PBOC’s Cash Injection Disappoints Stock Traders Wanting More

Beijing is providing just about enough cash at a time when banks are expected to help corporate clients pay taxes.

(Bloomberg) -- The People’s Bank of China signaled its intention to contain rising leverage by adding just enough cash to maintain medium-term liquidity. Stocks fell as expectations that the central bank would loosen its purse string were dashed.

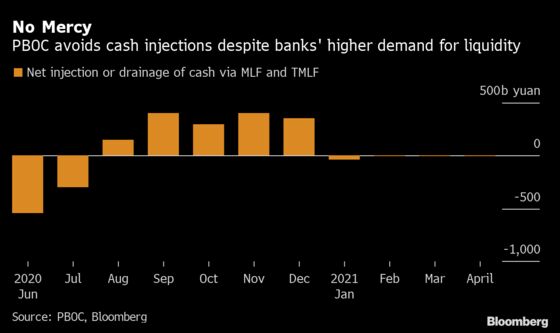

The PBOC injected 150 billion yuan ($23 billion) into the financial system on Thursday with its medium-term lending facility. That more-or-less matches the 100 billion yuan due and 56.1 billion yuan of targeted loans maturing on April 25.

While money markets barely reacted, the decline in stocks showed how equity traders are struggling to come to terms with plans by Chinese policy makers to gradually wind back pandemic-fueled stimulus. The test for the economy will come in the weeks ahead as banks need to help corporate clients pay taxes, and as sales of government bonds are forecast to accelerate.

“The expectation in the market is that the central bank will gradually tighten its liquidity as it seeks policy normalization after the pandemic,” said Zhang Gang, a strategist at Central China Securities Co.

The PBOC withdrew a net 40.5 billion yuan of one-year funds in the first quarter, as policy makers address the twin challenge of a buildup in leverage while supporting the economic recovery from the pandemic. The tightening ricocheted through markets, with the main equity gauge falling from the highest in more than a decade while the benchmark money-market rate jumped to a three-year high in February.

The benchmark CSI 300 Index closed 0.6% weaker, paring earlier losses while still underperforming the MSCI AC Asia Pacific Index. Liquor giants Kweichow Moutai Co. and Wuliangye Yibin Co., which are favored by institutional investors, were the two biggest drags on the index. The seven-day repurchase rate -- a gauge of interbank funding costs -- was little changed at 2.03%.

‘Bit Disappointing’

The PBOC’s stance on Thursday suggests it isn’t concerned about possible contagion from the recent credit stress engulfing China Huarong Asset Management Co., one of the nation’s largest distressed-debt managers.

Chinese policy makers have always been cautious about rapid increases in leverage. In 2017, the PBOC guided money rates higher, driving the benchmark 10-year yield to a three-year high, after low borrowing costs spurred a surge in property prices.

The government has said it aims to keep macro leverage “basically stable” in 2021, after the country’s debt-to-GDP ratio soared to a record 279% late last year following a series of stimulus measures deployed to blunt the virus impact.

The central bank’s operation Thursday “is a bit disappointing to the bond market and funding costs will rise,” said Xing Zhaopeng, senior China strategist at Australia & New Zealand Banking Group Ltd. in Shanghai. The PBOC is likely to add more cash through seven-day reverse-repurchase agreements to plug the liquidity gap as the tax payment season starts later this month, he said.

To be sure, banks aren’t suffering from a severe shortage in cash. The seven-day repurchase rate is close to its average level for the past year, and the 10-year sovereign bond yield is near its lowest level in more than two months. Of the analysts surveyed by Bloomberg, two had forecast a neutral stance from the PBOC, with the third seeing a gross injection of 150 billion yuan to 200 billion yuan.

The PBOC looks to be phasing out the usage of targeted loans, and is instead focusing on other policy tools to support small firms, according to Tommy Xie, head of Greater China research at Oversea-Chinese Banking Corp. in Singapore.

| Read more about China’s financial markets here: |

|---|

| Few Signs of Huarong Contagion Onshore: What to Watch in China |

| What to Watch for in China’s Unprecedented GDP Growth Report |

| China’s Epic Battle With Capital Flows Is More Intense Than Ever |

| China Tests Banks With the Longest Cash Drought in 10 Months (2) |

©2021 Bloomberg L.P.

With assistance from Bloomberg