Shorter Is Better Is Mantra for Malaysia Bonds as Deficit Widens

Shorter Is Better Is Mantra for Malaysia Bonds as Deficit Widens

(Bloomberg) -- It pays to be choosy about where you put your money in Malaysian bonds.

The debt market as a whole has a number of positives: a dovish central bank, attractive real yields, and buoyant demand from cashed up local banks. While accommodative policy will directly bolster shorter maturities, investors should be wary about longer tenors though due to the widening budget deficit.

The rising tide of overall interest can be seen in recent bond auctions. A sale of three-year notes last week drew a bid-to-cover ratio of 2.5 times, the highest at any offering of conventional debt this year, and up from the average of 2.1 times over the past three months. This was despite the issue size climbing to 5 billion ringgit ($1.2 billion), the largest for 2020.

Demand is being driven by onshore banks, many of which are flush with liquidity due to falling demand for loans, analysts say. Foreign interest has also been picking up, with overseas investors pouring in a net $1.8 billion in June, the highest in more than three years. Global participation still has room to increase, given investors abroad withdrew $3.8 billion in the first quarter amid the coronavirus shock.

Despite bond yields being close to record lows, persistent deflation means fixed-income securities remain attractive. Malaysia has already seen three months of falling prices, with signs pointing toward an extension of this trend when June data are released on Wednesday. A 1% drop in prices is estimated for this year, according to a Bloomberg survey of economists.

The main plus point for shorter maturities is the accommodative central bank. The economic outlook remains susceptible to “downside risks,” policy makers said in their July 7 statement, hinting at the prospect of additional interest-rate cuts on top of the 100 basis points they have already delivered this year. The World Bank forecasts Malaysia’s economy will shrink 3.1% this year, after revising its earlier estimate of a contraction of 0.1%.

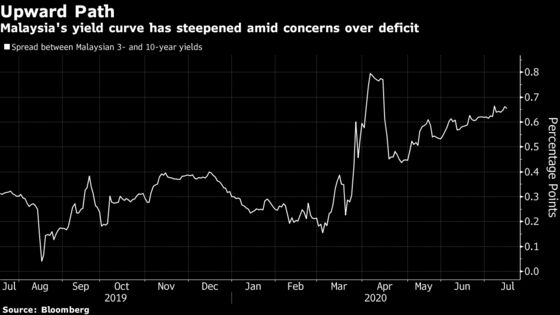

While longer-maturity bonds have rallied along with shorter tenors, the yield curve has been steepening amid concern over the fiscal deficit. The government predicts the budget shortfall will swell to a decade-high 5.8% to 6% of gross domestic product this year as it boosts spending to counter the impact of the pandemic. This is fueling discussion about whether the government will breach its self-imposed debt-ceiling limit of 55% of GDP.

All things being taken into account, there are a number of things to like about Malaysian bonds -- investors just have to make sure they hit the right spot.

What to Watch

- The Philippines will release balance-of-payments data for June on Monday, and Malaysia will announce inflation data for the same month on Wednesday

- Thailand will sell 30 billion baht ($947 million) of five-year bonds (LB24DB) and 5 billion baht of 50-year debt (LB676A) on Wednesday. An auction of the 20-year securities this week drew a bid-to-cover ratio of 2.37, the highest in two months. The nation will publish trade data the same day

- Bank Indonesia announced that it will be shortening the domestic non-deliverable forward auction window to 5 minutes from 15 minutes effective July 20

Note: Marcus Wong is an EM macro strategist who writes for Bloomberg. The observations he makes are his own and not intended as investment advice.

©2020 Bloomberg L.P.