Risks Central Bank Can't Ignore in India's Low Inflation Spell

India’s headline inflation data may be subdued for now, but there are mounting risks that are difficult to ignore.

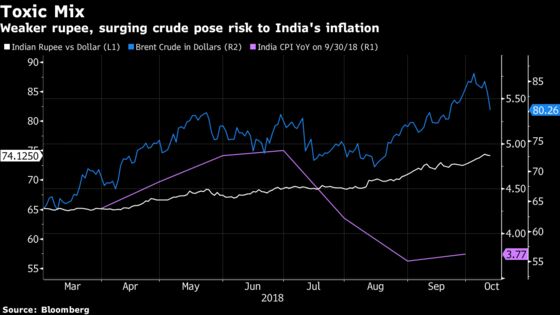

(Bloomberg) -- India’s headline inflation data is subdued for now, but there are mounting risks that are difficult to ignore: a currency at a record-low, high oil prices, and looming elections that’s prompting the government to raise food prices to placate farmers.

Consumer prices rose 3.77 percent in September from a year earlier, the Statistics Ministry said in a statement on Friday. That pace is well within the target set by the Reserve Bank of India. The median of 39 estimates in a Bloomberg survey of economists was for a 4.02 percent gain.

Inflation within the targeted range and signs that demand may be cooling in the world’s fastest-growing major economy prompted the central bank to keep interest rates on hold last week, and lower the forecast for gains in consumer prices. The RBI expects inflation in the range of 3.9 percent to 4.5 percent in the second half of the fiscal year to March 2019, down from 4.8 percent projected earlier.

“The rise in crude oil prices, the sharp weakening of the rupee, and the revision in minimum support price for farmers are likely to push up the headline inflation above 4 percent in the ongoing quarter,” said Aditi Nayar, principal economist at ICRA Ltd. “These risks, combined with the change in stance from neutral to calibrated tightening, suggest a likely rate hike in the December 2018 policy review,"

The Monetary Policy Committee’s change to a more hawkish stance comes amid concerns that surging oil and volatile financial markets could add to price pressures and offset the comfort from falling food prices.

Details

- Food and beverage prices rose 1.1 percent

- Clothing and footwear prices rose 4.6 percent

- Fuel and lighting prices rose 8.5 percent

- Housing prices rose 7.1 percent

| What Our Economists Say... |

| Weaker than anticipated inflation data over the past few months suggests that the change in RBI’s policy stance to calibrated tightening was rather premature and only highlights the central bank’s hawkish bias. In our view, as long as inflation continues to undershoot, it is likely to counter the central banks hawkish bias in favor of a hold. -- Abhishek Gupta, Bloomberg Economics |

India, which imports more than 80 percent of its oil needs, is vulnerable to increasing crude prices. Together with the rupee, Asia’s worst-performing major currency this year, this worsens the outlook for inflation and the current-account gap. Besides, the government’s move to raise support prices for farm produce will add to the inflationary pressures.

According to the central bank, a 20 percent increase in the price of the Indian basket of crude to $96 a barrel would dent growth by 30 basis points and stoke inflation by 40 basis points. The price of Brent crude, the benchmark for half the world’s oil, is hovering above $80 per barrel as impending American sanctions squeeze Iranian exports and an economic crisis in Venezuela disrupts supplies.

“We do not think that the RBI’s rate-hike cycle has come to an end,” said Sujan Hajra, chief economist at Anand Rathi Financial Services Ltd. “Yet, with the real policy rate at 250-300 basis points, headroom for the RBI to carry out rate hikes is limited unless inflation crosses 5 percent consistently.”

--With assistance from Anirban Nag and Manish Modi.

To contact the reporter on this story: Vrishti Beniwal in New Delhi at vbeniwal1@bloomberg.net

To contact the editors responsible for this story: Nasreen Seria at nseria@bloomberg.net, Karthikeyan Sundaram, Unni Krishnan

©2018 Bloomberg L.P.