution’s determination to act.

“All members agreed that a further forceful monetary policy response was warranted,” the account showed, yet there were “some nuances of views regarding specific elements of the proposal.”

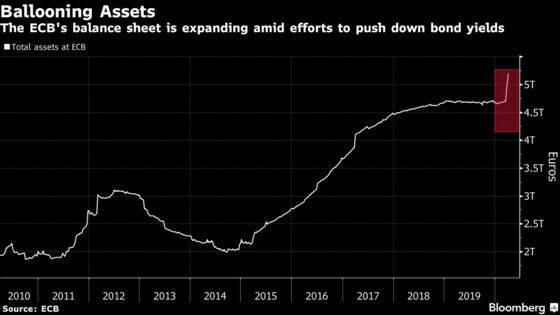

The ECB eventually approved a 750 billion-euro ($815 billion) purchase program with wide-ranging flexibility, including lifting constraints on how much of each nation’s debt the central bank can hold. The plan was backed by a “large majority” of policy makers.

“Some members” of the Governing Council “expressed a preference for employing the existing toolkit” such as an increase in ongoing quantitative easing or even the targeted bond-buying tool known as Outright Monetary Transactions.

OMT was developed during the debt crisis in 2012 and can target stressed nations, but only on the condition they also have a credit line with the region’s bailout fund.

At the same time, some officials had qualms about signaling the suspension of issuer limits. “It was recalled that these limits were one of the safeguards to ensure that the Governing Council acted within its mandate,” according to the account.

Element of Surprise

Lifting those caps underscored the ECB’s pledge to step up monetary stimulus again, if needed, and some economists are already predicting that more is in the pipeline. ABN Amro said on Wednesday purchases under the emergency program could be raised by another 500 billion euros as early as this month.

Lagarde hasn’t ruled out further action. She told French newspaper Le Parisien in an interview published late Wednesday that the ECB has other solutions should things deteriorate further, but “I’m not going to tell you which ones, because the impact will also be linked to the element of surprise.”

What Bloomberg’s Economists Say

“Minutes from the European Central Bank’s meetings are normally most useful for getting a sense of what the Governing Council will do next. The accounts from its gatherings last month suggest additional asset purchases are more likely than a deposit rate cut, if more action were required.”

-- David Powell. Read the ECB REACT

Some officials had pushed for a rate cut on March 12, according to an account of that meeting also published Thursday. In the end though, most members agreed an increase in bond purchases “would be more effective in lowering risk-free rates.”

That meeting failed to quell market panic, partly because of Lagarde’s gaffe that the ECB wasn’t there to “close spreads,” a comment that revived memories of the 2012 debt crisis.

At the emergency call six days later, the president acknowledged that “uncertainty on the economic front was creating severe strains in the financial markets.” She also noted “the message that, first and foremost, fiscal support was required had been well understood, and many governments had already responded.”

National administrations have announced massive stimulus programs, but have failed to agree on common solutions such as jointly issued debt -- so-called coronabonds -- that would help the most indebted member states to shoulder the cost of the crisis.

Lagarde has previously pushed for coronabonds but told Le Parisien that there’s no need for a “fixation” on that instrument, which is opposed by countries such as Germany for fear of becoming liable for other nations’ overspending.

©2020 Bloomberg L.P.