Even Recession Can’t Cool New Zealand’s Red-Hot Housing Market

It’s just suffered its biggest economic slump since the Great Depression, but New Zealand’s housing market is booming.

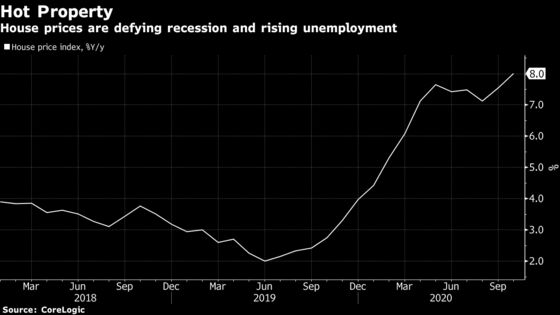

(Bloomberg) -- It’s just suffered its biggest economic slump since the Great Depression, its border is closed and unemployment is rising, but New Zealand’s housing market is booming.

Undeterred by the recession, buyers are rushing to take advantage of the record-low borrowing costs delivered by the central bank as it seeks to reflate the economy. House prices, which had been expected to drop during the pandemic, have instead surged to fresh record highs. The average price rose an annual 8% in October to NZ$753,000 ($519,800), the fastest gain in more than three years, while sales soared 25% from a year earlier in the busiest month since 2016.

“Most regions are now experiencing double-digit house price growth. What recession?” said Jarrod Kerr, chief economist at Kiwibank in Auckland. “We no longer see a correction in house prices either this year or next.”

The housing frenzy has become a hot political issue, with politicians accusing the Reserve Bank of inflating prices through rock-bottom interest rates and making homes too expensive for those on lower incomes. It’s a dynamic that’s emerging in other countries with similar housing markets, even those that, unlike New Zealand, have yet to get the pandemic under control.

Australian home prices rose for the first time in six months in October after it stamped out a Covid-19 outbreak, while U.K. prices hit a record even as it braced for new restrictions. In the U.S., house prices posted the biggest annual jump in seven years in the third quarter.

New Zealand has a housing shortage that’s seen demand outstrip supply for many years. Prices have doubled in some areas over the past decade, cementing the perception that property investment is a safe bet.

But there’s little doubt that record-low mortgage rates are fueling the latest price surge. The major banks are currently offering one-year fixed mortgage rates of about 2.5%, down from more than 4.5% three years ago.

The RBNZ has cut its official cash rate to 0.25% and embarked on quantitative easing to drive down borrowing costs. Last week it unveiled a program of cheap loans to banks designed to reduce interest rates further, and it hasn’t ruled out taking the OCR into negative territory next year.

The opposition National Party has called on the government to “rein in” the RBNZ, prompting Prime Minister Jacinda Ardern to stress the importance of the central bank’s independence.

Governor Adrian Orr has said the barrage of monetary stimulus is aimed at reviving inflation and encouraging employment as the economy reels from the coronavirus shock, and he’s taken umbrage at the suggestion he’s fueling social inequality through ultra-loose monetary policy.

“All I ever read about with monetary policy is house prices, yet that’s not our mandate,” Orr told a news conference on Nov. 11. “Our mandate is consumer-price inflation and employment.”

But the RBNZ does have a role in ensuring financial stability, which could be threatened if the housing boom becomes a bubble that bursts. Unemployment is forecast to continue to rise with the closed border keeping international tourists and students out.

What Bloomberg Economics Says

“Asset price inflation is one of the transmission channels of the extreme monetary stimulus delivered in response to the pandemic. As economies stabilize and labor markets begin to recover, central banks are set to encounter a transition in the balance of financial stability risks from employment to asset prices that will require them to turn toward macro prudential policy tools.”

-- James McIntyre, economist

For the full note, click here

Highly-leveraged investors have stormed back into the market since the RBNZ lifted lending restrictions in May that required them to have a 30% down-payment to qualify for a mortgage. At the time, it wanted to remove any obstacles to the flow of credit. Now it has reneged on a commitment to keep the restrictions off for 12 months and said it will reinstate them in March.

“We have seen a marked acceleration in higher risk loans, particularly to investors in the property market,” Orr said.

The return of macro-prudential measures may take some steam out of the market, but it won’t be a game changer, said Dominick Stephens, chief New Zealand economist at Westpac Banking Corp. in Auckland. He expects house-price inflation to accelerate to 15% by June next year, with prices climbing 13% over 2021 as a whole.

“Rising house prices are an unintended consequence of the Reserve Bank’s interest-rate cuts,” said Stephens. “But that doesn’t mean the RBNZ is going to reverse course -– if it did, deflation and high unemployment would beckon.”

©2020 Bloomberg L.P.