Powell’s Monetary Policy Gets Muddled by Jittery Markets, White House

Fed chair faces criticism from Wall Street to White House.

(Bloomberg) -- There’s what you think you said. There’s what you actually said. And perhaps most importantly for the steward of the world’s largest economy, there’s what people heard.

That’s a lesson Federal Reserve Chairman Jerome Powell is learning the hard way as he seeks to steer the economy between the twin shoals of overheating and recession while being buffeted by criticism from Wall Street to the White House.

Powell is going to be getting a lot more practice. He’ll hold a press conference after every Fed meeting from next month onward -- boosting both the opportunity to refine his message and the risk of sowing confusion.

Case in point: Powell’s unscripted comments on Oct. 3 that monetary policy was still boosting the economy and probably was “a long way from neutral” but might eventually have to turn restrictive.

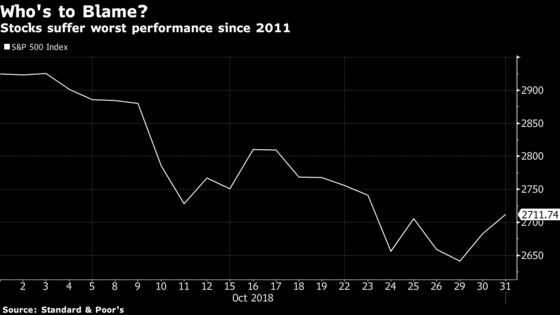

While numerous Fed watchers saw the remarks as nothing new, many investors heard it as a signal that the central bank was far from finished raising interest rates. And they dumped stocks in response, helping send the S&P 500 Index to its worst performance since 2011 last month.

Jefferies LLC chief market strategist David Zervos didn’t mince words, blaming Powell’s inexperience at the helm. The sell-off was “simply the result of a novice Fed chair fumbling the communications ball,” he said in an email to clients, dismissing arguments that U.S.-China trade tensions or other factors were to blame.

Powell and his colleagues are expected to hold policy steady at a two-day meeting starting Wednesday, while leaving the door ajar to a rate increase at their final gathering of 2018. Powell’s next press conference is scheduled for Dec. 19 and he will then hold one after every gathering starting in January.

December ‘Resolve’

“Heightened financial market volatility has not altered the Fed’s resolve to hike in December,” Morgan Stanley Chief U.S. Economist Ellen Zentner and her fellow economists wrote in a Nov. 1 note.

The problem is that investors are still getting to know Powell eight months after he became chairman. Unlike predecessors Ben Bernanke and Janet Yellen, he doesn’t have a Ph.D. in economics and prides himself on his ability to translate difficult subjects into plain English. That’s undoubtedly what he was trying to do in his Oct. 3 comments to television anchor Judy Woodruff.

The result is that perhaps “a little gets lost in translation in the financial markets because people want to infer changes in the substance of what’s being said when what’s changing is just the approach or the tone,” said Stephen Stanley, chief economist of Amherst Pierpont Securities LLC.

It hasn’t helped that Powell has spent his early days being critical of some concepts that have served as Fed policy lodestars in the past. He’s stressed the wide bands of uncertainty surrounding economists’ estimates of R star -- the neutral interest rate that neither spurs nor curbs growth -- and U star -- the unemployment rate that is sustainable in the long-run.

Not Clear

So when Powell said that interest rates were far from neutral, it’s perhaps not surprising that investors didn’t know exactly what was meant.

“They do seem very proud of their transparency but if that transparency is just them saying we’re not sure of anything, then it’s unclear what they are so proud of,” Michael Feroli, chief U.S. economist for JPMorgan Chase & Co., said in an email.

What Our Economists Say:“The market sell-off in October was much more tied to evidence of tariffs impacting companies’ quarterly earnings than it was to Fed rhetoric. Had it been the latter, market expectations for the Fed would have materially changed, and this is not the case. Powell was right to throw cold water onto the mounting mania toward the star-variables. They are useful academic instruments -- however, the lack of precision in knowing these in real time is a substantial hindrance to their utility -- one which should not be overlooked.”-- Carl Riccadonna, chief U.S. economist, Bloomberg Economics |

Powell and his colleagues also “have not been terribly up front about the need to eventually get the labor market in equilibrium,” said Deutsche Bank Securities Chief Economist Peter Hooper. That too is not surprising: Any suggestion that the Fed was trying to engineer a rise in joblessness could trigger even more criticism from President Donald Trump.

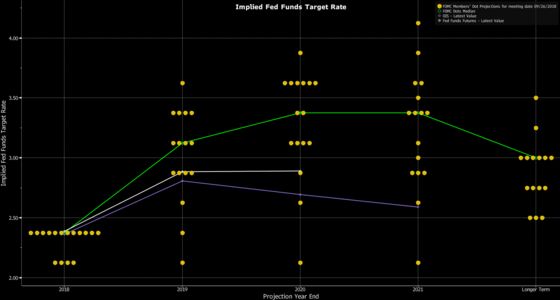

The result is that even seasoned Fed watchers are puzzling over where Powell falls in the so-called dot plot of policy makers’ interest rate projections. That’s in contrast with Yellen: Economists were pretty certain which anonymous dot she represented in the quarterly forecasts.

“We don’t know where Powell is,” said HSBC Securities Chief U.S. economist Kevin Logan, adding, “He’s probably somewhere in the middle” of the dot plot but whether he favors two, three or four rate increases next year is unclear.

Logan said the Fed is approaching an “inflection point” for monetary policy and its communications strategy. For years, its task was clear: nurture a slow-motion recovery by running an expansionary policy. But now, with unemployment at a 48-year low and inflation on target, the Fed is getting out of the business of providing the economy with support. What comes afterward is less clear.

The improving economy is also allowing the Fed to step back from holding the market’s hand by scaling back the forward guidance it provides investors on where rates are headed. It moved in that direction in June when it stopped describing policy as “accommodative” in its post-meeting statement.

Still, there’s only so far the Fed can go in that direction as long as it’s publishing a policy dot plot.

“They are trying to dial back from forward guidance but it’s difficult to go as far as you might like to when you’re still doing these dot plots,” said Johns Hopkins University professor Jonathan Wright.

Wrightson ICAP LLC chief economist Lou Crandall said he understands how investors could have misread Powell’s Oct. 3 remarks and that the chairman himself probably wishes he hadn’t made them.

Still, Crandall voiced hopes that Powell “succeeds in getting to a world where he can speak in plain and not precisely tailored English and not have people misunderstand him.”

To contact the reporter on this story: Rich Miller in Washington at rmiller28@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull

©2018 Bloomberg L.P.