Quantitative Tightening Not So Frightening, Even as Stocks Slump

Quantitative Tightening Not So Frightening, Even as Stocks Slump

(Bloomberg) -- U.S. President Donald Trump is not alone in blaming the Federal Reserve for this week’s tumble in stocks, as many investors attribute the ebbing of easy money for spurring an outbreak of market turmoil.

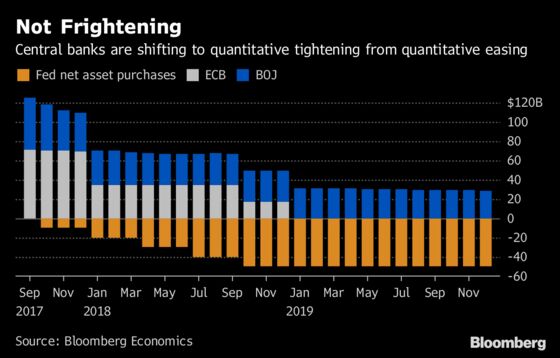

With Bloomberg Economics declaring October as the month the world’s major central banks together start running down their bond holdings, the withdrawal of liquidity is being blamed in part for the summer sell-off in emerging markets, the highest 10-year U.S. Treasury yield in seven years and the biggest drop in stocks since February.

What’s at risk of getting lost in the focus on the shift by central banks to quantitative tightening from quantitative easing, however, is how accommodative they still are -- and are set to be for some time to come.

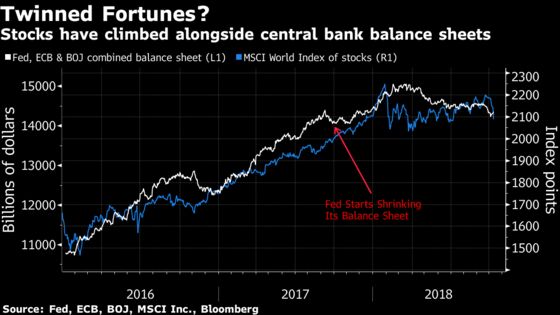

Even as they stop, slow or reverse their buying of bonds, Bank of America Corp. reckons the combined balance sheet of the Fed, European Central Bank, Bank of Japan and Bank of England will be just 4 percent smaller by the end of 2020. That means plenty of liquidity left sloshing around the global financial system and supporting the world economy.

“We are worried about a lot of things -- trade wars and oil sanctions come to mind -- but we are not worried about quantitative tightening,’’ Ethan Harris, chief economist at Bank of America, wrote in a recent report to clients titled “Quantitative Frightening.’’ Harris, who previously worked at the New York Fed, says still-large balance sheets suggest “a limited bond market sell-off and limited spillover into other asset classes.’’

As for interest rates -- which Trump as repeatedly said the Fed has been pushing up too quickly -- the U.S. benchmark remains well below historical averages. The Fed’s policy rate is only barely positive, after adjusting for inflation. And in the euro area and Japan, nominal rates, let alone real ones, remain negative.

Indeed, an average rate for developed-market borrowing costs compiled by JPMorgan Chase & Co. economists only rose above 1 percent last month for the first time since 2009. Even 12 months from now, it’s forecast at about 1.5 percentage points below the average of the two years before the financial crisis.

For now, that may be little comfort for Treasuries investors contemplating a rare annual loss. The 2.5 percent slide in the Bloomberg Barclays U.S. Treasury Index so far in 2018 puts it on course for the first drop since the 2013 taper tantrum, and only the third since 2000.

The slide in Treasuries, which sent the 10-year yield as high as 3.26 percent on Tuesday, added to the unease for stock investors. With money-market funds now yielding real returns, the bar is higher to invest in riskier assets, the thinking goes. The S&P 500 Index tumbled more than 5 percent Wednesday and Thursday, the most since February. High-yield corporate bonds fell, though recent losses only take them back to mid-August levels.

The retreat from riskier assets could get a whole lot worse in the eyes of those warning that the QT campaign could be more aggressive than most assume.

Morgan Stanley strategists warned clients this week of a 1987-style disruption. Back then, the Fed had been hiking rates, then West Germany’s Bundesbank suddenly shifted policy, fueling international economic tensions. And that was the backdrop for the 20 percent slide in the S&P 500 on Black Monday.

Fast forward to this week, and ECB Governing Council member Klaas Knot said policy makers may consider speeding up the process of removing their extraordinary stimulus if the euro-area economy meets their projections.

“Risky asset markets may head toward troubled waters,” Hans Redeker, global head of currency strategy at Morgan Stanley, and his team wrote in a note.

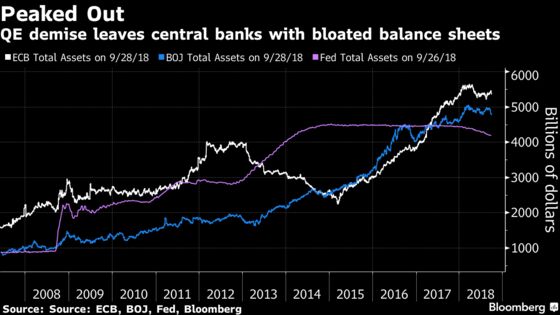

While a heated debate rages on whether QE did much for economies once central banks had staved off a 1930s-scale financial collapse, there’s no argument that the effort has been gargantuan.

The big central banks increased their cumulative balance sheets four times over, with the Fed’s alone topping $4 trillion -- equivalent to 20 percent of U.S. gross domestic product. Japan’s holdings are on course to soon pass the level of GDP.

The Fed started shrinking its bond portfolio a year ago. The ECB is planning to halt its asset purchases at year-end, a step the BOE has already taken, although neither has outlined when it will hit reverse. The BOJ has pared back its buying, but is set to keep pumping out money through next year.

GLOBAL INSIGHT: From QE to QT -- Not Quite Watching Paint Dry

Put it all together and economists anticipate the bond portfolios are set to stay bloated for a long time -- and much bigger than before the crisis. Cornerstone Macro LLP predicts the Fed’s holdings will only shrink about 40 percent as much as they expanded.

Ultimately, the impact of policy normalization could be a rotation within asset classes, rather than a wholesale exit towards cash. That suggests a shift toward financial stocks as interest rates rise, with groups like technology struggling. Other pivots could come in fixed income; JPMorgan has highlighted how bond issuance skewed toward lower-rated companies and longer-dated securities in the QE era.

For many, it’s all part and parcel of any monetary tightening cycle.

“Quantitative tightening is a phrase I hear often,” said Roberto Perli, a partner at Cornerstone and a former Fed official. “But there’s nothing to worry about. It’s not going to be that large.”

To contact the reporters on this story: Simon Kennedy in London at skennedy4@bloomberg.net;Christopher Anstey in Tokyo at canstey@bloomberg.net

To contact the editors responsible for this story: Stephanie Flanders at flanders@bloomberg.net, Brian Swint, Lucy Meakin

©2018 Bloomberg L.P.