Silver's Overlooked Rally May Put Gold in the Shade

(Bloomberg Opinion) -- It’s not only gold that glitters. Since touching its weakest level in more than a decade in March, silver has doubled to a seven-year high of almost $23 an ounce. Partly, it’s a rally fueled by the same low-yield, weak-dollar haven dynamic that has pushed bullion to within spitting distance of a record. Investor demand is booming and silver — which is the best conductor of electricity — has industrial uses, too. Short-term supply, meanwhile, has been dented by pandemic-related closures. The metal can keep shining.

Silver tends to loosely track gold. Like the yellow metal, it is benefiting from investors’ jangled nerves, with the global economic recovery looking slow and further coronavirus outbreaks almost certain. Rock-bottom borrowing rates have also reduced the opportunity cost of holding a non-interest-bearing asset, and there’s no sign of a change.

Investor demand is responsible for much of this accelerated rally. This year alone, exchange-traded funds have increased their gold holdings by more than a quarter to surpass 106 million ounces, according to data compiled by Bloomberg, taking the total value to almost $200 billion. Silver holdings have climbed 40%, to more than 850 million ounces. In the futures market, net managed money long positions are climbing back toward levels seen at the end of 2019. The Silver Institute, meanwhile, estimates retail bullion coin sales jumped by an estimated 60% in the first half from a year earlier. Speculative interest in China, which helped drive silver to all-time highs in 2011, is also showing signs of life.

Demand from other quarters is less dramatic, though still encouraging. It helps that silver has a range of applications, unlike gold, which is generally too expensive for industrial uses. Not all are growing: Appetite from photography has ebbed since the advent of the digital camera, while the consumer electronics and automotive sectors have suffered from the squeeze the pandemic has put on households. Yet silver jewelry is expected to drop less than gold, given its relative affordability. Solar panels, meanwhile, should benefit from green-tinged recovery efforts — photovoltaic cells account for about a fifth of silver’s industrial demand. China is the world’s biggest solar power market, and will increase installations this year, despite the slow start to 2020. The country’s silver imports have been running above average. Longer term, the advent of next-generation telecoms technology will help, too.

All the while, supply has been severely disrupted by coronavirus closures and other containment measures, particularly in Peru and Mexico. The Silver Institute earlier this month put the expected drop in mine production at 7% for 2020, even after recent restarts.

The issues go beyond the pandemic. Output has been trending lower in recent years, with large primary-silver mines aging and new ones holding less of what is one of the world’s rarest metals. Silver is usually a byproduct, meaning most production comes from mines that primarily dig out zinc, lead, copper or gold. That’s good news for miners like Mexico’s Fresnillo Plc, with large primary silver operations. Despite marginal increases expected from 2021, rivals can’t simply crank up production in response to higher prices. At a time of tight exploration budgets, a little shiny silver can’t make up for plenty of lackluster zinc.

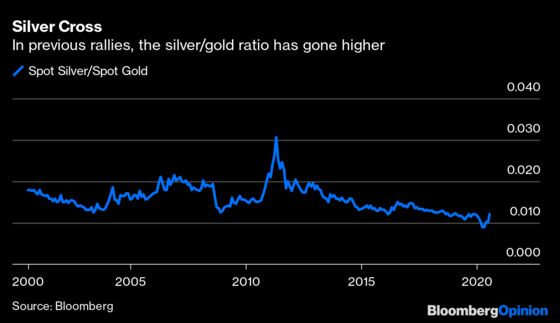

Comparing silver with gold suggests the rally has further to run. The silver-gold price ratio, currently around 1.2%, is edging closer to its long-term average of around 1.5%, according to analyst Vivek Dhar at Commonwealth Bank of Australia. He points out previous sharp run-ups in silver have seen the ratio climb to 2.2% or 2.4 before retreating%. That leaves room for silver to keep shining.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Clara Ferreira Marques is a Bloomberg Opinion columnist covering commodities and environmental, social and governance issues. Previously, she was an associate editor for Reuters Breakingviews, and editor and correspondent for Reuters in Singapore, India, the U.K., Italy and Russia.

©2020 Bloomberg L.P.