SNB Keeps Cool as Franc Surges to 2015 Highs: Decision Guide

SNB Keeps Cool as Franc Surges to 2015 Highs: Decision Guide

(Bloomberg) -- Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

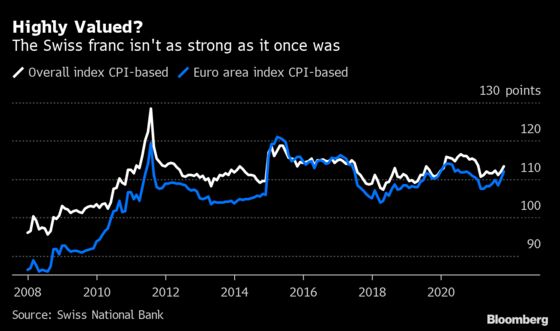

The Swiss National Bank’s long-standing claim that the franc is “highly valued” is looking harder to justify as officials watch it strengthen to within striking distance of parity with the euro.

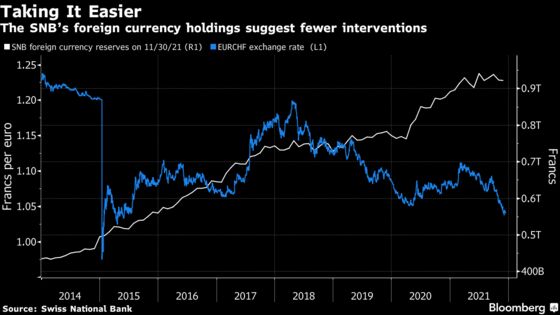

When the currency climbed through what was once considered a key line in the sand to 1.04 per euro this month, the surge wasn’t met with big central-bank interventions. That laid-back approach suggests SNB officials led by President Thomas Jordan are growing more comfortable with the level of the exchange rate.

“The Swiss franc isn’t highly valued anymore,” said Adriel Jost, partner and managing director at the consultancy WPuls, and a former SNB staffer. While the SNB’s own data point to an overvaluation, Jost calculates that the franc is actually slightly undervalued on a trade-weighted basis. “This explains the SNB’s reticence concerning interventions in the past few weeks.”

One reason to be sanguine is Switzerland’s comparably low rate of inflation versus the euro area or the U.S., helping shift the balance for purchasing power. Even so, an unbothered stance is all the more remarkable considering the franc is at the highest since the aftermath of the SNB’s seismic abandonment of its cap on the currency in 2015.

How officials describe the franc will feature in their decision on Thursday at 9:30 a.m. in Zurich. The central bank is all but sure to keep both its policy and its deposit rate at -0.75%. There will also be new growth and inflation forecasts, and Jordan will later brief the press.

The SNB’s statement will arrive during a final flurry for 2021 of global central bank meetings at a time when they are all struggling to assess different threats posed by inflation and of the omicron variant of the coronavirus.

The U.S. Federal Reserve, whose announcement is due the evening before, has shown more alarm at the surge in prices that the European Central Bank, which is scheduled to release its own decision later on Thursday.

Switzerland has so far bucked the trend with much weaker headline inflation, most recently reaching 1.5%. The currency’s strength and a consumer-price basket of which energy constitutes only 4% have meant more muted effects in the data than seen elsewhere.

For its super-easy stance, the SNB needs to keep money market rates close to its policy rate of -0.75%. But the Swiss Average Rate Overnight, known as SARON for short, has drifted higher, and officials could decide that it needs to be pushed back down.

Credit Suisse Group AG economist Maxime Botteron believes the SNB may tackle the problem by giving banks less of an exemption on the cash being hit with negative rates, by lowering the threshold to 27 from 30.

The SNB could also call for reactivate the countercyclical capital buffer for banks’ mortgage exposure, to temper real estate market exuberance. Having suspended the requirement during the initial weeks of the pandemic, the SNB has since warned repeatedly about the buildup of risks.

Any formal decision lies with Switzerland’s executive, which acts based on the SNB’s recommendation.

| Read More... |

|---|

|

©2021 Bloomberg L.P.