Powell’s Hawkish Tune Rouses Equities as Bonds Wait It Out

Investors responded to the Fed’s intent to tackle inflation with a clear risk-on pivot, as stocks climbed and Treasuries steadied.

(Bloomberg) -- Investors responded to the Federal Reserve’s intent to tackle inflation with a clear risk-on pivot, as stocks climbed and Treasuries steadied.

Equity strategists highlighted the usually positive outlook for stocks in the early stages of a tightening cycle, even as bond and currency analysts suggested more volatility was likely in their markets into 2022. Though the dollar fell Wednesday, market watchers expect that weakness to be short-lived and see its rally resuming.

“Equity prices turned from red to green, likely because the uncertainty had been lifted and Fed Chair Powell didn’t sound as hawkish as many had feared,” said Sam Stovall, chief investment strategist at CFRA Research. “History says, but does not guarantee, that prior Fed tightenings resulted in minor price increases for the equity market over the ensuing year.”

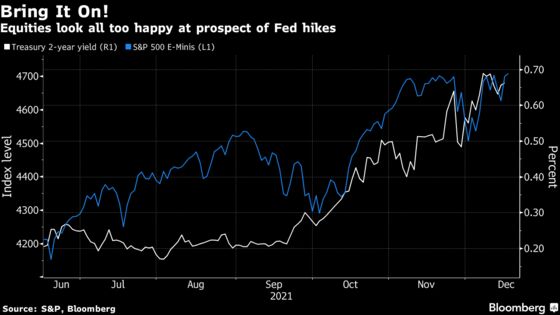

Stovall noted that the S&P 500 Index rose initially during a majority of the Fed’s 17 post-World War II tightening cycles, highlighting a median gain of about 3.5% for the periods between the first hike and the third. Traders are pricing for the first U.S. rate increase to come next June, while the Fed indicated there could be three hikes in 2022.

Abrupt Pivot

In an abrupt policy pivot, the Fed sped up the drawdown of its asset-purchase program and laid out a road map for eight interest-rate increases through to 2024. Chair Jerome Powell also raised the possibility that the central bank might begin to withdraw liquidity before too long by reducing its massive balance sheet.

While equity investors welcomed the combination of Fed certainty and a confident outlook, there were also signs of caution as strategists outlined the risks that either policy aggression or the impact of omicron could undercut the expansion.

“The Fed is likely going to continue to tread lightly as they walk the fine line of attempting to cool inflation without slowing the economy too dramatically,” said Charlie Ripley, senior investment strategist for Allianz Investment Management. “The reality is uncertainty surrounding Fed policy is high and will likely remain that way as Chairman Powell attempts to unwind the largest monetary stimulus package in history without disruption.”

Read: The Fed Is Embracing the Market’s Favorite Strategy: Macro Man

Japanese Stocks

Nomura Securities in Tokyo saw the outcome as broadly positive for global stocks, with extra potential that it could set up Japanese equities for some outperformance -- and not only because the yen weakened noticeably after the meeting.

“Buying in U.S. equities was concentrated in names or sectors where high growth can be anticipated even under a rate-hike cycle,” said Takashi Ito, an equity market strategist at Nomura. “It wouldn’t be strange to see the discount on Japanese equities narrow following the FOMC, with market interest centered around electronics, machinery, automakers and marine transportation stocks.”

King Dollar

Currency strategists expect dollar strength to reassert itself, despite the overnight surge for commodity currencies such as the Australian and New Zealand dollars. National Australia Bank Ltd. sees the Fed potentially hiking four times next year, provided the pandemic doesn’t substantially disrupt the economy.

“There was clearly not enough drama to warrant a material extension of the dollar rally,” HSBC Holdings Plc strategists including Daragh Maher wrote in a note. “We continue to look for gradual dollar strength ahead through 2022, supported by the Fed’s ongoing move to the exit from accommodative monetary policy.”

Vishnu Varathan, Mizuho Bank Ltd.’s head of economics and strategy, also sees a firmer dollar in the first half, especially against the euro and the yen. Even commodity currencies look vulnerable because of the potential for weaker raw materials prices, he said.

Rising Yields

The lack of a strong reaction in bond yields was also seen as only temporary, with most strategists expecting a fresh climb that would start with shorter-dated maturities and extend.

“U.S. 10-year yields could test 2% in 2022,” Mizuho’s Varathan said. “Whether that will be exceeded could at a later stage be a function of the expiry of flexible average inflation targeting. Or in other words a reversion to an outright inflation target.”

While the U.S. yield curve initially flattened, the bets unwound by the end of the trading day, with longer-end yields rebounding.

JPMorgan Asset Management warned of the impact higher yields might have on the higher-priced sections of the stock market.

“Higher yields can add to the pressure on high valuation pockets of the equity markets, suggesting a broader position across global equities, including emerging markets and particularly Asian equities given the scope for earnings upgrades,” said global market strategist Kerry Craig.

Emerging Pressure

As for the impact on emerging market assets -- which often come under pressure as Treasury yields push higher -- Asia is seen as best prepared to weather the hawkish shift.

“Strong trade surpluses in the region, domestic demand recovering following recent easing in restrictions, and large FX reserve buffers should help to minimize volatility,” said Khoon Goh, head of Asia research at Australia & New Zealand Banking Group Ltd. “Several Asian central banks should also be in a position to begin normalizing policy alongside the Fed, which will help.”

Other strategists pointed to the increased influence of China’s yuan in the emerging-market currency space as a counterbalance to the dollar.

“For EM currencies, they will continue to take cues from the yuan complex, which has seen a rather mild reaction to overnight USD moves,” said Terence Wu, FX strategist in Singapore at Oversea-Chinese Banking Corp. “Near-term reaction should remain rather muted.”

©2021 Bloomberg L.P.