Powell Bets Your Inflation Beliefs Will Help Him Keep the Economy From Overheating

Economists tend to reflect what the Fed tells them while consumers may not fully understand what they’re being asked.

(Bloomberg) -- Federal Reserve Chairman Jerome Powell is pinning his hopes of stopping the U.S. economy from overheating on a variable that a former colleague called “the most significant unobservable of all:” inflation expectations.

In recent public appearances, Powell has argued that the Fed can countenance a fall in joblessness to an almost 50-year low without triggering an inflationary surge in large part because Americans believe the central bank will keep prices under wraps. “The key is the anchored expectations,” he said last week.

The problem is that it’s not easy to divine what inflation beliefs are and how they might change. What’s more, there’s no measure of where companies -- arguably the most important players in setting prices -- expect the cost of living to go. That makes Powell’s focus on price expectations a potentially risky move as the Fed gradually raises interest rates.

“The concept of inflation expectations is quite under-theorized and hard to pin down empirically,” Powell’s former Fed colleague, Daniel Tarullo, said in a speech last October.

Janet Yellen, Powell’s predecessor as Fed chair, also understood the limitations: “Economists’ understanding of exactly how and why inflation expectations change over time is limited,” she said in a speech in September 2017.

If inflation were to get out of control, that would be bad news for investors. In recent days, the stock market has been rocked by a rise in Treasury bond yields primarily driven by the economy’s strength -- not by expectations of faster inflation. Yields could march higher still if rising wages and surging oil prices trigger a spike in consumer prices, forcing the Powell Fed to rethink its gradual strategy for containing inflation.

“There’s going to be a little tighter jobs market and a little faster inflation” than the Fed expects, Michael Feroli, chief U.S. economist for JPMorgan Chase & Co. in New York, said in an interview. “The risk is they’ll have go a bit further” in raising rates as a result, he said.

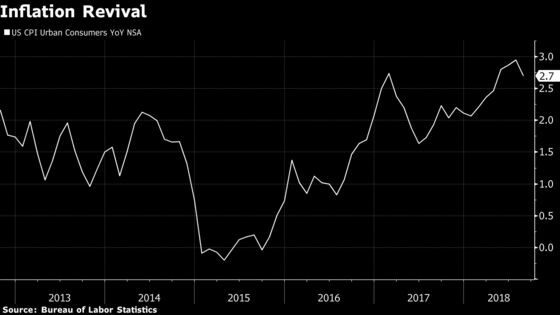

Government data on Thursday are expected to show that consumer price inflation eased to 2.4 percent last month from 2.7 percent in August, according to the median forecast of economists surveyed by Bloomberg. The inflation measure the Fed targets -- the personal consumption expenditures price index -- historically runs about quarter percentage below that gauge.

Tame Prices

The lack of price pressure has spurred a debate about the Phillips curve, an economic model which posits that inflation heats up as the labor market tightens, prompting companies to first boost wages and then prices more broadly as they seek to recoup their additional costs.

That relationship, though, has mostly broken down in recent years as inflation stayed tame despite the drop in unemployment. Powell even quipped last week that “it’s really more like a Phillips line” though he cautioned against throwing out the concept entirely.

Inside and outside the Fed, economists have sought to explain the seeming disconnect between consumer price changes and the job market by stressing the importance of inflation expectations. Companies will resist granting workers bigger salary increases if they believe they can’t raise prices as well. Employees, in turn, may be satisfied with smaller wage gains if they don’t think the pay rises will be eaten up by faster inflation.

“To the extent the public believes that central banks will keep inflation around 2 percent, which is one of our main jobs, that has tended to reduce the sensitivity of inflation to changes in unemployment,” Powell said on Oct. 3.

Goldilocks Economy

He maintains that will help the U.S. enjoy something it hasn’t experienced since 1950 -- an extended period of low, stable inflation and very low unemployment. “This forecast is not too good to be true,” he said on Oct. 2.

Academic economists who’ve studied the Phillips curve are not as sanguine.

“We’ve got this unbelievable momentum” in the labor market that could drive joblessness well below its current 3.7 percent, Harvard University professor James Stock told reporters on Sept. 30. “We’re likely to see inflation rates of 2.5, and then everyone is going to get way stressed out about how we’re going to handle that.”

Northwestern University’s Robert Gordon and Johns Hopkins University’s Laurence Ball agreed that price gains are likely to accelerate. “If unemployment stays at 3.7 or 3.5 percent, it is likely inflation will rise significantly above 2 percent,” Ball said, though he added the Fed shouldn’t overreact to that.

Powell has said the Fed stands “ready to act with authority” if inflation expectations “drift materially up or down.” The catch: He may not know that’s happened until it’s too late.

To assess expectations, the central bank depends on surveys of economists and households and on trading in the bond market, especially demand for Treasury Inflation-Protected Securities. Each has weaknesses.

Economists tend to reflect what the Fed tells them while consumers may not fully understand what they’re being asked. And bond dealings can be distorted by liquidity and other considerations.

Meanwhile, there are signs that businesses have gained pricing power as economic growth has accelerated, especially if they can justify their price increases by pointing to higher tariffs on U.S. imports. A survey of manufacturing and non-manufacturing companies by IHS Markit found that their average selling prices rose at the fastest rate of the nine-year-old expansion in September.

Among companies that have recently announced or warned of impending price increases are PepsiCo Inc., Samsonite International SA and Steven Madden Ltd.

It is paradoxical that Powell is making policy contingent on a squishy concept like inflation expectations. He has, after all, repeatedly cautioned against leaning too heavily on such “unobservable” variables as the natural rate of unemployment or the neutral interest rate.

“Over my time at the Fed, I came to worry that inflation expectations are bearing an awful lot of weight in monetary policy these days,” said Tarullo, who left the central bank last year to become a Harvard Law School professor.

--With assistance from Jeanna Smialek.

To contact the reporter on this story: Rich Miller in Washington at rmiller28@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull

©2018 Bloomberg L.P.