The Emerging Markets Rally Is About to Be Tested

A slew of factors are likely to test the resilience of the rally in Emerging Markets.

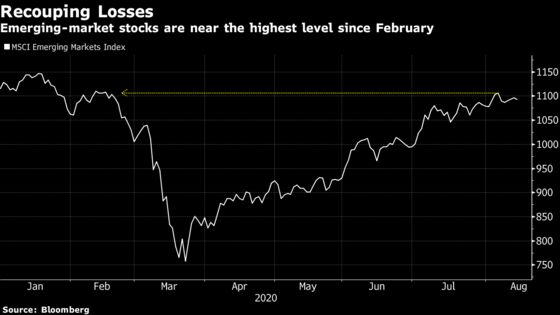

(Bloomberg) -- The emerging-market rally that has all but wiped out the losses since the start of the coronavirus pandemic looks headed for a late-August reappraisal amid a resurgence of trade tensions and delays to U.S. stimulus.

Indexes of stocks, currencies and domestic bonds rose in tandem last week, with the MSCI equity gauge clocking up its longest sequence of weekly gains since January, even as idiosyncratic risks across developing nations mounted. Russia and Mexico led inflows to emerging-market exchange-traded funds. China’s retail sales and industrial production data missed estimates, Malaysia’s and Thailand’s economies shrank the most since the Asian financial crisis, Brazil suffered a fresh bout of political turmoil and Turkey struggled to shore up the lira.

That resilience may now be tested as U.S.-China relations worsen in the run-up to America’s presidential election. President Donald Trump on Friday ordered the Chinese owner of the popular music video app TikTok to sell its U.S. assets, as both countries postponed talks planned for the weekend aimed at reviewing progress on the phase-one trade deal. Meantime, Taiwan formally signed an agreement to buy F-16 jets built by Lockheed Martin Corp., a move likely to be denounced by Beijing.

“Markets will begin to price more caution given the upcoming volatile U.S. election, and particularly if U.S.-China animosities do not ebb away,” said Ehsan Khoman, the head of Middle Eastern research at MUFG Bank in Dubai.

Uncertainty about whether further U.S. government stimulus will be enacted, with negotiations still in deadlock, may also sap risk appetite in the coming days. Minutes of the Federal Reserve’s July meeting due Wednesday will probably offer clues on what the central bank’s next steps may be to increase policy accommodation.

“The sharp rally in risk markets leaves less obvious upside,” Morgan Stanley New York-based strategist Michael Zezas wrote in a note. “Another round of stimulus is the difference between ensuring that the economic recovery continues uninterrupted and a meaningful short-term pullback in growth. It may also be the difference between a confident six- to 12-month view on a variety of risk assets and a meaningful near-term correction.”

While traders will focus on interest-rate decisions in Indonesia and the Philippines this week, the most significant policy meeting may be in Turkey, where the central bank has resorted to backdoor monetary tightening to anchor the lira. The currency has depreciated more than 5% versus the dollar this month.

Listen: EM Weekly Podcast: Central Banks’ Conflicting Pressures

Stealth Tightening

- Torn between market pressure to raise borrowing costs and President Recep Tayyip Erdogan’s persistent calls to lower them, Turkey’s central bank will probably keep the one-week repo rate unchanged at 8.25% on Thursday

- The central bank now tweaks the cost of funding on a daily basis, modifying the amount of liquidity available to lenders across its various interest rates, following the currency’s slide to a record low

- Derivatives traders pared their bearish wagers against the lira last week, according to one-month risk reversals

- Read: Turkey’s Central Bank Is in a Bind Ahead of Rates Day: Eco Week

- Read: Turkey Stands Alone in Emerging Markets as Economic Woes Deepen

Indonesia, Philippines Decide

Bank Indonesia is forecast to leave interest rates on hold Wednesday, with policy makers aware that cutting borrowing costs further risks adding to the rupiah’s recent losses

- The central bank issued several statements last week saying it was intervening to prevent currency depreciation. Policy makers may believe they should pause to address concerns over the shift in focus toward domestic stimulus and away from supporting the currency

- This is related to concern that direct support for the budget will likely extend into next year in light of the recession-fighting budget presented on Friday, according to Tamara Henderson of Bloomberg Economics

- At the same time, a rate cut can’t be ruled out. Since BI’s last meeting, second-quarter GDP was weaker than expected and CPI has remained well below target

- The Philippine central bank is also expected to stay on hold Thursday after the governor said there’s no compelling reason for a near-term cut

- This is despite the disappointing GDP figures released earlier this month and the strength of the peso, which was Asia’s best-performing currency last week

- Namibia and Zambia will decide on interest rates on Wednesday, while policy makers in Botswana and Mozambique will decide on Thursday

Mideast Markets

- Equities across the Middle East advanced on Sunday, in the first day of trading after Israel and the United Arab Emirates said they reached an agreement to begin normalizing relations

- On Sunday, UAE-based APEX National Investment said it agreed to conduct research on the coronavirus with Israel’s TeraGroup

- Elsewhere, Bahrain’s bonds may extend this year’s underperformance among Gulf peers after the nation’s debt received its first downgrade in over two years from Fitch Ratings

- The credit assessor said the nation will likely “require further Gulf backing” in the medium term as the government’s finances remain under strain

Other Data and Events

- Indonesia’s current-account balance due on Tuesday is likely to show sustained improvement in the second quarter. The central bank has referred to the positive trend as giving it more scope to keep cutting rates

- Trade numbers for July will be released on the same day

- Malaysia reports July CPI on Tuesday, with the measure forecast to improve marginally to minus 1.3%

- Malaysian bonds fell last week, after being Asia’s star performers this quarter

- China’s prime lending rates are expected to remain unchanged on Thursday

- Taiwan’s July export orders and second-quarter current account are both due Thursday and are likely to remain resilient

- Implied Taiwan dollar volatility continues to grind lower due to an ongoing stalemate between markets and the central bank

- South Korea’s 20-day exports due Friday will probably show some deterioration after the 10-day measure fell 12.7% year-on-year on a daily average basis

- The won was little changed last week

- Chile is expected to post second-quarter gross domestic product figures on Tuesday that flag the impact of the coronavirus lockdowns

- A report on Argentina’s June economic activity, scheduled for Thursday, will probably show a rebound due to less restrictive lockdowns in Buenos Aires

- Still, it will do little to lift the nation from being among the worst performers in the second quarter, according to Bloomberg Economics

- Budget balance figures for July are expected to be released on Friday.

- Bond investors, meantime, now have until Aug. 28 to accept the terms of a debt-restructuring agreement struck earlier this month

- Mexico’s retail sales data for June, to be posted on Friday, will probably show a sluggish recovery from May and remain below last year’s levels. The peso was the best performer among peers last week

- Investors in Brazil will watch for signs of government fiscal discipline after inconsistent rhetoric from President Jair Bolsonaro

©2020 Bloomberg L.P.