This Stock-Market Slump Is Everybody's Business

A worrisome decline in transport shares leads market commentary. Plus, “risk on” with a twist and China rally doubters.

(Bloomberg Opinion) -- In the history of slumps, the recent 3.49 percent drop in the Dow Jones Transportation Average from this year’s high on Feb. 21 isn’t particularly notable. There is something troubling, though, about the way the index has fallen. More specifically, Wednesday’s drop in the gauge – which is chock full of companies with greater-than-average exposure to global trade and economic growth – was the ninth straight, marketing its longest slump since February 2009. That should raise eyebrows.

At the least, the decline in the transports – whose members include railroad Norfolk Southern Corp., package delivery company FedEx Corp. and trucking firm J.B. Hunt Transport Services Inc. – confirms the recent data showing a big slowdown in economic growth this quarter. But given that the stock market is inherently forward-looking, the drop certainly raises concern that the worst is yet to come, especially with worries mounting that the U.S. and China may fail to reach a “real” trade deal that bolsters growth for both sides. Federal Reserve Bank of New York Fed President John Williams said Wednesday that he expects economic growth to slow to around 2 percent this year. That’s a pace that will excite no one. And at about 13 times this year’s forecast earnings, the Dow Jones Transportation Average is trading at near its lowest valuation of the last 10 years, which isn’t a sign of confidence in the outlook. This isn’t just a U.S. phenomenon. Four of the 10 gauges tracked by Bloomberg to assess the health of global trade are now below their long-run averages, compared with zero in November.

The Organization for Economic Cooperation and Development on Wednesday slashed its 2019 world growth forecast to 3.3 percent from its prior estimate of 3.5 percent. “The global expansion continues to lose momentum,” the Paris-based OECD said as it downgraded almost every Group of 20 nation’s economy. “Growth outcomes could be weaker still if downside risks materialize or interact.”

‘RISK ON’ ISN’T WHAT IT USED TO BE

The bulls might say that the Dow Jones Transportation Average is still up about 12 percent this year, beating the Dow Jones Industrial Average and the S&P 500 Index. Also, so-called risk assets in general are doing well. True, but the strategists at Arbor Research & Trading have uncovered some interesting developments in the “risk-on” trade that they haven’t seen before. Based on exchange-traded fund data, investors have steered flows into U.S. corporate bonds, emerging-market equities and global debt in 2019. Commodities and global equities have suffered outflows. “The fears of a protracted global slowdown are quite high, pushing flows into assets expected to weather continued dovish rhetoric from central banks and low interest rates,” Arbor Research data scientist Ben Breitholtz wrote in a research note Tuesday. Outflows from global equities have been redirected to global debt ETFs. The past 20 trading days have seen the strongest inflows, totaling over $4.5 billion, in the history of these ETFs, according to Breitholtz. “Sub-par global-growth outlooks have investors fleeing any and all commodities with the majority of the damage felt by precious metals,” Breitholtz wrote. “Not surprisingly, investors are seeking the strongest performing asset in international bonds.” Investors are likely to continue to seek the stability of securities found in aggregate bond indexes until the global economic data shows improvement, he concluded.

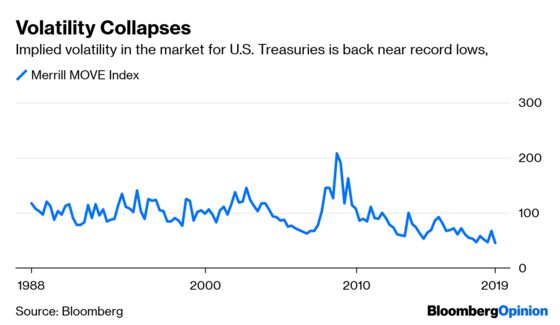

THE MESSAGE IN LOW BOND VOLATILITY

Speaking of bonds, Wednesday was a good day to be long government debt of all kinds. Yields on sovereign bonds fell across the board, led by Canada, the U.K., Italy and France – to name just a few. After reaching a high of 1.62 percent in October, the yield on the Bloomberg Barclays Aggregate Treasuries Index of global government debt has fallen back to about 1.34 percent. The move makes sense, given the OECD’s dour outlook and more central banks throwing in the towel on their optimistic view of the economy. Take the Fed’s latest Beige Book economic report released Wednesday. Based on anecdotal information collected by the 12 regional Fed banks through Feb. 25, the central bank characterized growth as “slight to moderate” across most of the country. That’s a downgrade from the last report, which noted growth was “modest to moderate.” The government shutdown certainly damped consumer spending, but what’s worrisome is that companies reported “concerns about weakening global demand, higher costs due to tariffs and ongoing trade policy uncertainty.” It appears bond investors don’t expect a rebound anytime soon. The Merrill Lynch MOVE Index, which tracks expected volatility in the $15.3 trillion market for Treasuries, has fallen back toward some of its lowest levels ever, suggesting traders don’t see any big change in yields on the horizon.

ANOTHER ONE BITES THE DUST

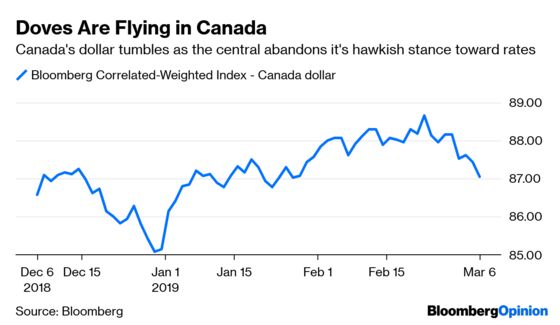

The Bank of Canada capitulated on Wednesday. As perhaps the last holdout among major central banks signaling the need for tighter monetary policy, the Bank of Canada now sees less of an urgency to raise interest rates as officials expressed greater uncertainty about the outlook amid a deeper-than-expected slowdown. Shifting from the tone from their most recent statement in January, policy makers dropped their assertion that rates will need to rise over time, replacing it with an observation that the economy continued to require stimulus and that there was “increased uncertainty” about the timing of future increases. The move has significant implications for Canada’s dollar, reducing most of the incentive to buy the loonie. It fell to its lowest level since January against a basket of nine other developed-market currencies. Yes, Canada’s dollar is still greatly influenced by oil prices, with the strategists at BNY Mellon noting that the correlation between the two are at the high end of its historical range, but the central bank’s newfound dovishness may change that. The Bank of Canada “has been one of the few central banks which had been seen to be more hawkish than the Fed,” BNY Mellon currency and macro strategist John Velis wrote in a report. “Expect that ‘relative policy expectations differential’ to tighten from here,” clouding the outlook for the loonie.

CHINA RALLY DOUBTERS

There’s no shortage of market participants who subscribe to the theory that as Chinese stocks go, so go stocks in the rest of the world. There’s something to that, as 2018’s big slump in Chinese equities foreshadowed the slide in major stock markets at the end of last year. And this year, the Shanghai Shenzen CSI 300 Index is up an amazing 28 percent, thanks to the influx of bargain hunters and some stimulus measured announced by Chinese authorities. That compares with a gain of a little more than 10 percent for the MSCI All-Country World Index. But before getting all bulled-up, consider that a growing number of investors are betting big on a reversal. Short interest in the iShares China-Large Cap ETF, the largest U.S.-listed exchange-traded fund invested in China, has risen by 51 percent this year to 33.2 million shares, data by financial analytics firm S3 Partners LLC show. The dollar value of short exposure has jumped by about $600 million this year to $1.46 billion and now hovers near the highest since May 2017, according to Bloomberg News’s Elena Popina. The $6.4 billion exchange-traded fund, one of the most liquid China-focused ETFs, is seeing its short interest advance as hedge funds use the product to hedge their long exposure in Chinese stocks traded in the U.S. or Hong Kong, Ihor Dusaniwsky, the firm’s managing director of predictive analytics, told Bloomberg News. Chinese stocks kept rising back in 2017, but last year’s decline was epic, sending them to to their lowest levels since early 2016.

TEA LEAVES

The European Central Bank meets Thursday to decide monetary policy, and while no change in interest rates is expected, policy makers are likely to cut their economic forecasts by enough to justify another round of loans for banks. The latest projections show extensive downgrades for inflation and economic expansion in 2019, with an assumption of a pickup toward the end of the year, according to Bloomberg News’s Jana Randow and Carolynn Look, citing people with knowledge of the matter. At the least, this just shows how poor the global economic outlook is at the moment, and helps to explain the malaise that has settled over markets of late. And the ECB may not be overreacting. The OECD cut its euro zone growth outlook to a pitiful 1 percent from an anemic 1.8 percent.

DON’T MISS

Don’t Assume That the Fed Is Done Raising Rates: Bill Dudley

A Manager's Past Performance Matters More Than Ever: Vasant Dhar

Even the Germans Can't Deny Reality in Europe: Marcus Ashworth

Why East European Countries Shun the Euro: Leonid Bershidsky

U.S. Trade Snub Should Be Wake-Up Call for India: Mihir Sharma

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.