Powell Paves Way for Possible Dovish Shift in Inflation Strategy

Powell said the Fed is happy with the stance of monetary policy after cutting interest rates three times last year.

(Bloomberg) --

Federal Reserve Chairman Jerome Powell signaled that the central bank would pull out the stops to combat a global disinflationary downdraft, foreshadowing a potential shift toward an easier monetary policy over time.

Speaking to reporters on Wednesday after the Fed left its benchmark interest rate unchanged, Powell said he is intent on evading the downward spiral in inflation and inflation expectations that’s bedeviled other countries.

“We have seen this dynamic play out in other economies around the world, and we are determined to avoid it here in the U.S.,” he said.

The strong words -- combined with a minor, yet telling tweak in the Fed’s post-meeting statement -- suggested that the central bank is moving toward a major change in how it interprets its price-stability mandate as it completes a review of its policy framework by mid-year.

“They really want to communicate that they want inflation to move above 2% because they want to see inflation expectations pick up,” said Robin Anderson, senior economist at Principal Global Investors. “It does seem a more dovish emphasis to market participants that the bar for any rate hike is extremely high.”

Under the new approach -- which Powell emphasized is still under consideration -- the central bank would try to make up for past deviations from its 2% target, rather than treating misses of the goal as bygones, as it does now.

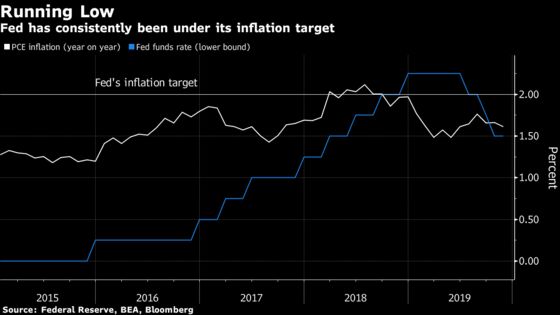

With inflation having run more or less consistently below that goal since it was introduced in 2012, such a shift would likely result in a more dovish Fed as policy makers sought to pump up prices and the economy.

“We’re not satisfied with inflation running below 2%, particularly at a time such as now where we’re a long way into an expansion,” Powell said.

The Fed’s preferred gauge of price pressures -- the personal consumption expenditures price index -- rose 1.5% for the 12 months ending in November. Powell said inflation is expected to move closer to 2% over the next few months thanks to so-called base effects, “as unusually low readings from early 2019 drop out of the calculation.”

On Hold

Powell said the Fed is happy with the stance of monetary policy after cutting interest rates three times last year.

And the central bank is likely to remain that way unless the economic outlook changes materially – no matter what President Donald Trump -- who just this week again called for lower rates -- may want, the Fed chair made clear.

Trade uncertainty has eased, though it’s not disappeared, and global growth looks to be bottoming out, with the economic fallout from a spreading coronavirus still a wild card, he said.

In what some analysts saw as a significant shift, the Fed did alter its post-meeting policy statement to emphasize its determination to hit its 2% inflation target, saying price rises need to return to that level not just be near it.

“I definitely think it tilted dovish and it reinforced a commitment to reflation,” said Laura Rosner, partner at MacroPolicy Perspectives LLC in New York. “It’s a step toward them actually changing their framework” for targeting inflation.

Technical Tweaks

Powell opened his press conference with an explanation of the Fed’s approach to managing money markets, including what he called a small technical rise in the rate the central bank pays on reserves.

Read more: Fed Wrestles to Keep a Grip on Its Key Rate With a Tweak to IOER

The Fed is currently expanding its balance sheet to ensure ample liquidity in the money markets and avoid the sort of turmoil that briefly occurred last September.

Powell said the Fed could end its efforts to beef up its asset holdings in the second quarter by scaling back its monthly purchases from the current rate of $60 billion per month.

He again took issue with those in the markets who argue that the buying has boosted stock prices by flooding the financial system with liquidity, saying that was not the Fed’s intent.

The Standard & Poor’s 500 index has risen about 10% since the Fed announced its bill-buying program last October.

Not Extreme

In response to a question, Powell did allow that asset valuations are somewhat elevated.

“Valuations are high, but not at extremes,” he said, adding though that the overall risks to financial stability are moderate.

What Bloomberg’s Economists Say

The implicit message is that, while policy makers are alert to international developments (i.e. coronavirus, geopolitics, etc.), the accommodative setting of policy -- 75 bps to 100 bps below the committee’s median estimate of neutral -- should give the economy enough support to endure modest changes to the risk landscape.

-- Carl Riccadonna, Yelena Shulyatyeva and Andrew HusbyClick here to view the note

Powell said the Fed expects to wind up its strategic framework review in the middle of this year. The review, which was launched in 2019, is looking at everything from how the Fed communicates policy to the tools it uses to carry it out.

“We undertook the review because we felt and I felt that it was time to incorporate the realities of what you could call the new normal into our policy framework,” Powell said.

Those realities include “powerful global disinflationary trends” and “much lower” interest rates worldwide.

While saying he did not want to prejudge the review’s results, Powell said that a shift away from an approach of letting inflation bygones be bygones would also result in a change in the conduct of monetary policy.

“In effect they are setting the stage for the adoption of an average make-up inflation strategy,” said Kathleen Bostjancic, an economist at Oxford Economics in New York.

To contact the reporters on this story: Rich Miller in Washington at rmiller28@bloomberg.net;Christopher Condon in Washington at ccondon4@bloomberg.net;Matthew Boesler in New York at mboesler1@bloomberg.net

To contact the editors responsible for this story: Margaret Collins at mcollins45@bloomberg.net, Alister Bull, Ana Monteiro

©2020 Bloomberg L.P.