Powell Bolsters Case for Fed Rate Pause as Inflation Stays Muted

Details on balance sheet plan coming reasonably soon, Powell says.

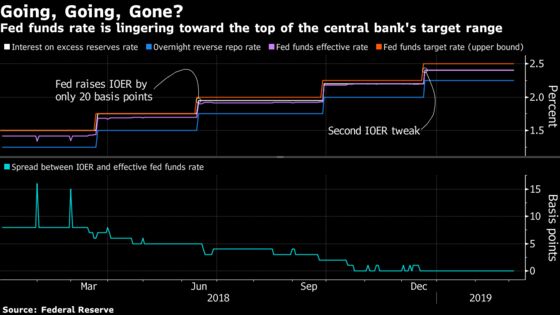

.jpg?auto=format%2Ccompress&w=200)

(Bloomberg) -- Federal Reserve Chairman Jerome Powell made clear he and his colleagues are in no hurry to adjust interest rates as growth slows and inflation stays muted, but said the U.S. central bank would announce new details of plans for its balance sheet “reasonably soon.”

In a speech late Friday in Stanford, California, Powell didn’t mention the dismal U.S. employment report for February released earlier in the day, saying measures of the labor market “look as favorable as they have in many decades,” before reiterating the Fed’s mantra on being patient.

“Despite this favorable picture, we have seen some cross-currents in recent months,” he said in the prepared remarks. “With nothing in the outlook demanding an immediate policy response and particularly given muted inflation pressures, the committee has adopted a patient, wait-and-see approach to considering any alteration in the stance of policy.’’

He also said the rate-setting Federal Open Market Committee is “well along in our discussions of a plan to conclude balance-sheet runoff later this year.”

Growth Slowdown

Powell’s remarks follow a spate of gloomy economic developments in the U.S. and elsewhere that are validating the Fed’s decision earlier this year to put interest-rate moves on hold for the time being after hiking four times in 2018. A possible warning sign in that data-dependent strategy appeared as the week came to a close.

The U.S. Labor Department reported that employers added just 20,000 new jobs last month, the fewest since September 2017 and well below economists’ estimates. The outlook outside the U.S. also took a hit this week as China lowered its goal for growth in 2019 to a range of 6 percent to 6.5 percent, while the European Central Bank slashed its forecast for 2019 growth to 1.1 percent from 1.7 percent.

U.S. stocks fell more than 2 percent on the week.

Responding to questions after his speech, Powell said inflation in the U.S. is low, stable and doesn’t react much to slack in the economy -- the product of economic changes and credibility in the Fed built up over the decades that needs to be maintained.

He also said economies around the world have slowed in the past six months, citing Western Europe, China and the U.S. Downside risks to the outlook have increased, he said, citing Brexit and uncertainty around trade policy.

Reacting to Data

Mark Duggan, director of the Stanford Institute for Economic Policy Research, said following the speech that he thought Powell and his colleagues were striking the right tone around monetary policy.

“They’re reacting to the data and that’s smart,” he said. “The data has come in recently suggesting inflationary pressures are going down not up.”

Powell’s speech marked the last substantive public remarks from a Fed official before the FOMC convenes March 19-20 to decide the next move on monetary policy after offering new economic forecasts and rate projections. No rate move is expected amid concerns such as those raised Thursday by Fed Governor Lael Brainard, who said a weakening economic outlook in the U.S. and abroad argue for a “softer” path for interest rates than previously envisioned.

Powell devoted part of his prepared remarks to the importance of maintaining trust in public institutions. The U.S. central bank has come under scrutiny from President Donald Trump, who has complained about Powell’s campaign to return rates to a more normal setting. Powell will have an opportunity to lay out the Fed’s strategy in an interview scheduled to air Sunday night on CBS’s “60 Minutes” program.

Speaking at length on a variety of topics, Powell said the decision on the level at which to halt balance-sheet runoffs will be determined by estimates of the demand for bank reserves. Reserves are on the liability side of the balance sheet and have fallen largely in line with the ongoing decline in assets.

When the monthly runoffs are halted, Powell said officials may decide to hold the overall size of the balance sheet constant “for a time to allow reserves to very gradually decline to the desired level as other liabilities, such as currency, increase.”

The Fed expanded its balance sheet to a high of $4.5 trillion with bond purchases, including during the Great Recession. Since October 2017, officials have trimmed the portfolio back to about $4 trillion.

The Fed manages short-term interest rates through a mechanism it adopted during the financial crisis that relies on abundant bank reserves and so is keen not to let reserves fall too low.

In another nod to post-crisis “normalization,” Powell said he has asked a group of his colleagues to review the role of interest-rate projections that are published quarterly, or the Fed’s so-called “dot plot.”

The tool has gathered even more attention from economists and investors as the central bank has reduced the amount of forward-looking guidance it provides to the public through its policy statements in recent years. But it does a poor job, Powell said, of conveying the level of risks attached to those projections.

Forward Guidance

“Returning to a world of little or no explicit forward guidance in the FOMC’s post-meeting statement presents a challenge, for the dot plot has, on occasion, been a source of confusion,” he said. “We will need to find other ways to address the collateral confusion that sometimes surrounds the dots.”

Powell also laid out the objectives of a policy framework review the Fed has said will last all year, as well as what will not be undertaken.

“We seek no changes in law and we are not considering fundamental changes in the structure of the Fed, or in the 2 percent inflation objective,” he said, adding there is a “high bar” for adopting any other fundamental change.

Powell focused at length on the worries associated with operating monetary policy in a long-term environment of low inflation and low interest rates, making it difficult for the Fed to combat recessions because rates may frequently return close to zero. That’s causing officials to consider adopting a “make-up” strategy wherein they would seek to follow periods of below-target inflation with periods of above-target inflation in an effort to boost the average level of price changes.

Since the Fed adopted an explicit 2 percent inflation target in 2012, the core rate of inflation measured by the central bank’s own favorite gauge has averaged just 1.6 percent.

“Makeup strategies are probably the most prominent idea and deserve serious attention,” he said. “They are largely untried, however, and we have reason to question how they would perform in practice."

To contact the reporter on this story: Christopher Condon in Washington at ccondon4@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Shamim Adam

©2019 Bloomberg L.P.