Riksbank U-Turn Stokes Sweden Rate-Hike Suspense: Decision Guide

Riksbank U-Turn Stokes Sweden Rate-Hike Suspense: Decision Guide

(Bloomberg) -- Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

The Riksbank may be about to complete one of the most dramatic monetary policy shifts since Stefan Ingves first took charge of Sweden’s central bank in 2006.

Less than three months since its officials stood out from the tightening trend of global counterparts by effectively ruling out interest-rate hikes before 2024, investors are poised for just such a move to transpire on Thursday.

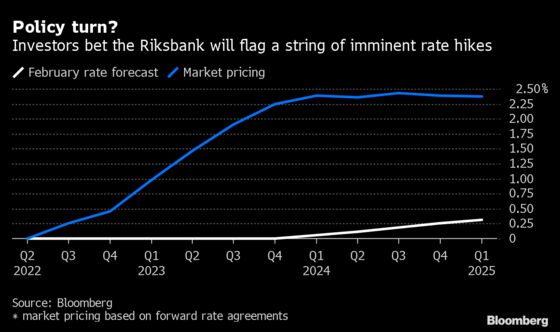

Economists are less convinced that will happen, though they reckon that even no change at this week’s Riksbank decision will be accompanied by a forecast warning of an imminent series of borrowing-cost increases to act against inflation.

The central bank’s composure of defiance crumbled in mid-March, when the governor, Ingves, acknowledged that an environment of “far too high” price increases meant rates would probably need to rise sooner than previously signaled. Subsequently, three more officials publicly admitted the need to change course.

“This is about showing that they take price increases seriously,” Thomas Pohjanen, who manages the Excalibur Fixed Income hedge fund, said. “My interpretation of the comments from Riksbank board members is that they feel that it’s better to start hiking soon, accept that they were wrong in February, and rip off the band aid.”

Pohjanen believes it is likely that the Riksbank will choose to hike already this week, but acknowledges it is a close call. That move, he said, should be accompanied by a reduction of the bank’s asset portfolio, and followed by further rate increases.

“I think a series of hikes are needed, and that it’s too cautious to only talk about 25 basis points now and 25 basis points later this year,” he said. “I wouldn’t be surprised if they would increase the rate at five or six straight policy meetings.”

Collectively, investors are pricing in close to a full 25-basis point hike on Thursday from the policy rate’s current level of zero. By contrast, only 2 out of 18 economists surveyed by Bloomberg expect such a move so soon.

| Bank | Forecast for Riksbank Policy |

|---|---|

| Danske Bank | First hike in June, but April is “a close call” |

| DNB | Hikes in June, Sept. and Nov. |

| Handelsbanken | First hike in June, policy rate peaking at 1.25% in 2024 |

| Morgan Stanley | Hikes in June, Sept., Nov., Feb., then wait-and-see mode |

| Nordea | Hikes in June, Sept. and Nov. |

| SEB | First hike in June, followed by 4 more in 2022-2023 |

| Swedbank | First hike in April, policy rate at 1.5% by April 2023 |

Whatever the Riksbank does to its policy rate this week, all eyes will be on what it says about hikes going forward. Market pricing indicates it could start a series of nine or ten increases, bringing borrowing costs to their highest level in close to 14 years.

While Ingves recently said taking the policy rate to 2.5% would be doable, economists question whether the Riksbank is willing to risk the impact on the country’s indebted households that such a shift would entail.

“The economic effects of such aggressive hikes could be dramatic,” Svenska Handelsbanken’s Johan Lof said. “We still foresee a hiking pace that is more in keeping with the Riksbank’s announcement of a gradual tightening of monetary policy than that being priced in by the market.”

For now, the Riksbank’s challenge on inflation is pressing. The central bank’s target measure, CPIF, rose to 6.1% in March. Much of that is driven by higher costs for fuel, electricity and supply shortages, factors that make it unlikely that the 2% goal will be met in the months ahead.

Some observers argue that the central bank’s U-turn is rash. Alexander Onica, a portfolio manager at Skandia Investment Management, reckons that as inflation is largely due to factors beyond the Riksbank’s control, the only thing a rapid shift in policy could accomplish now is to curb prices by slowing down the economy.

“The fact that an institution of that size and magnitude makes such a move just underlines that they are not in charge,” he said. “The oil price is in charge, and when central banks try to control oil prices by using policy rates, there is a risk that it doesn’t end well.”

| Read More... |

|---|

|

©2022 Bloomberg L.P.