Signs of U.S. Growth Overheating Missing as Fed Eyes Rate Hikes

Signs of U.S. Growth Overheating Missing as Fed Eyes Rate Hikes

(Bloomberg) -- The American job market looks hot. Some parts of the economy do not.

That’s the dilemma facing the Federal Open Market Committee as it prepares a likely interest rate increase in two weeks -- the Federal Reserve’s ninth hike in three years -- and to signal more to come in 2019.

With recent declines in stocks, cheaper oil, softening house prices and falling long-term bond yields, the world’s largest economy is downshifting after a few quarters of above-average growth fueled by higher government spending and tax cuts. Faced with the slowdown and a central bank that’s still raising rates, President Donald Trump may be asking a fair question with his Fed criticism: Where are signs the economy is too hot?

“In the absence of any evidence of overheating, it’s hard to see why the FOMC would want to raise rates above neutral and risk slowing the economy even more than it is already likely to slow on its own given the waning fiscal stimulus,” said Roberto Perli, a partner at Cornerstone Macro LLC in Washington and a former Fed economist.

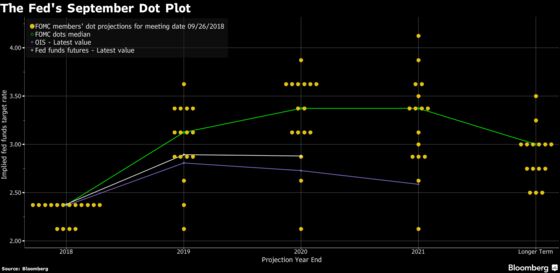

Perli’s reference to a neutral rate is Fed parlance for the policy setting that’s neither boosting nor slowing growth. Right now, with the federal funds rate at 2 percent to 2.25 percent, Fed officials are split about whether they’re as little as one or as many as five rate hikes under neutral.

Staying below neutral is the equivalent of stepping on the monetary accelerator. Going above it means applying the brakes.

Fed Chairman Jerome Powell said last week the Fed was nearing the range of estimates that represent a neutral setting.

As the U.S. expansion edges closer to the longest on record next year, some interest-rate sensitive parts of the economy -- autos and housing, in particular -- are showing signs of weakness. Growth averaged close to 4 percent in the past two quarters, the fastest back-to-back pace since 2014, boosted by a $1.5 trillion tax overhaul and a $300 billion spending increase.

Yet some companies aren’t feeling the boom times. General Motors Co. said Nov. 26 it will cut 14,000 salaried and factory workers and close seven factories worldwide by the end of next year.

Luxury homebuilder Toll Brothers Inc. reported Tuesday its first drop in orders since 2014. In California, which is facing an affordability crisis and a decline in foreign demand, orders fell 39 percent.

Powell has emphasized the overall U.S. economy is strong, and the outlook is favorable despite pockets of weakness. The Fed bases its rates forecasts on its outlook for the economy, and the tightening now is aimed at preventing excesses from occurring a year or more down the road.

“You don’t need to worry about overheating to rationalize the rate hikes to date,” former Fed Vice Chairman Alan Blinder said. “Up to now, the Fed is just stepping less hard on the gas pedal.”

If there is a market that’s nearing a boil, it’s the job market, with an the unemployment rate at half-century low of 3.7 percent. While employers have cited shortages of qualified skilled workers, wage gains have been moderate and there’s no indication they are feeding into inflation.

“The Fed can’t sit and wait until wages and prices overheat,” said Stephen Stanley, chief economist at Amherst Pierpont Securities LLC.

That’s not evident in prices. The Fed’s preferred measure of inflation met its 2 percent target in October, though excluding volatile food and energy, the core measure rose 1.8 percent. A plunge in oil is likely to weigh on price measures in the fourth quarter.

The Fed is also monitoring financial markets and asset prices, which helped trigger the past two recessions.

A Fed report last week said it viewed financial-stability concerns as moderate, citing commercial real estate, corporate debt and leveraged loans among the potential issues. Downturns in 2001 and 2008 were ultimately the result of financial excesses rather than inflation.

“There is a less traditional kind of overheating that worries the Fed, which is financial excesses, especially non-financial corporate borrowing,” said Jonathan Wright, an economics professor at Johns Hopkins University in Baltimore and a former Fed economist. “The Fed is acutely aware that the overheating that ended the last two cycles was in finance, not in wages and prices.”

To contact the reporter on this story: Steve Matthews in Atlanta at smatthews@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull

©2018 Bloomberg L.P.