Putin's Crisis Firefighter Passes the Baton on Fixing Economy

Russia’s central bank believes that it’s time for government to assume the burden of fixing what ails the economy.

(Bloomberg) -- Russia’s central bank, which fought on the front-lines of the country’s battle to save its currency almost four years ago, believes it’s time for the government to assume the burden of fixing what ails the economy.

With crises flaring across emerging markets from Turkey to Argentina, there’s again no shortage of calls for decisive action by central bankers. When the moment of truth arrived for the Bank of Russia in 2014, Governor Elvira Nabiullina held little back, jacking up the key interest rate in the middle of the night in Moscow and spending about a fifth of its international reserves to prop up the ruble before allowing the currency to trade freely.

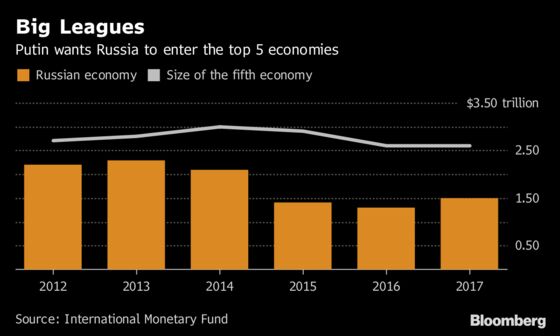

But now that the focus is increasingly shifting to economic growth, the central bank is sticking to the sidelines. Speaking in a Bloomberg Television interview, Nabiullina said it’s up to the government to deliver the structural reforms needed to meet President Vladimir Putin’s goal of turning Russia into one of the world’s five biggest economies.

The “serious external shocks” Russia faced in 2014 “ultimately affected the financial sector and that’s certainly why we were the ones who had to take decisions ahead of others,” Nabiullina said on Thursday at the St. Petersburg International Economic Forum. “But in order to increase the pace of economic growth, financial and macroeconomic stability isn’t enough.”

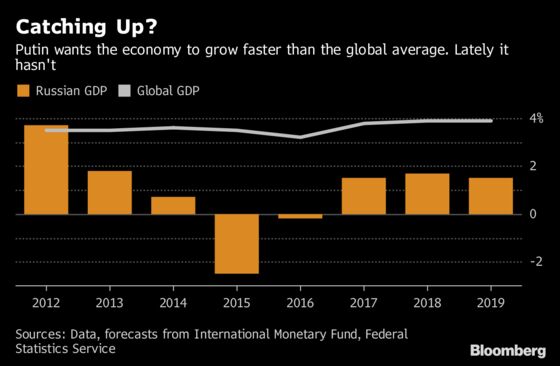

Re-elected in March, Putin has promised to accelerate sluggish economic growth to a level that exceeds the global average and deliver a “decisive breakthrough” in living standards during his current six-year term. But Nabiullina has repeatedly warned that the economy won’t grow faster than 2 percent without structural reforms.

While the global economy gained 3.8 percent last year, Russia’s gross domestic product increased 1.5 percent, far below official estimates. Despite a rebound in oil prices, it expanded 1.3 percent in the first three months from a year earlier, missing projections for the third straight quarter. The latest round of U.S. sanctions dealt a new blow in April.

Stopping short of calling Putin’s goals unrealistic, Nabiullina described them as “rather ambitious” but achievable. Still, “decisive measures” are needed to implement structural reforms that increase productivity and create the conditions for investment.

For Nabiullina, that means creating “predictable conditions -- in taxes, in complying with the rules of the game, and in reducing regulatory barriers for business.” The government is “drafting concrete measures now,” she said.

Under her stewardship, the central bank has done its part. Since preventing a financial meltdown in 2014, it’s pushed inflation to a record low and kept rates elevated. The ruble is the best performer in emerging markets this month against the dollar, recouping losses after its steepest drop since 2015 in April.

The latest round of U.S. sanctions complicates Russia’s prospects by threatening to undermine investment. While the impact of the penalties on the economy is hard to quantify, it will be “rather limited,” according to Nabiullina. The sensitivity of the exchange rate to oil prices has declined, and inflation is less vulnerable to ruble fluctuations, she said.

Although conservative policies and low inflation may not jumpstart the economy, the governor said they provided enough protection for Russia to weather the recent turmoil.

“Markets have stabilized rather fast,” Nabiullina said.

--With assistance from Andrey Biryukov, Anna Andrianova and Evgenia Pismennaya.

To contact the reporters on this story: John Micklethwait in St. Petersburg at micklethwait@bloomberg.net;Olga Tanas in Moscow at otanas@bloomberg.net

To contact the editors responsible for this story: Gregory L. White at gwhite64@bloomberg.net, Paul Abelsky, Tony Halpin

©2018 Bloomberg L.P.