RBA’s Yield-Curve Control in Cruise Control as Markets Take Hint

Australia’s government bond market is functioning much better than in March when QE began.

(Bloomberg) -- The Reserve Bank of Australia has shifted its yield curve control into cruise control having abstained from buying securities for 47 days now, the same length of time as its initial streak of purchases.

That’s because the government bond market is functioning much better than in March when QE began, leaving the three-year yield anchored around the 0.25% target. The dislocated state of the market was a key factor in the RBA scooping up more than A$50 billion ($34.3 billion) of securities of various maturities in just under seven weeks.

The RBA cut its cash rate to the effective lower bound of 0.25%, announced a bond-buying program targeting the three-year yield and set up a A$90 billion lending facility to get credit flowing into the economy at an emergency meeting in March.

Despite the central bank’s overall success in lowering borrowing costs, the short end of the market is looking a little strange right now as yields on one- and two-years bonds have climbed above the three year due to poor liquidity at these tenors. The RBA said in the minutes of its June policy meeting released last week that it was prepared to act on this.

“Should these developments continue, the bank would consider purchasing bonds in the secondary market to ensure that these short-term yields are consistent with the target for three-year yields,” it said.

Bill Evans, chief economist at Westpac Banking Corp., says the central bank is likely to remain “firmly focused on the short end of the yield curve” in the period ahead because of its relative importance to fixed-rate mortgages and business loans in Australia.

“As borrowers become convinced that the bank will respect the effective lower bound for the cash rate as, for now, is certainly the case, the attraction of fixing borrowing costs will increase,” he said.

Evans expects the RBA to eventually begin a gradually tightening, lifting the three-year target to around 0.4% by mid-2022, with the cash rate remaining at its current level beyond the end of 2023.

Stimulus funding

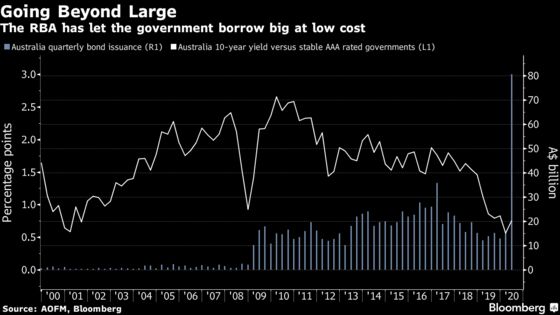

The market’s smooth functioning means the Australian government’s debt arm has had no problem borrowing at an unprecedented pace to finance stimulus.

The Australian government’s debt arm has issued A$80.6 billion of bonds to date this quarter, bringing the total this fiscal year to A$123.2 billion, as it finances the massive fiscal support. That easily bested the previous record in 2017 of A$106 billion.

In discussions with key investors in Australian government debt, the funding arm found that some offshore investors were wary that the sovereign rating could be downgraded, given the volumes of issuance required to fund the fiscal response, but this was unlikely to impact their demand for Australian securities.

“For many investors, the RBA being less active in the government bond market compared to other sovereigns was viewed favourably as this reflected less chance of ‘distortion’ in the AGS market,” it reported.

What this boils down to is that Australia is well placed to access funds, if it chooses to extend or add to its fiscal stimulus programs.

The government will deliver an update to the economic and fiscal outlook on July 23 that is likely to address the future of these programs. The RBA made clear in the minutes that fiscal and monetary support “would be required for some time.”

©2020 Bloomberg L.P.