Ruble at Mercy of Sanctions as Russian Defenses Show Cracks

Ruble Left at Mercy of Sanctions as Russian Defenses Show Cracks

(Bloomberg) -- Move over, Elvira Nabiullina.

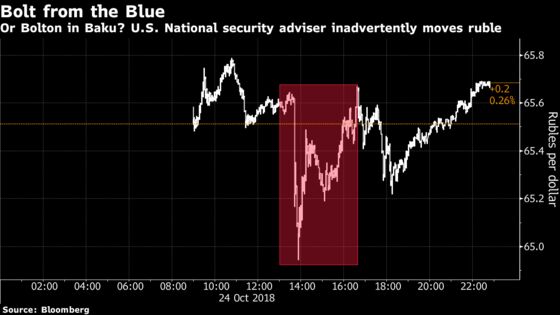

While the Russian central bank governor’s interest-rate decision on Friday created barely a ripple in the currency market, U.S. National Security Adviser John Bolton gave ruble traders a case of whiplash two days earlier.

Merely the appearance that Bolton was striking a conciliatory tone on sanctions was enough to catapult the ruble on Wednesday from losses to an intraday gain of almost 1 percent. But once it became clear his comments from Azerbaijan weren’t so optimistic, the speculation Washington might hold off on further penalties rapidly evaporated, leaving the currency down for a second day against the dollar.

As central bankers filed into Friday’s meeting in Moscow, the ruble’s sensitivity also raises the question of just how much the measures of support deployed at the last gathering have accomplished.

The Bank of Russia patted itself on the back, saying in a statement accompanying their latest rate decision that suspending foreign-currency purchases helped the domestic financial market’s “stabilization in the second half of September and in early October, with exchange-rate volatility declining.”

Indeed, halting the program and surprising markets with the first rate hike since 2014 contributed to the ruble’s rebound of over 3 percent since the September decision. But as much as half the appreciation came from a weaker dollar, according to ING Groep NV, and the currency remains vulnerable.

Not Immune

“The central bank’s decision to put the foreign currency interventions on hold might have absorbed some Russia-specific pressure on the ruble, but it hasn’t made it immune to global trends,” said Dmitry Dolgin, chief economist at ING in Moscow.

While Nabiullina pledged emergency support last week in the event of a market crisis, Friday’s meeting was a sedate affair. After last month’s unexpected quarter-point increase, the Bank of Russia kept its benchmark on hold at 7.5 percent as predicted by all but two of the 41 economists surveyed by Bloomberg.

Plenty of risks still linger for the ruble. As the U.S. midterms approach, lawmakers continue to mull sanctions that could ban investors from buying Russia’s new sovereign bonds and impose limits on its banks.

Benchmark Brent’s retreat from $80 has also put the currency of the world’s biggest energy exporter on track for its first weekly drop in three against a backdrop of global market ructions. The price of a barrel of Brent crude in ruble terms is the lowest since August.

The ruble traded 0.5 percent weaker at 65.9025 per dollar as of 5:11 p.m. in Moscow on Friday, set for a 0.6 percent drop in the week.

Further down the line, the central bank has said it will make up for the foreign-currency purchases it skipped during the pause. That could mean additional ruble stress as the government returns to topping up reserves.

But for some economists, the decision on currency purchases says something more worrying about the central bank’s attitude to the ruble.

Red Lines?

Hitting the pause button implies the existence of red lines for the exchange rate beyond which the currency won’t be allowed to weaken, according to Vladimir Tikhomirov, chief economist at brokerage BCS Financial Group.

Back in 2014, when the first round of U.S. and European Union sanctions helped send Russian markets into a tailspin, the central bank intervened heavily to support the ruble before ultimately letting the currency trade freely. Since then, it’s pledged to avoid interventions unless the ruble’s swings threaten financial stability.

Policy makers insist they’re allowing the market to determine the exchange rate and have explained their pause of foreign-currency purchases as an effort to steady the ruble. Nabiullina has said a decision to resume the program will depend on volatility and not the ruble’s exchange rate.

Still, there may have been an element of smoke and mirrors to the last rate decision, according to Natalia Orlova, chief economist at Alfa-Bank.

“The decision to raise the key rate looks like a cover-up,” Orlova said. “It allowed them to distract attention from the announcement on halting the FX purchases and to create the impression that the central bank is regulating the economy with the help of interest rates.”

--With assistance from Zoya Shilova, Anna Andrianova and Torrey Clark.

To contact the reporter on this story: Evgenia Pismennaya in Moscow at epismennaya@bloomberg.net

To contact the editors responsible for this story: Gregory L. White at gwhite64@bloomberg.net, ;Dana El Baltaji at delbaltaji@bloomberg.net, Alex Nicholson, Paul Abelsky

©2018 Bloomberg L.P.