Six Suggestions for How to Deal With Ballooning U.S. Debt

U.S. Treasury’s total debt pile already tops $20 trillion, more than $6 trillion more than when President Trump took office.

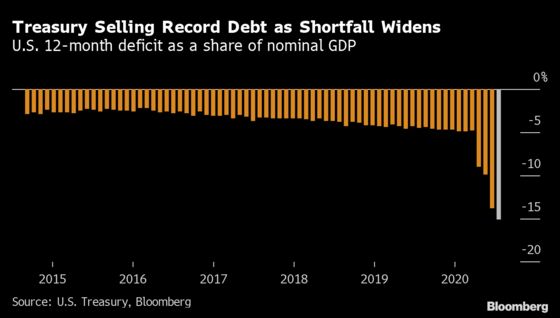

(Bloomberg) -- Efforts to limit the economic fallout from the pandemic are set to swell the U.S. budget deficit to about 15% of gross domestic product—the highest since World War II. That’s forcing record government borrowing. The Treasury’s total debt pile already tops $20 trillion, more than $6 trillion more than when President Trump took office.

The Federal Reserve has slashed rates. introduced an arsenal of programs to support financial markets, and Thursday unveiled a new approach to setting U.S. monetary policy. Yet more fiscal and monetary actions are likely to be necessary to help consumers and businesses through the crisis. And though the U.S. is the world’s largest economy and government borrower, it’s far from being the only country with swollen debt loads from pandemic-fighting measures.

Bloomberg Markets canvassed some investors, policymakers, and economists to get a diverse set of ideas on how the U.S.—and perhaps other economies—should tackle this era of supercharged debt loads.

Jason Cummins, chief U.S. economist at Brevan Howard Asset Management LLP, served as chairman of the Treasury Borrowing Advisory Committee when it advised the Treasury to bring back 20-year bonds instead of issuing 50- and 100-year bonds. The Treasury sold its first 20-year bonds since the 1980s earlier this year.

“Now, more than ever, Treasury has to be a steward and manager of U.S. debt. The way to do that is by funding it in a predictable manner at the least cost over time. And the model developed by several members of the Treasury Borrowing Advisory Committee has shown that that is accomplished by issuing a larger share of debt in the belly of the yield curve, that is, the three- to five-year maturity sector. Especially when you have a huge stock of debt to be sold going forward, which the U.S. does, you want to fund it in the most efficient way possible. This is not the time for Treasury to try new things like experimenting with terming out its debt further—which would be counterproductive in the end by raising borrowing costs for households and businesses.”

Heather Boushey, president and chief executive officer of the Washington Center for Equitable Growth and an economic policy advisor to Democratic presidential candidate Joe Biden, says politicians need to consider beefing up fiscal policy and unwinding some parts of the Trump administration’s 2017 tax law that reduced revenue as a share of GDP.

“How are we going to rethink and raise taxes so we can afford to make absolutely vital investments in the public sector? I don’t think we should do this until we are in recovery—and solidly in a recovery. This is not a plan of action for now.

“We live in one of the richest countries the world has ever seen, and especially since the Great Recession, we’ve seen a continued and sustained increase in wealth inequality in the U.S. and a concentration across firms. [We need to be] looking at something like a wealth tax.

”We need to make sure that the systems that actually execute on fiscal policy are ready to go. Fiscal policy isn't a bunch of people in a room making a decision on the interest rate. It's systems. It's more complicated."

Peter Fisher, professor at Dartmouth College’s Tuck School of Business, ended sales of 30-year bonds in 2001 when he was Treasury Undersecretary. (They were brought back in 2006.) He says the government should sell ultra-long-term bonds or even perpetual securities that have no maturity date. The 100-year bond could be structured to amortize over the life of the bonds, as mortgage loans do, instead of paying interest semiannually and principal at maturity.

“Perpetuals would be nice, but 100-year bonds get you almost to the same place. And amortizing would remove the lump sum principal problem for the investor, and it also reduces Treasury’s refinancing risk.”

Valerie Grant, senior fund manager in the group that runs AllianceBernstein LP’s responsible U.S. equities portfolios, says fiscal policymakers should set aside concerns about deficits and debt and focus on combating both the overall economic toll of the pandemic as well as long-term trends of inequality within the labor market.

“Even before the pandemic, many people were employed in jobs that couldn’t actually sustain a reasonable standard of living. Then you have this crisis, and the consequences are just awful and amplified because of that backdrop. So the fiscal stimulus is needed, and Treasury is having no trouble selling the debt.”

Takeshi Tashiro is a nonresident senior fellow at the Peterson Institute for International Economics.

“The U.S. faces a risk of Japanification. Or you may want to call it secular stagnation. This pandemic demands more aggressive actions by the governments and the central banks. Monetary policy has been doing everything it can. Fiscal policy is the only available policy instrument lately.

“Look at Japan. Debt is not a catastrophe as long as interest rates are low. I’m not saying the U.S. should have a higher level of debt, but huge deficits are not bad as long as you spend where you need to spend. Central banks are doing what they should do as the Fed maintains low rates when the government needs them to.”

Paul McCulley, the former chief economist at Pacific Investment Management Co., who now teaches at Georgetown University, says the U.S. Treasury and Federal Reserve are right to align their efforts and monetize some of the new debt.

“Right now we are in a situation where we unambiguously need fiscal policy dominance, and there’s nothing immoral about that. It’s very practical and is the anti-deflation, pro-democracy outcome we need.”

McCormick covers bonds and FX for Bloomberg News in New York. Dmitrieva reports on the U.S. economy for Bloomberg News in Washington.

©2020 Bloomberg L.P.