Repo Turmoil Spawns Doubt Fed Is Targeting Right Interest Rate

Repo Turmoil Spawns Doubt Fed Is Targeting Right Interest Rate

(Bloomberg) -- Recent turbulence in U.S. money markets has cast light on a big problem hidden at the root of the Federal Reserve’s conduct of monetary policy: It is targeting an increasingly irrelevant interest rate.

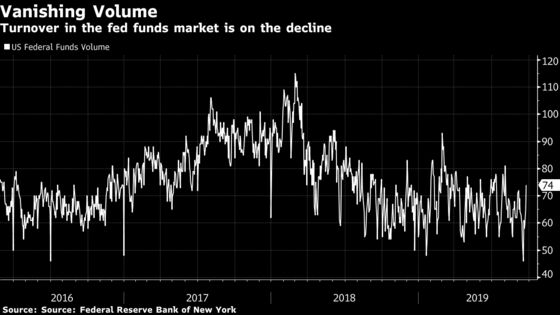

Less than $100 billion changes hands each day in the federal funds market, the overnight interbank rate that the central bank targets. In contrast, considerably more than a trillion dollars are traded daily in the market for repurchase agreements, where financial institutions swap Treasury securities for cash.

“Fed funds is a moribund market,” said Mark Cabana, head of U.S. interest rates at Bank of America Corp. “It does not really represent where banks are truly seeking to lend and borrow.”

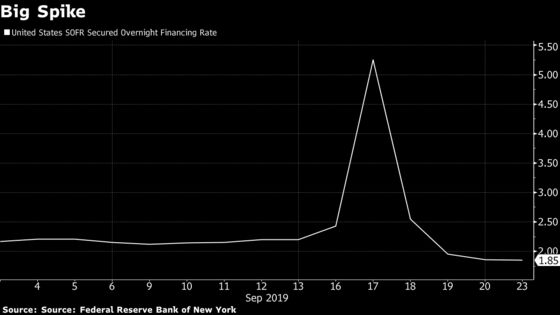

That’s led to calls that the Fed change its framework for carrying out monetary policy. The aim: Lessen the chances of the sort of turmoil that saw repurchase or repo rates soar as high as 10% last week and strengthen the central bank’s control of the short-term money markets that underpin the financial system and the economy.

Read more: N.Y. Fed Takes $75B of Securities in Overnight Repo Operation

The most radical step the Fed could take -- and probably the one that’s least likely at this point -- would be to junk the fed funds target entirely and replace it with an objective for an economically more significant short-term rate.

Among the possible candidates to replace fed funds: The recently minted secured overnight financing rate, a broad daily repo rate measure that the Fed is championing as a new benchmark for contracts on everything from home mortgages to corporate loans. One downside is that, being linked to repo, it too was subject to major spikes during the recent tumult.

A more subtle, yet still potentially significant change that the central bank could make would be to tweak the rules of engagement under which the New York Fed’s Open Market Desk operates in the money market. Instead of being tasked to merely keep the federal funds rate within its target range, the desk could be given greater leeway to respond to pressures elsewhere in the money markets.

While some analysts say the desk may be indirectly doing that already, a more explicit mandate would reassure traders that the Fed is ready to respond promptly to market dislocations even when the funds rate is within its target range.

Speaking to reporters on Sept. 18, Fed Chairman Jerome Powell played down the significance of recent market strains, though he acknowledged that they had been worse than expected.

“While these issues are important for market functioning and market participants, they have no implications for the economy or the stance of monetary policy,” he said.

Before the 2008-09 financial crisis, it made sense for the Fed to target the federal funds rate because that was the market banks used to lend and borrow scarce reserves from each other, with hundreds of billions of dollars changing hands each day.

The market’s dynamics changed, however, when quantitative-easing measures intended to safeguard the economy created vast new bank reserves, lessening the need for institutions to tap interbank liquidity. While some of those reserves have since been extinguished, there are still far more than there were pre-crisis.

That’s left the Federal Home Loan Banks -- a group of government-sponsored lenders -- as the dominant players in the fed funds market, unintentionally giving them outsized influence over where the rate settles.

“It’s too specialized and too small a market,” said Joseph Gagnon, a former Fed official who is now a senior fellow at the Peterson Institute for International Economics. “You want a bigger market” to use for a target.

Fed policy makers discussed alternatives to the funds target at their policy making meeting last November. One that got a lot of air time: The overnight bank funding rate.

Published by the New York Fed, the unsecured benchmark adds eurodollar transactions -- which are largely banks borrowing from non-bank financial institutions, like money-market mutual funds -- and certain domestic deposits to the volume of daily fed funds transactions.

Whereas fed funds breached the Fed’s target range last week, the overnight bank funding rate peaked at 2.25% before retreating.

While OBFR volume is roughly double that of fed funds alone, it is still just a fraction of that in the repurchase market. And it also has been trending lower in recent years.

Rates Primer:

|

Some policy makers at the November meeting “saw it as desirable to explore the possibility of targeting a secured interest rate,” according to the minutes of the gathering.

Peterson’s Gagnon supports targeting the secured overnight financing rate, or SOFR. One ancillary benefit of doing so: It might reassure borrowers and lenders that SOFR will be relatively stable and so make them more likely to adopt it as an alternative to the beleaguered London inter bank offered rate.

The recent turmoil -- which saw SOFR more than double to 5.25% on Sept. 17 -- has raised questions among some market participants about its suitability as a benchmark.

Adoption of a SOFR target though would have some other downsides. It could open up the Fed to accusations that it is protecting hedge funds and other financial institutions active in the repurchase markets, said Scott Skyrm, executive vice president at broker-dealer Curvature Securities.

The central bank may also find it harder to keep the rate within its target range than has been the case with fed funds.

“There’s no perfect substitute” for the current target, said Gennadiy Goldberg, senior U.S. rates strategist at TD Securities.

--With assistance from Liz Capo McCormick and Alexandra Harris.

To contact the reporter on this story: Rich Miller in Washington at rmiller28@bloomberg.net

To contact the editors responsible for this story: Margaret Collins at mcollins45@bloomberg.net, Alister Bull, Sarah McGregor

©2019 Bloomberg L.P.