Six Sovereign Defaults in 13 Months Roil Latin American Markets

Six Defaults in 13 Months Upend Latin America’s Bond Market

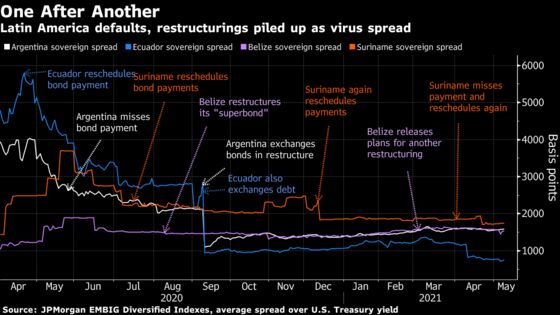

(Bloomberg) -- Sovereign bond defaults have piled up at a dizzying clip in Latin America since the pandemic began. First, it was Ecuador’s turn, then came Argentina, followed by Suriname, then Belize, then Suriname again and Suriname one more time.

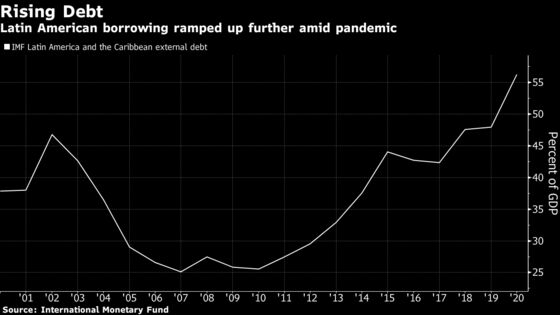

In all, more than $80 billion of foreign bonds have been restructured. And there’s more pain to come.

Traders are almost certain three of those countries will default yet again, bond prices suggest, and the fourth, Ecuador, is far from financial stability. Then there’s the case of Venezuela, which has been mired in default for so many years that creditors have resigned themselves to recouping just a tiny fraction of their money, if anything.

All of which makes the current moment feel a bit like a flashback to the Lost Decade of the 1980s, when Latin America’s heavily indebted countries sank into default one after another and their economies fell into protracted recessions that deepened poverty. While this time is unlikely to be as bad -- in part because rising commodity prices are providing a financial lift -- no bond market in the developing world has been upended in the pandemic quite like Latin America’s.

Buffeted by never-ending waves of Covid-19 and economic paralysis, the region has become Exhibit A in the study of how the virus has deepened the divide between the rich and poor nations of the world. The region’s plight is adding a sense of urgency to the calls in policy circles in Brussels and Washington to provide more relief to developing nations after the Group of 20 leading countries put a temporary moratorium on certain debts. In June, the board of the International Monetary Fund will consider a proposal to free up an additional $650 billion to lend to struggling countries.

Siobhan Morden, a Wall Street analyst who’s specialized in emerging-market debt for the past three decades, says the economic fundamentals in Latin America are so weak right now that “even the strongest countries are struggling.”

“It is a difficult dynamic,” says Morden, who runs Latin America fixed-income strategy at Amherst Pierpoint. On the one hand, bond investors are demanding fiscal restraint to ensure long-term debt sustainability while on the other, governments are eager to ramp up spending on much-needed social and medical programs. “The two are incompatible.”

“Rating agencies and bond vigilantes are quite nervous about repayment risk,” Morden says, “and that has a lasting impact.”

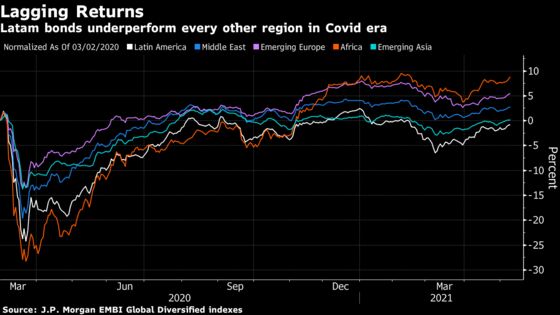

Dollar bonds issued by Latin American governments are the worst performers of any emerging-market region tracked by JPMorgan Chase over almost any recent time period, including a 3.1% loss this year. The region’s stocks, tracked by MSCI, follow a similar trend going back as far as a decade. And several of its currencies are among the biggest decliners in the developing world this year.

A recent HSBC survey of money managers illustrated how gloomy the mood is. Of the 164 surveyed, just 43% said they had overweight positions in Latin America, down from 70% in January. And it was the only region where net sentiment was negative on local currencies, external bonds and equities.

To be clear, the countries that defaulted have long had weak finances, and few analysts see the region’s top economies -- Brazil, Mexico, Chile, Colombia, Peru -- sinking into financial crisis any time soon. They have solid hard-currency reserves, access to debt markets that global central bankers flooded with cash, and they’re benefiting from soaring global demand for their commodity exports.

But even in these nations, signs of stress and strain are mounting.

Chilean assets tumbled recently after workers won permission to tap pensions for the third time since the pandemic began. Peruvian bonds have rebounded somewhat, but are still among the worst in emerging markets this year as a Marxist candidate leads presidential opinion polls. In Colombia, the government’s attempts to increase taxes were met with deadly street protests, forcing policy makers to retreat.

And in Brazil and Mexico, the region’s two powerhouses, the cost for the government to borrow in dollars has jumped relative to peer countries in other parts of the world.

The two countries have been ravaged by Covid-19. Combined, they’ve lost over 600,000 lives. As a whole, the region has accounted for a third of all deaths even though it only makes up 8% of the global population. The pandemic worsened inequality and poverty, especially among women, while also triggering a 7% economic contraction in 2020, more than double the decline of any other region.

To make matters worse, Latin America was already a laggard in global economic growth going into the pandemic. Mired in a prolonged bust following the go-go days of the aughts -- when an unprecedented commodities rally swelled corporate and government coffers -- the region posted an average annual expansion of just 0.8% from 2014 to 2019, a fraction of the average pace for other emerging markets.

So bad were these years that some old Latin American hands had actually taken to referring to this period as the region’s second Lost Decade, following the original one in the 1980s. Seen as such, the region now faces the prospect of back-to-back decades of stagnation.

Bill Rhodes remembers the first Lost Decade well.

He was one of Citibank’s top bankers in Latin America at the time and he played a big role in the debt restructuring framework -- eventually known as the Brady plan -- that was hashed out.

Some things were very different back then. Benchmark interest rates in the U.S. had soared above 10%, compared to the near-zero rates of today. This effectively had cut developing nations off from international financing. And most of the debt was in the form of loans from banks like Citibank -- the predecessor to Citigroup -- instead of the bonds of today.

| Read more on the restructurings: |

|---|

|

|

|

|

But when Rhodes looks at the impact that Covid has had on the region, he sees enough similarities between now and then to justify the use of the term, or to at least warn of the possibility.

“It’s worse than in any other area in the world,” said Rhodes, who spent five decades at Citi. “That’s a very real point that people don’t pick up on enough.”

©2021 Bloomberg L.P.