Quantitative Tightening to End as Central Banks Retreat

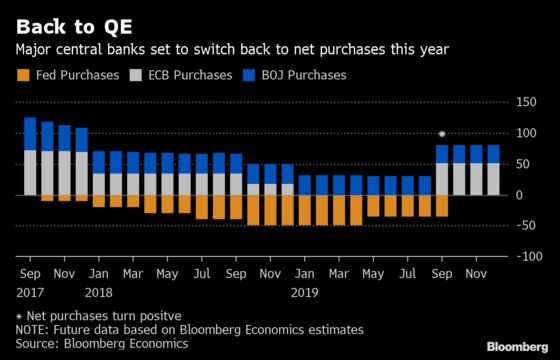

Net purchases by major central banks set to turn positive.

(Bloomberg) -- The era of quantitative tightening by major central banks is proving to be short lived.

Net bond purchases by the Federal Reserve, European Central Bank and Bank of Japan will swing back above zero from September, according to an analysis of their balance sheets by Bloomberg Economics. That’s just eleven months since they collectively hit reverse having spent a decade pumping stimulus into their economies via quantitative easing.

The outlook shows how quickly central banks have been forced to turn tail after spending much of last year leaning toward tightening monetary policy, only to now be looking to loosen it as the world economy slows. It also underscores how their balance sheets are likely to remain permanently larger than the pre-crisis years.

Wall Street and the White House may be delighted by the decision. Many traders blamed the Fed-led withdrawal of stimulus for a sell-off in stocks near the end of 2018. President Donald Trump also attacked the Fed, tweeting as recently as Friday that it “must stop with the crazy quantitative tightening.”

For investors, the switch back, coupled with shifts toward lower interest rates, strengthens the case for buying bonds given the increased demand and shrinking supply of them. That could add fuel to a rally that’s already pushed average yields on global bonds down by almost 1 percentage point since November, left an almost $13 trillion pile of negative-yielding bonds and sparked predictions that U.S. 10-year borrowing costs could also hit zero. Those lower yields would tend to push investors back into stocks.

The conclusion of quantitative tightening in the U.S. will probably come as the Fed is easing borrowing costs for the first time since 2008.

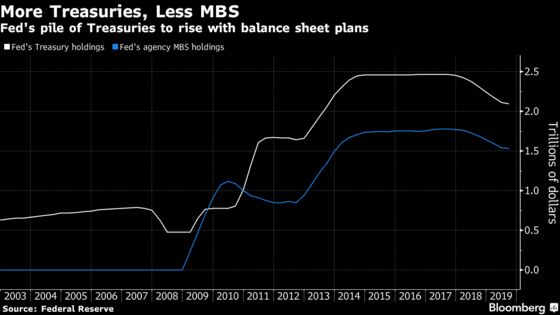

Since the Fed began reversing QE in October 2017, it has shed about $370 billion in Treasuries from its balance sheet which had hit $4.5 trillion in 2015. Those holdings will begin to rise later this year as the Fed ends the unwind and engineers plans to move back to pre-crisis norms of holding only government debt by slowly replacing its $1.5 trillion in mortgage-debt holdings with Treasuries.

According to an estimate by Wells Fargo & Co., the U.S. central bank’s balance sheet will rise past its historic peak as it adds over $2 trillion to its Treasury debt holdings in the next decade. The analysts predict the Fed will opt to focus some of their new purchases on Treasury bills, which will combine with other forces to steepen the yield curve.

“The Fed’s plans for the balance sheet are to shift out of MBS and into Treasuries and, given their guidance, they should be buying some bills,” said Mike Schumacher, strategist at Wells Fargo. “That will cause the curve to steepen.”

As for the European Central Bank, Bloomberg Economics is among those predicting it will announce in September that it will be purchasing bonds again. Its base case is that the ECB will start 45 billion euros of monthly net asset purchases to run for a year, starting in the fourth quarter.

ECB executive board member Benoit Coeure, the head of market operations and a driving force behind QE when it was launched in 2015, said this month that policy makers could hypothetically restart net asset purchases if circumstances demanded. Goldman Sachs Group Inc. and Morgan Stanley are also predicting a return to the pumps.

In contrast to the ECB and Fed, the Bank of Japan ran out of time to officially taper its program of buying stocks and bonds before the policy debate shifted back to the need for more stimulus.

The central bank has some room to expand its purchases of government debt after scaling back its buying to well below half an 80 trillion yen annual target as markets helped to keep bond yields low. A higher national sales tax this October could be the trigger for the BOJ to do more.

Other central banks may also step up. Economists have started to speculate that the Reserve Bank of Australia may eventually begin doing so amid the potential for its benchmark to go below 1%. The Reserve Bank of New Zealand is also reviewing its unconventional monetary policy strategy, Bloomberg News reported on Tuesday.

With Bank of America Corp. estimating central banks worldwide bought more than $12 trillion of assets since the crisis of 2008, there are concerns further rounds will have less impact than in the past.

Deutsche Bank AG chief economist Torsten Slok waded through 16 academic studies and found that most reckoned there is a diminishing impact from QE and the success of such programs in the past in controlling long-rates and inflation expectations was mainly focused on the effect of the announcement.

“Academic papers evaluating QE across countries show that it is no longer a useful instrument,” said Slok.

--With assistance from Enda Curran.

To contact the reporters on this story: David Goodman in London at dgoodman28@bloomberg.net;Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, Simon Kennedy, Alister Bull

©2019 Bloomberg L.P.