Powell to Duck Taking Sides as Two Fed Camps Square Off on Rates

Powell to Duck Taking Sides as Two Fed Camps Square Off on Rates

(Bloomberg) -- Federal Reserve Chairman Jerome Powell will probably gloss over an emerging division among policy makers about what it will take for them to resume raising interest rates when he speaks to lawmakers on Tuesday.

On the one side is what economist Stephen Stanley calls the Mester camp -- after Federal Reserve Bank of Cleveland President Loretta Mester. This group sees the Fed restarting rate hikes if the economy performs as they expect -– with slower but still solid growth, low unemployment and inflation near 2 percent.

The Williams camp -- named after New York Fed President John Williams -- would require inflation beating their forecasts before recommencing rate increases, according to Stanley. Fed Vice Chairman Richard Clarida also seems to belong in this group of Federal Open Market Committee policy makers.

“The opinion on the committee is pretty divided,’’ said Stanley, who is chief economist of Amherst Pierpont Securities LLC. Powell will try “to nuance any disagreement on the committee and focus on what they have common ground on.’’

Powell begins his semi-annual testimony to Congress at 9:45 a.m. on Tuesday before the Senate Banking Committee and continues on Wednesday before the House Financial Services Committee.

Which group of policy makers prevails in the rate debate is of critical importance to financial markets and to President Donald Trump.

If the Mester camp wins out, then the Fed could resume raising rates later this year as uncertainties surrounding the outlook dissipate.

If the Williams-Clarida group carries the day, the central bank may be on hold for the rest of 2019, pending a sustained inflation reading at or above the Fed’s 2 percent target.

That would be welcome news for Trump, who sharply criticized the Fed last year for raising rates and who met Powell to discuss the economic outlook on Feb. 4.

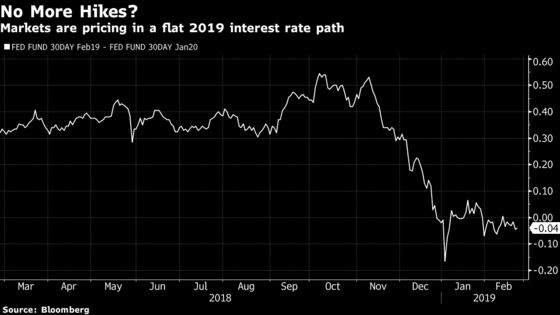

Investors expect the Fed to refrain from any hikes this year and lean toward the next move being a cut, according to trading in the federal funds futures market.

Policy makers surprised the markets last month by dropping their projection of “some further gradual increases’’ in interest rates and replacing it with a promise to be “patient’’ in determining future adjustments in policy. The FOMC said it took that decision “in light of global economic and financial developments and muted inflation pressures.’’

Since then, world financial markets have advanced, driven in part by growing optimism of a lasting truce in the U.S.-China trade war. The outlook for global growth and for U.S. inflation though remains uncertain.

Powell sounded like he was in the Williams-Clarida camp when he spoke to reporters on Jan. 30.

“I would want to see a need for further rate increases and, for me, a big part of that would be inflation,’’ he said.

Measured by the Fed’s preferred gauge, and excluding volatile food and energy components, inflation in the U.S. measured 1.9 percent in the 12 months through November. It topped 2 percent, on an unrounded year-over-year basis, just once since 2012.

Williams voiced concern last week that inflation expectations may have slipped downward after years in which price rises have failed to reach 2 percent.

“We have seen some worrying signs of a deterioration of measures of longer-run inflation expectations in recent years,” he said. “The risk of the inflation expectations anchor slipping toward shore calls for a reassessment of the dominant inflation targeting framework.”

Williams and San Francisco Fed researcher Thomas Mertens argued in a January paper that allowing inflation to overshoot 2 percent when policy interest rates are above zero would help to keep inflation expectations anchored. Currently, the Fed has a symmetric target set at 2 percent that disregards past inflation rates.

While the Fed has just begun in-depth discussions on whether to change that inflation framework, Williams’ views “have already had an impact’’ on its current approach to policy, said Deutsche Bank Securities chief economist Peter Hooper.

“We got a fairly noticeable shift’’ in the FOMC’s stance in January, with policy makers evincing more concern about inflation being too low, he said.

Still, not all policy makers are convinced that price rises need to surprise on the upside for rate hikes to restart.

“For some FOMC members, seeing a decline in uncertainty -- especially with respect to trade frictions and global growth -- might be enough to justify further tightening,’’ Wrightson ICAP LLC chief economist Lou Crandall said.

Mester said last week that interest rates ‘‘may need to move a bit higher’’ if the economy performs along the lines she’s expecting. She’s forecasting growth of 2 percent to 2.5 percent this year, unemployment at or below 4 percent and inflation near the Fed’s 2 percent goal.

It’s “not particularly clear’’ what it will take for the Fed to resume raising rates, said Roberto Perli, a partner at Cornerstone Macro LLC, adding, “the market is very much focused on this.’’

To contact the reporters on this story: Rich Miller in Washington at rmiller28@bloomberg.net;Steve Matthews in Atlanta at smatthews@bloomberg.net

To contact the editors responsible for this story: Alister Bull at abull7@bloomberg.net, Brendan Murray

©2019 Bloomberg L.P.