Reluctant PBOC Seen Limiting Support for China’s Bond Market

Market participants will next be watching how the PBOC handles further batches of medium-term funds that come up for renewal.

(Bloomberg) --

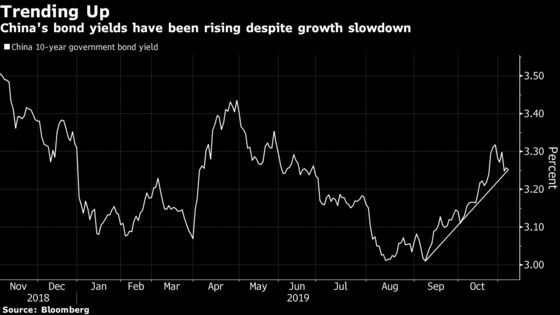

While Tuesday’s move by the People’s Bank of China to trim a benchmark for bank funding costs has helped halt a slide in the country’s bonds, market participants see little scope for more robust moves by the central bank that could offer further support.

That leaves yields, which have climbed the past two months even as economic growth weakened, remaining under pressure -- all the more so with central and local government debt issuance expected to climb. Key to investor concerns is inflation, which probably hit the highest in more than seven years last month.

“Probably more action is needed to bring yields down further, but authorities may not want to do it in an aggressive manner because of the inflation outlook,” said Suan Teck Kin, Singapore-based economist at United Overseas Bank. “Bond investors should expect only a gradual drop in yields.”

Tuesday’s announcement from the PBOC, when it cut by 5 basis points the rate on a tranche of medium-term funds extended to banks, came after weeks of inaction by monetary authorities to address evidence of a weakening economy. Concerns about consumer-price pressures probably explained the delay, said Wu Zhaoyin, chief strategist at Avic Trust Co. in Shanghai.

Market participants will next be watching how the PBOC handles further batches of medium-term funds that come up for renewal. Tranches are due on Dec. 4 and Dec. 16, when officials could trim rates by another 5 to 10 basis points, according to Goldman Sachs Group Inc.

Wu is among those doubting whether the PBOC will also reduce the seven-day reverse repurchase rate. The central bank had raised that money-market benchmark during the Federal Reserve‘s tightening cycle, but has held off on lowering it even as the U.S. shifted to easing this year.

Ten-year Chinese government bond yields were around 3.25% in Shanghai midday Thursday, down from the October high of 3.31%, though still well up on the September low of 3%.

Also in focus for the market is the likelihood of greater supply, as fiscal authorities take steps to shore up growth while the central bank limits its actions.

| Read More: |

|---|

Some analysts have forecast new issuance of local-government bonds could reach 5.5 trillion yuan ($786 billion) in 2020, marking a year-on-year jump of 28%. Local authorities also have more than 2 trillion yuan ($286 billion) of notes maturing next year, according to data compiled by Bloomberg -- a record and 58% more than this year’s level.

Meantime, the central government’s fiscal targets are up for discussion at the annual Economic Work Conference, typically held in December. This year already saw a widening in the budget deficit to 1.83 trillion yuan from 1.55 trillion the previous year, with the gap filled by additional debt. Fiscal stimulus didn’t arrest a slowdown that may drop below 6% in the final quarter of 2019.

“With consumption still weaker than expected, a trade deal not yet in hand, and the housing market under scrutiny, China has to rely more on fiscal stimulus,” said Wu at Avic Trust.

--With assistance from Jing Zhao.

To contact the reporter on this story: Hong Shen in Singapore at hshen87@bloomberg.net

To contact the editors responsible for this story: Richard Frost at rfrost4@bloomberg.net, Christopher Anstey, Sofia Horta e Costa

©2019 Bloomberg L.P.