RBA Sees Households Well Placed to Meet Debts as Lending Surges

RBA Sees Households Well Placed to Meet Debts as Lending Surges

(Bloomberg) -- Australians are cashed up from stimulus payments during Covid-19 restrictions that should allow them to meet their commitments, the central bank said, as separate data showed another surge in home loans.

“Almost all households with a mortgage remain well positioned to service their debt, and many have responded to the increased uncertainty and any boost to their cash flow by increasing their prepayments,” the Reserve Bank said in its semi-annual assessment of the financial system in Sydney on Friday. “The strengthening in lending standards over recent years has meant the share of housing loans with riskier characteristics is lower than in the past.”

The review came as the statistics bureau reported a 12.6% jump in the value of new home loans in August, after an 8.8% gain in July, with first-home buyer commitments advancing 17.7% to the highest level since October 2009. It cautioned that lenders were saying Covid-19 had slowed approvals, meaning the data reflect demand in June and early July, or before the southeastern state of Victoria was forced back into lockdown.

Australia’s economy has been buffeted by the shutdown of large tracts of industry to contain Covid-19, and ongoing restrictions that include the closure of some state and international borders. A spike in unemployment stoked fears of forced housing sales, prompting banks to offer mortgage deferrals and the government to deploy major stimulus to tide over firms and households.

The stability review found that at least 10%–15% of small businesses in the hardest-hit industries don’t have enough cash on hand to meet their monthly expenses. About one-quarter of small businesses currently receiving income support would close if the support measures were removed now, before an improvement in trading conditions, it showed.

The RBA urged lenders to be mindful of the fallout as loan deferrals end. “Banks need to deal carefully with the loans of borrowers who will not be able to resume repayments, in a way that balances avoiding further losses to the bank, the interests of the borrower and potential spillover effects from any sales of collateral.”

Cash Stash

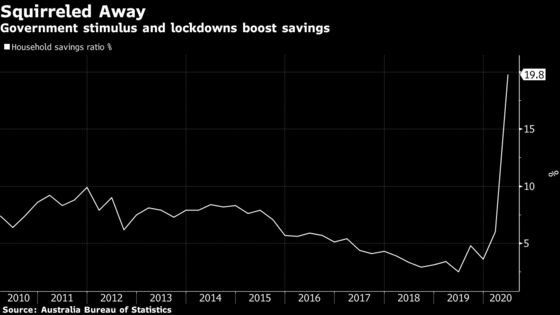

Australians have salted away some of the government cash they’ve been unable to spend on leisure due to the Covid lockdown. They’ve also paid down debt, leaving them well placed to drive a recovery once the virus is contained.

The nation’s savings ratio soared to a 46-year high of 19.8% in the three months through June, and would’ve hit almost 25% if pension-fund withdrawals were included.

“Overall household income in Australia increased in the first half of the year, with large fiscal stimulus payments more than offsetting the decline in employment income,” the RBA said. “Households’ cash flow also benefited from loan repayment deferrals and the early release of funds from superannuation.”

The property market has recorded only mild falls during the Covid-19 crisis, with major city values down just 2.6% since March. Yet there are clouds on the horizon, as mortgage deferrals draw to a close and the job market set to further deteriorate. One market driver will be absent for the next couple of years -- population growth -- as the shuttering of international borders triggers a collapse in immigration.

“To date, job losses and reduced working hours have been most pronounced for younger workers,” the RBA said. “Individuals with mortgages have historically had lower rates of unemployment than renters, although both groups have experienced increasing unemployment over 2020. With further increases in unemployment expected, more households will experience financial stress.”

The RBA cut is cash rate to a record-low 0.25% in March, at the peak of Covid uncertainty, and also set a three-year yield target of 0.25%, in a signal that borrowing costs would remain low for some time. Economists expect the central bank will add further stimulus in the months ahead, potentially taking rates to 0.10% and expanding its bond-buying program.

“While credit is available at very low interest rates, reduced housing demand from very low immigration and the rise in unemployment contribute to the risk of further falls in housing prices,” the RBA said. “This increases the potential for losses for lenders in the event of a rise in distressed sales.”

©2020 Bloomberg L.P.