Sell Treasuries on Bet Market Wrong About Fed, Aberdeen Says

Aberdeen is shorting U.S. two-and five-year notes on expectations growth in the world’s biggest economy will remain robust.

(Bloomberg) -- Aberdeen Standard Investments is selling Treasuries in a bet investors are wrong to predict the Federal Reserve will cut interest rates this year.

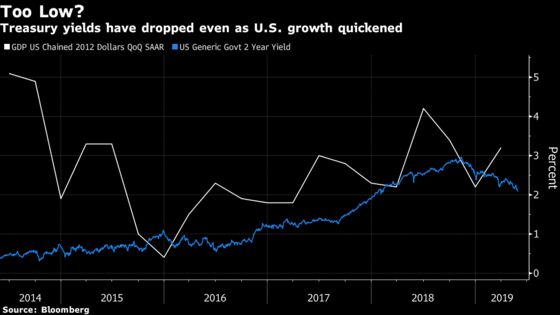

The fund manager is shorting U.S. two- and five-year notes on expectations growth in the world’s biggest economy will remain robust, according to Adam McCabe, Singapore-based head of fixed-income for Asia and Australia. Aberdeen’s conviction comes even as Treasury 10-year yields have dropped to the lowest since 2017 and a key part of the yield curve has inverted, signaling the U.S. may be headed for a recession.

“Economic conditions in the U.S. are resilient and there’s no compelling case at the moment for the Fed to ease monetary policy,” said McCabe at Aberdeen, which oversees $643 billion. “The hurdle that the Fed will have to jump to ease is quite high.”

Treasuries have led gains in global bonds this week as U.S.-China trade tensions and political risks in Europe sent investors scurrying for the safest assets. Benchmark 10-year yields fell as low as 2.21% Wednesday, the least since September 2017, while two-year yields slipped to 2.05%, down from 2.97% as recently as November.

Traders are ratcheting up bets major central banks will need to ease policy to stimulate the global economy. Markets are now fully pricing in three Fed rate cuts by the end of next year, according to fed fund futures.

Bullish Views

Aberdeen’s view is at odds with that of Bank of America Merrill Lynch, which sees Treasury 10-year yields falling as low as 2.05% by December. Antares Capital predicts the benchmark may slide toward 2% due to the U.S.-China trade war, while Morgan Stanley says the inverted yield curve is clearly signaling a downturn.

Still, recent data backs Aberdeen’s case that the economy is motoring along nicely. U.S. economic growth accelerated to 3.2% in the first quarter, beating Wall Street forecasts, while the jobless rate dropped to 3.6% last month, the lowest level in almost 50 years.

“If the Fed doesn’t ease monetary policy, it’s hard to sustain the levels of yields that the market’s currently pricing,” McCabe said. “I’d be expecting toward year-end, yields to reach 2.7% to 2.75%” for 10-year notes, he said. The yield climbed one basis point Thursday to 2.27%.

While Aberdeen is negative on Treasuries, it is buying Chinese government bonds on expectations the central bank will loosen financial conditions to stimulate growth.

Overweight China

The People’s Bank of China said this month it would cut its reserve requirement ratio to release 280 billion yuan ($41 billion) of longer-term funds by lowering the proportion of deposits smaller banks need to lock away.

We’re been structurally overweight China bonds,” McCabe said. “It’s a market that’s going to exhibit low correlations to the U.S., largely because the policy direction is very much one of supporting global liquidity.”

Here are some more of McCabe’s investment views:

- Fund is buying Philippine bonds as central bank re-establishes policy credibility

- Poised to purchase Indonesian debt after 175 basis points of central bank rate hikes last year

- Sees Reserve Bank of Australia keeping rates at 1.5% in June. Cutting too soon may imply it is reacting to weaker property prices rather than broader economic conditions

To contact the reporter on this story: Ruth Carson in Singapore at rliew6@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Nicholas Reynolds

©2019 Bloomberg L.P.