Russia Ready to Buy Own Debt If Sanctions Spark Market Crash

Russia Ready to Buy Own Debt If Sanctions Spark Market Crash

(Bloomberg) -- Russia is ready to take the emergency step of buying its own ruble debt if a new wave of U.S. sanctions threatens to upend the market.

“In a very stressful scenario when we see the conditions of a market failure” both “the central bank and the government have the tools to intervene on the open market to cushion the adjustment period,” Deputy Finance Minister Vladimir Kolychev said in a Bloomberg TV interview.

A coordinated response would be a first since the Finance Ministry and the Bank of Russia teamed up early in 2015 to support the ruble at the height of the country’s currency crisis. As turmoil spreads across emerging markets, Russian assets have been battered by harsh U.S. sanctions in April and a “nuclear” option proposed in Congress that could target sovereign debt.

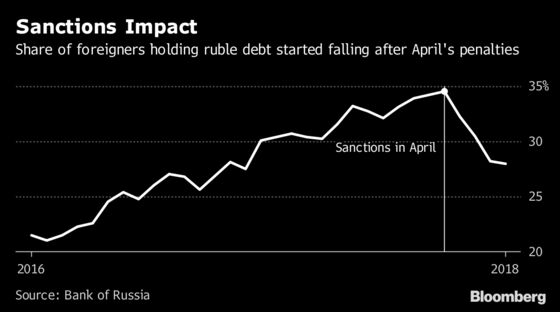

Foreign holdings of sovereign ruble debt have since declined to the lowest since 2016. The securities have handed investors a 12 percent loss since July, the fourth-worst performance among Russia’s peers tracked by Bloomberg. The ruble stabilized against the dollar Thursday, near the weakest level since April 2016, while yields on 10-year debt rose five basis points to 8.94 percent.

The share of non-residents in Russia’s ruble-denominated debt has fallen to 26-27 percent, according to Kolychev. That’s down from a peak of 34.5 percent in March and 28 percent in July, central bank data show.

Despite the threat of the harshest U.S. measures to date, officials say Russia is prepared for the worst. At a forum sponsored by the ministry in Moscow on Thursday, Kolychev and colleagues from the central bank, Economy Ministry and a big state bank downplayed the risks from painful new measures, arguing that Russia’s in a strong position to weather any further instability.

Rising Costs

The U.S. Senate is set to debate new sanctions to punish the Kremlin for alleged election meddling, including a raft of measures dubbed “the bill from hell” that could bar Americans from buying new issues of Russian sovereign debt and ban the largest state banks from using dollars.

If U.S. actions forced foreign investors to sell Russian debt, Kolychev said in the interview that the first move would be to halt new issuance to keep pressure from building in the market.

The Finance Ministry canceled a bond auction on Wednesday, the second time in recent weeks, amid rising borrowing costs. In another sign of increasing volatility, the governor of the Bank of Russia said policy makers at next week’s meeting will consider the first increase of the key interest rate since 2014 as inflationary risks grow due to the ruble’s weakness.

Cushion Volatility

The ministry will decide about buying back domestic bonds if volatility is several times higher than normal, among factors such as demand and liquidity, and had no limit on volumes, Kolychev said Thursday. There’s been no discussion of support for Eurobonds but Russia could stabilize that market if needed, he said.

Even if the U.S. targets Russia’s biggest state lenders, such as Sberbank PJSC, private banks can continue to carry out dollar transactions, Kolychev said in the interview. And the government can “cushion short-term volatility and provide the necessary liquidity in local currency and foreign currency to continue to process transactions in international trade, he said.”

The government has 3 trillion rubles ($44 billion) of liquid assets, including deposits with lenders and funds in central bank accounts, enough to last to the end of 2019, Kolychev said. The Finance Ministry may not sell the full amount of debt in its borrowing plan for the year if the market conditions remain unfavorable, he said during the interview.

“What’s important is we have buffers in terms of cash liquidity that could allow us to be flexible,” Kolychev said. “We don’t actually have to borrow into a stressful environment."

--With assistance from Nejra Cehic, Andrey Biryukov and Evgenia Pismennaya.

To contact the reporters on this story: Olga Tanas in Moscow at otanas@bloomberg.net;Anna Andrianova in Moscow at aandrianova@bloomberg.net;Jake Rudnitsky in Moscow at jrudnitsky@bloomberg.net

To contact the editors responsible for this story: Gregory L. White at gwhite64@bloomberg.net, Torrey Clark, Paul Abelsky

©2018 Bloomberg L.P.