Spread Shows RBA Rate May No Longer Be Floor for Borrowing Costs

Spread Shows RBA Rate May No Longer Be Floor for Borrowing Costs

(Bloomberg) --

The Federal Reserve’s highly anticipated commercial paper facility is open, but it’s unclear how much more the program will do from here to get much-needed funding flowing to companies.

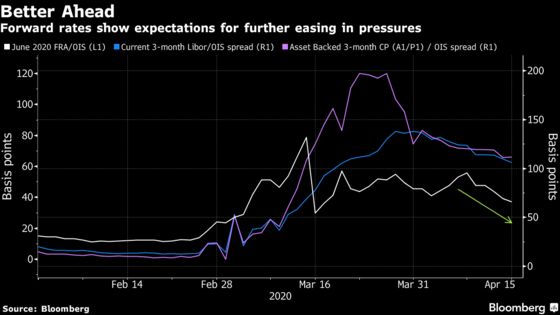

The yield premium over the risk-free rate that investors demand to hold asset-backed commercial paper has steadied. It shrank when the facility was announced a month ago, but the actual start to the program this week has seen it level out roughly in line with the rate offered by the Fed. And the AA rated financial commercial paper market is now in its third straight week without any long-dated issuance, based on Fed data.

These signals contrast with a continued decline in the three-month London interbank offered rate for dollars, a key benchmark for lending between banks. That suggests morale is improving on Wall Street and the market indicates that the unsecured rate should continue to converge with risk-free rates in the coming months, further easing funding pressures.

The Fed’s commercial paper facility is only in its second day of operation, and with no clear read on participation until Thursday’s reserves update from the central bank, it’s too early to tell what the full impact will be. But take-up might not be too overwhelming, as the highly-rated companies that have the best access to the program may have already found alternative sources for their most urgent funding needs in the weeks since it was announced, judging by the record surge in investment-grade corporate bond issuance.

Small businesses may be better served by the central bank’s Main Street Lending Program, said Jefferies money markets economist Tom Simons, who points out that many of the Fed’s facilities are providing help “to the same profile of borrowers.”

“Since small businesses are the majority employers in this country it’s really most important that we make sure that once these communities reopen that the small businesses can reopen too,” he said. “To the extent that the Main Street Facility can help attain that goal -- can help small businesses stay afloat -- it’s more likely that’s going to be helpful.”

The U.S. central bank’s facility allows it to buy three-month corporate, asset-backed and municipal commercial paper. The rate for top-tier assets has so far been set at 1.18%, which was a touch below Tuesday’s market rate and in line with Wednesday’s.

Secured funding rates, meanwhile, are rising in line with the flood of Treasury-bill issuance, with another $60 billion on the slate Wednesday. The general collateral repurchase-agreement rate -- the benchmark for overnight lending backed by Treasuries -- has climbed to around 0.10%, having started the week around 0.08%, based on ICAP data.

The Secured Overnight Financing Rate, which is intended to replace Libor by the end of next year, has edged up to 0.06%, slightly above the effective fed funds rate of 0.05%. SOFR has attracted a fair amount of attention as it’s included as the reference rate for new loans under the upcoming Main Street facility.

Here’s a look at the state of play in some other key funding metrics:

Europe Unclenching

As is the case in the U.S., unsecured interbank credit markets across the Atlantic have begun to loosen up. The rate that banks use to lend to each other in Europe is showing signs of peaking and that’s good news for the region’s funding market.

The three-month Euro interbank offered rate fell to minus 0.25% on Wednesday, its second daily drop and down from a four-year high touched last week. A number of factors behind the rate look calmer, limiting the potential for any further gains.

The European Central Bank “now provides a strong backstop to commercial paper yields and is also able to purchase sub-one year public bonds, the market has reduced its ECB rate-cut expectations, and recent collateral easing measures should reduce reliance of euro-area banks on unsecured funding,” Ronald Man, a rates strategist at Bank of America Merrill Lynch, said in a note.

Euribor interest-rate futures, which reflect the rate at expiry, show expectations are the highest in May, before falling to minus 0.42% in the summer of 2021. The rate isn’t seen rising back to current levels until 2024.

RBA, Swap Rate

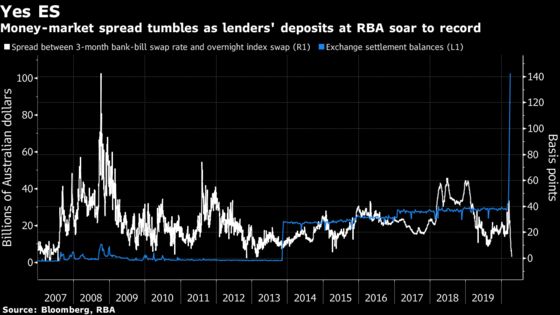

A disappearing spread between money-market rates and expected policy equivalents indicates the Reserve Bank of Australia’s official cash rate may no longer serve as the floor for borrowing costs.

The three-month bank-bill swap rate -- a gauge of Australian borrowing costs -- has continued to slide, with its spread over a similar-tenor overnight index now poised to fall below zero for the first time since 2007. As the RBA pays 0.1% on exchange-settlement balances -- while keeping its official cash-rate and target for three-year bond yields at 0.25% -- lenders’ deposits at the central bank’s ES accounts have soared to a record.

“As the RBA floods the short end with cash, most instruments are being crushed against the 0.10% rate earned on exchange-settlement balances,” Philip Brown and Martin Whetton, strategists at Commonwealth Bank of Australia, wrote in a note. “The cash rate is no longer the important number.”

©2020 Bloomberg L.P.