Post-Crisis ECB Considers How It'll Set Rates in the Future

Post-Crisis ECB Considers How It'll Set Interest Rates in Future

(Bloomberg) -- The European Central Bank is starting to consider whether the financial crisis changed forever the way it controls interest rates.

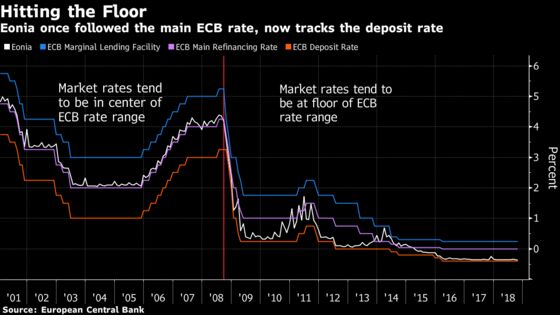

A decade of pumping cash into the financial system put so much downward pressure on market rates that all policy makers can do is set a floor -- the minus 0.4 percent they impose for holding banks’ deposits overnight. Like the U.S. Federal Reserve and Bank of England though, the ECB will need to weigh whether to revert to a system of controlling rates by keeping liquidity tight.

Core to the debate is whether central banks are better off with large balance sheets and far-reaching policy tools, or if they should scale back to avoid crimping money markets. The answers will likely have long-term ramifications for the credibility of monetary policy.

“The size of central-bank balance sheets will never be as it was before the crisis,” said Samy Chaar, chief economist at Lombard Odier in Geneva. “It’s pretty much a reality now.”

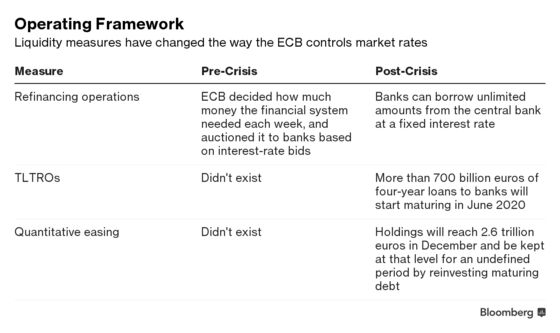

ECB staff are already reviewing the monetary-policy framework, according to euro-area officials familiar with the matter, who asked not to be identified because the work is confidential. A spokesman for the central bank declined to comment. Executive Board member Benoit Coeure said in a speech last month that the future framework is an important decision “that will need time and careful deliberations.”

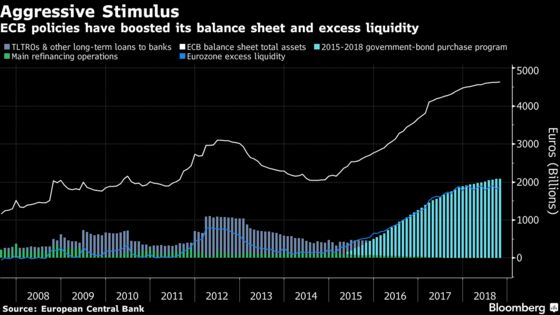

The ECB’s Governing Council starts a two-day meeting in Frankfurt on Wednesday to set policy. The explosion in liquidity from stimulus measures so far means there are now almost 2 trillion euros ($2.3 trillion) of excess reserves in the banking system, compared with effectively none before the crisis. The deposit facility sets a floor for market rates because it’s the safest place for lenders to park those excess funds overnight.

The ECB, Fed and BOE all previously used a corridor system -- so-called because the central bank would manage liquidity to keep short-term rates roughly in the middle of a defined corridor.

The BOE altered its framework in 2009 and now uses the same interest rate for overnight deposits and for its loans to banks.

The Fed switched to a “soggy floor” gradually after 2008. That’s because the large non-bank sector -- such as asset managers and government-backed mortgage financing agencies that can’t place money directly with the Fed --- pushed market rates lower than the Fed’s rate on excess reserves. Policy makers introduced another technical tool to soak up that liquidity.

That might be a model for the ECB to adopt once a new overnight lending rate takes effect in 2020, Rabobank analysts said Wednesday.

A key argument in favor of the rate floor is that it works with quantitative easing -- a tool that could well become a standard feature. Should central banks switch back to the corridor system after shrinking their balance sheets, they could find themselves reversing tack again in a future economic downturn, potentially damaging their credibility.

Fed Chair Jerome Powell has said he “sees the attraction” of keeping the floor, but also that he wants a renewed debate beginning this fall over how to manage rates in the longer term. William Dudley, before he stepped down as president of the New York Fed, said the argument for the floor is “very compelling.”

A counter-argument was put forward in a 2016 paper by Ulrich Bindseil, the ECB’s director general for market operations, who noted that prolonged use of the floor system comes with excess liquidity that can mute lending between banks.

“A lean balance sheet is a sign of well‐functioning financial markets and a healthy economy because the central bank is neither used as intermediary by the banking system, nor does the central bank see a need to engage in special crisis measures,” he wrote.

There’s no need to rush to a decision. As long as excess liquidity remains high -- which could be years as the ECB gradually pares back stimulus -- market rates will remain largely anchored to the deposit rate.

“The main refinancing operations rate becomes relevant again when the level of excess liquidity is around 250-300 billion euros,” said Aila Mihr, an analyst at Danske Bank. “Our view is that that’s not going to be reached anytime soon before 2025-26.”

--With assistance from Lorcan Roche Kelly, Christopher Condon and Alessandro Speciale.

To contact the reporter on this story: Carolynn Look in London at clook4@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, Jana Randow

©2018 Bloomberg L.P.