Rates Experts Work to Decode Enigma of Fed Balance-Sheet Pivot

Gentler-than-expected unwinding of the balance sheet is seen averting liquidity strains.

(Bloomberg) -- As equity investors cheer the Federal Reserve’s newfound caution toward shrinking the balance sheet, rates traders are still working to decode its implications.

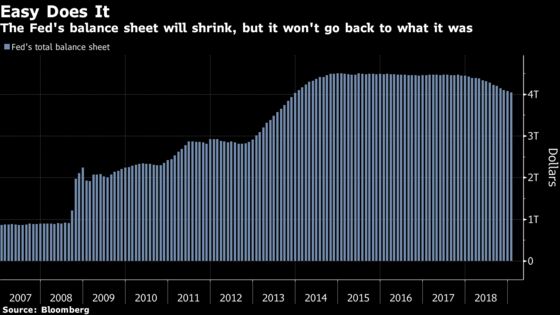

In the fed funds market, a gentler-than-expected unwind of the central bank’s $4 trillion portfolio reduces the likelihood that policy makers will lose control of their key target. But the sudden pivot also forces traders to rethink views on all sorts of markets and metrics, from repurchase agreements and Treasury bills to Libor and the yield curve.

Some of these markets may be affected indirectly. Balance-sheet policy changes may have knock-on effects on U.S. government issuance, or implications for the Fed’s dominant policy lever, the target range for interest rates. And since policy makers have offered no details on the balance sheet’s ultimate size, or when it will get there, investors have few hard numbers to play with. Street projections for the end of the unwind now range from a few months from now to well into 2020.

“I don’t think anyone can predict with a high degree of certainty how quantitative tightening is going to end,” said Stewart Taylor, who helps manage $8.1 billion in fixed-income assets at Eaton Vance in Boston. “It’s all a big ball of confusion.”

Still, one area where market veterans expect to see a material impact is in the repo market. As the balance-sheet unwind slowly drains liquidity from the financial system, some are already suggesting bank reserves are starting to become scarce. That may be forcing firms to tap additional funding and -- combined with a surge in T-bill issuance -- contributing to a rise in money-market rates. An earlier-than-anticipated end to the rundown would likely avert strains in the key funding market, the thinking goes.

Rising repo rates have also forced other short-term rates higher, including commercial paper and Libor. As reserves become more abundant, the upward pressure on CP and the London interbank offered rate relative to the effective fed funds rate should also start to wane.

Investors at the shortest end of the Treasury market may likewise benefit if the central bank decides to maintain a larger-than-expected portfolio. The Fed’s unwind has forced the Treasury Department to make up for the lost funding by selling more debt to the public, predominantly bills. Reduced supply pressures should help ease rates.

Moreover, some analysts actually expect the Fed to become a buyer of bills once again as policy makers look to keep the balance sheet steady while allowing holdings of mortgage-backed securities to fully roll off. That said, the supply outlook for the coming months remains clouded as the debt-ceiling debate heats up, and the Treasury is required to pare its cash balance ahead of the March 1 reinstatement deadline.

Fed Funds Fallout

Less T-bill issuance due to an early end to the rundown should also help alleviate much of the upward pressure on the effective fed funds rate, given supply is another key contributor to the drift higher in money-market rates. As bills and short-term assets have become more attractive alternatives to lending reserves to other banks, reduced interbank funding has pushed the policy rate higher.

In June and again in December, to maintain control of a fed funds rate that had climbed to within just five basis points of their target band’s ceiling, officials took the unprecedented step of reducing how much they pay on excess reserves that deposit banks keep at the Fed relative to the upper bound of the range. A policy of more abundant reserves may make a third tweak less likely.

“All things being equal, an early end to the rolloff reduces the chance that short-term rates would have spiked” over the interest the Fed pays on banks’ excess reserves, said Joseph Abate, a Barclays money-market strategist.

“The concern was that if you pulled out too much liquidity, you would create upward pressure on repo and funding rates,” he said. “Now that the Fed has indicated that it wants to accommodate bank demand for reserves, there’s less of a risk of that happening.”

Curve Ball

Asset managers are also parsing the Fed’s balance-sheet plans -- and what they signal for interest rates -- as potential cues for yield-curve steepening trades.

“An early end to the runoff will be viewed in a very positive light,” as it would point to a central bank on the verge of easing, said Eaton Vance’s Taylor. He sees short-dated Treasury securities benefiting versus longer maturities, causing the yield curve to steepen.

The Fed’s balance-sheet policy may also more directly support the case for a steeper curve. Minutes of the Fed’s December policy meeting showed several members favored maintaining “a portfolio of holdings weighted toward shorter maturities,” which would preserve the Fed’s ability to curb benchmark borrowing costs in the next downturn by buying longer-dated securities.

“If the Fed’s focusing on short-term securities, that would imply at the margin a steeper curve,” said Jabaz Mathai, Citigroup Global Markets’ head of U.S. rates strategy. “That also gives the Fed flexibility if they need sometime to engage in Operation Twist.”

--With assistance from Liz Capo McCormick.

To contact the reporters on this story: Emily Barrett in New York at ebarrett25@bloomberg.net;Vivien Lou Chen in San Francisco at vchen1@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Boris Korby

©2019 Bloomberg L.P.