PGIM’s Tipp Sees 10-Year Yield Falling to 1% Once Stimulus Fades

PGIM’s Tipp Sees 10-Year Yield Falling to 1% Once Stimulus Fades

(Bloomberg) -- The bond-market selloff that’s jolted Treasury yields higher is bound to run out of steam as the effects of fiscal stimulus wear off, eventually driving 10-year rates back down to 1%, says PGIM Fixed Income’s Robert Tipp.

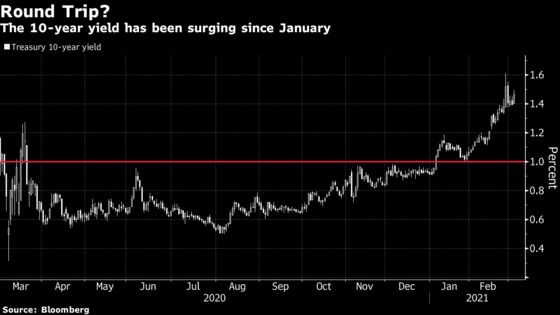

A rush out of Treasuries pushed 10-year yields above 1.6% last week for the first time since February 2020 as global reflation wagers revved up and traders pulled forward bets on when the Federal Reserve will lift rates from near zero. Optimism over vaccinations and further U.S. economic relief renewed that momentum Wednesday, pushing the benchmark rate to just below 1.5%. It was around 1.46% in New York morning trading Thursday.

For Tipp, chief investment strategist and head of global bonds for the money manager, which oversees about $968 billion, it’s all gone too far, too fast. In his view, investors aren’t considering that the tailwind from any additional stimulus package and infrastructure spending will fade. He expects the economy will end up in a more sluggish state than at the end of 2019, before the pandemic even struck, because of structural issues such as a shrinking workforce.

“As growth drops off next year, it’s going to become clear that the Fed is not going to be hiking as rapidly as what’s priced into the forward curve, if at all, maybe for the next handful of years,” Tipp said in an interview. “Once you’ve gone through all of the stimulus and you’ve gotten the long-term infrastructure package done, if you’re not achieving the inflation target, then the rationale for hiking rates” could be gone.

Tipp makes it clear that he doesn’t expect a straight shot back down to 1% -- a level last seen in January. The economy could experience a “twin peaks situation,” he said: It would get a boost from the relief package that’s in the works, then go through a lull until other stimulus measures, such as an infrastructure spending plan that could exceed $2 trillion, provide another jolt.

“Before we get to the part where we’re going back down to 1%, we have to go through the part where you get an absolute peak in optimism about the strength of the recovery,” he said.

Year-End Timing

Tipp is one of the managers on the PGIM Total Return Bond Fund, which has about $62 billion in assets and has generated essentially a flat return over the past year, beating around 7% of peers, data compiled by Bloomberg show. It’s outpaced about 71% of competitors on a three-year basis, averaging a 5.62% annual return.

In Tipp’s view, it “could very well be by the end of this year” that the market returns to 1%.

The Fed’s willingness to let inflation overshoot its 2% goal so it averages that level over time will play a role, as it will “have to guide rates back down” if officials are serious about that target. The Fed could do so by continuing to provide forward guidance assuring markets that hikes will be on hold until the goal is met, he said. The central bank has struggled to achieve that inflation target.

In the market for eurodollar futures and swaps, traders are now pricing in a full quarter-point Fed hike in the first quarter of 2023. The Fed itself has signaled it intends to keep policy steady at least through the end of that year.

False Dawns

Of course, the market may drive rates back down without Fed guidance if economic data disappoint, or if there’s a setback in terms of the pandemic. There have been several false dawns for a break higher in yields in the past year, raising the possibility that obstacles to a sustained climb remain.

After the latest turmoil in Treasuries, a speech Thursday by Fed Chair Jerome Powell is the next big event for investors, for any sense of pushback on the runup in yields. There’s also Friday’s report on February payrolls, which will be in focus after a weak January release.

Investors banking on further government spending have been lifting their outlook for price pressures. On Wednesday, a market proxy for the anticipated annual inflation rate for the next half-decade exceeded 2.5% for the first time since 2008. The 10-year Treasury yield has risen more than a half-percentage point in 2021, an increase that’s started to weigh on stocks.

In the meantime, Tipp is watching for the crest in yields, saying it may have already happened and that he’d be “surprised” to see the 10-year exceed 2%.

“The market would have to be convinced that you’re going back to a world of higher growth and inflation that you had pre-Covid on a sustained basis,” he said. That sounds “too extreme” even “for a market running away on irrational exuberance.”

©2021 Bloomberg L.P.