Powell Discovers Juggling Three Fed Communication Tools Is Hard

Confusion about Fed’s intentions -- were they hawkish or dovish? -- resulted from a mixed message and investors didn’t like it.

(Bloomberg) -- Jerome Powell, the Federal Reserve chairman who vowed to speak in “plain English,’’ is finding out just how vexing central-bank talk can be.

The problem that flared up for Powell this week is partly inherited. The Fed now speaks with an unwieldy information apparatus that’s challenged by turning points in policy and the economy. This week’s confusion about the Fed’s intentions -- were they hawkish or dovish? -- resulted from a mixed message and investors didn’t like it.

“It is difficult to communicate uncertainty, and a baseline” outlook, said Adam Posen, a former member of the Bank of England’s Monetary Policy Committee who now leads the Peterson Institute for International Economics in Washington. Saying you’re uncertain or that there are risks around that path can spook investors, Posen said: “It is never going to be perfect.”

Stocks tumbled into the worst decline for any Federal Open Market Committee announcement day since 2011. Asian stocks fell again on Friday and Japanese equities dropped deeper into a bear market.

Here’s a look at the Fed’s communication tools and how they worked or didn’t this week.

The Statement

The oldest form of FOMC decision-day communication, the group statement reflects the consensus view of what are currently 10 members who vote on monetary policy. A broader group of 17 FOMC participants discussed the outlook in the Fed’s boardroom this week. Achieving unanimity among diverse views requires brokering an agreement on words. The flimsier the deal, the fuzzier the words become.

On Wednesday, the statement’s first paragraph on the economic assessment changed very little from early November. It didn’t address the softening in inflation data and said price expectations were “little changed,” rather than acknowledging a decline.

After telegraphing in November’s meeting minutes that a reference to “further gradual increases” might come out of the statement, it showed up again with the addition of the ambiguous word “some’’ -- as in “some further gradual increases’’ -- in the policy rate. That language gave no sense of an approach more responsive to incoming information.

“‘Some’ does not describe one, and it probably doesn’t describe two,’’ said Andrew Levin, a former FOMC adviser on communication who is now a professor at Dartmouth College. “The statement could have been made more flexible and data dependent.’’

The statement also didn’t capture the sense of risk management Powell in particular had been trying to communicate. While there was a new nod to “global economic and financial developments,’’ the message was this had little bearing on the plan to keep hiking for now.

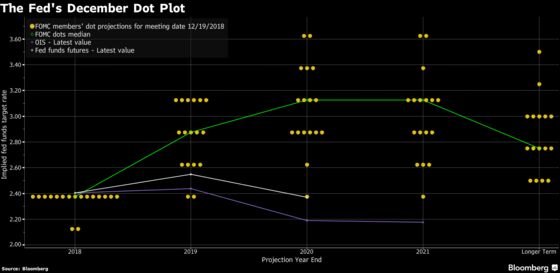

The Dot Plot

This is the policy forecast of all 17 participants. Financial markets focus on the median estimates, not the range. The median is simply a handy number to latch on to. That reinforces a baseline outlook but doesn’t get across a message about the diversity of views.

Even so, the dot plot may be in line with the language allowing for “some further gradual increases.” “Some” could cover the median projection for halting after three hikes in the next two years, or it could allow for the majority of participants who foresee either two or three hikes in 2019. But futures-market expectations were for one hike next year, at most.

The Press Conference

This offered a contrast between Powell’s opening statement -- which attempted to communicate the committee’s views -- and the questions from reporters, where he veered closer to his own.

In the opening remarks, Powell embraced the median path, citing two more increases forecast for 2019, and noted that committee’s projections still called for relatively strong growth and low unemployment. There was a nod to tighter financial conditions and weaker growth abroad adding headwinds for 2019, though not enough for the committee to deviate from continued hikes. However, he also cautioned that the median estimate on the rate path “certainly does not represent a committee plan.”

He hedged those views even more in the Q&A while coming off as more dovish.

For example, Powell said “there’s a fairly high degree of uncertainty about both the path and the ultimate destination of any further increases.”

Similarly, Powell said “inflation has continued to surprise to the downside.” That message could have been easily inserted in the economic update paragraph of the FOMC statement. It communicates risk about a central variable that is one leg of the Fed’s mandate.

“The statement seemed oblivious to reality,” Levin said.

In response to another question, Powell elaborated on data dependence. Once the policy rate is in the range of estimates of a rate that neither speeds up or slows the economy, “I think it’s appropriate to be putting aside individual estimates of that, and be looking at what the incoming data are telling you about the outlook.”

That expresses a lot more flexibility than either the statement or the forecasts communicated.

“The apparatus they have built up constrains the chair in terms of how much they can feel the market,” said Michael Feroli, chief U.S. economist at JPMorgan Chase & Co. in New York. “They could have been softer and gentler.”

To contact the reporter on this story: Craig Torres in Washington at ctorres3@bloomberg.net

To contact the editors responsible for this story: Alister Bull at abull7@bloomberg.net, Brendan Murray, Scott Lanman

©2018 Bloomberg L.P.