Party Might Not Be Over for the Best Chinese Proxy: Taking Stock

Party Might Not Be Over for the Best Chinese Proxy: Taking Stock

(Bloomberg) -- Some may question the strength of the stock rally and fear volatility, but signs of economic stability in China favor the sector most exposed to that nation: miners. Strategists at Credit Suisse just upgraded the industry to overweight and make points worth hearing.

China is key and accounts for about half of global copper demand, and more than 60 percent of iron ore consumption. Historically, mining stocks outperform one to three months after Chinese purchasing managers’ index data turns, according to Credit Suisse.

And yes, China’s manufacturing activity picked up and returned to positive territory last month, amid strong domestic demand, falling inventories and stabilizing monetary policy. The country has also started to implement stimulus to support the economy, and the effects might materialize in the very near future. In fact, copper prices are already bouncing.

But that’s not all. Monetary policy could also play a part. The dovish Fed is weighing on the dollar, which is supportive of commodity prices. In addition, Credit Suisse found out that miners are one of the best-performing sectors following a yield curve inversion, and beat the market 80 percent of the time when that happens.

Valuation-wise, the sector doesn’t look pricey, hovering just above a 10 times price-to-earnings ratio, and offering one of the best dividend yields in the market. Miners have cleaned up their balance sheets to become one of the least-leveraged sectors in Europe and have focused on shareholders’ returns.

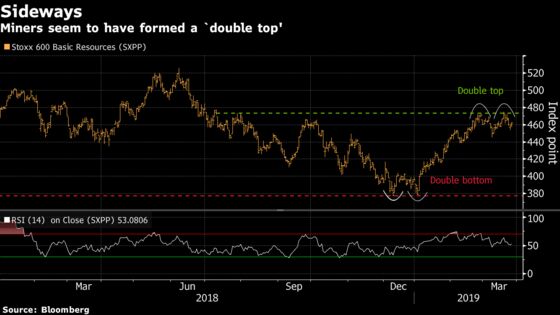

So what could spoil the party? The obvious thing would be a negative switch in macro data, triggering a slump in metal demand and commodities prices. Some weakness can’t be ruled out, especially if you look at technicals, as the SXPP seems to have formed a double top. It’s also worth keeping an eye on the pound’s strength, as most miners are U.K.-listed, and Brexit news seen as positive by the market could limit the upside for large caps.

Still, further voices came out this week to support the miners. Morgan Stanley believes the sector is still attractive, citing reasonable absolute and relative valuation levels, low leverage and metal spot prices supporting earnings-per-share upgrades. In term of single names, they prefer Anglo American, Glencore, Lundin Mining and Norsk Hydro, while Credit Suisse has Norsk Hydro and Glencore as their only overweight plays.

Ahead of speeches from ECB President Mario Draghi and other central bank representatives, Euro Stoxx 50 futures are trading up 0.4%.

SECTORS IN FOCUS TODAY:

- Watch European autos after a report that Renault is seeking to restart merger talks with Nissan as a first step towards eventually making a joint offer for Fiat Chrysler. Watch Volkswagen, BMW, Daimler and Peugeot for reaction to the news.

- Watch European Boeing suppliers after a 737 Max aircraft, which did not have any passengers on board, had to make an emergency landing in Florida on Tuesday due to engine trouble. Watch Safran, Senior, Rolls-Royce, Leonardo, Meggitt, Melrose Industries, Thales and BAE Systems.

- Watch oil and oil companies as crude is on course for its best quarterly gain since 2009, with the latest jump coming after Russian Energy Minister Alexander Novak told reporters that the country will likely reach its pledged output cut of 228,000 barrels a day by the end of the month. All eyes will be on weekly U.S. inventory data this afternoon.

- Watch the pound and U.K. stocks as the House of Commons will attempt to break the deadlock on Wednesday with votes on alternatives to Prime Minister Theresa May’s divorce deal with the European Union. One positive for May is her deal is slowly getting more support from hardliners. More details of how this is going to play on this handy graphic.

- Watch the lira and Turkish stocks after Turkey has made it virtually impossible for foreign investors to sell the lira, averting a currency slide that might have dealt a blow to President Recep Tayyip Erdogan before local elections this weekend.

COMMENT:

- “Despite Europe’s low economic growth and negative bond yields, we don’t see it succumbing to the kind of deflation trap that befell Japan in the late 1990s,” Bloomberg Intelligence strategists Laurent Douillet and Tim Craighead write in a note. “But European equities, up 18% from the lows of December, are also unlikely to repeat their surge of 2Q16, the last time European bond yields were negative.”

COMPANY NEWS AND M&A:

- Renault Seeks to Restart Merger Discussions With Nissan: FT (1)

- Nissan Plans to Cut 600 Jobs in Barcelona, Expansion Reports

- Swedbank May Have Misled U.S. Investigators, Sweden’s SVT Says

- Electrolux Reiterates Business Outlook for 2019 Ahead of CMD

- Carrefour in Talks W/ French Unions to Cut 1,500 Jobs: Figaro

- Lawmaker Wants Intelsat to Share Airwaves Sale Payout With U.S.

- Novartis’s Multiple Sclerosis Tablet Mayzent Approved by FDA (1)

- Steinhoff Raises 4.8b Rand Through Placement of KAP Shares

- Daimler Nears Geely Deal Over Stake in Small-Car Smart Unit: FT

- China Cancels Glencore Canada Canola Permit Amid Trade Spat

- Glencore in Debt Extension, Warrants Pact With PolyMet Mining

- Poland’s PKO Has Appetite for Foreign Expansion, CEO Tells Puls

- Neopost Expects Organic Sales to Be ‘Almost Flat’ This Year

- Jyske Bank Says Board Will Work to Start New Buyback Program

- Orpea Full Year Ebitda Meets Estimates

- Cromwell Confirms Approach to U.K.’s RDI REIT, Talks Ongoing

- Hamburger Hafen Sees Further Growth in 2019, Raises Dividend

- Telenor offered 100m Veon common shares priced at $2.16/ads. Net proceeds of about $213m to be included in Q1 cash flow

NOTES FROM THE SELL SIDE:

- Citi raised Pets at Home to buy, saying the company now has a “viable plan” for a business turnaround, helped by market dynamics and company initiatives after the veterinary strategy update. Citi said those positives could drive Ebit growth, estimated at +14% CAGR FY18-21. Price target is 180p.

- Citi says investors may be getting ahead of themselves by sending Wirecard’s stock 26% higher on Tuesday after the company said irregularities in Singapore have no material financial impact. Broker reiterates its sell rating as “significant uncertainties still remain,” including the ongoing Singaporean police investigations, which seem to have widened to include Wirecard subsidiaries in other countries such as India.

- Jefferies believes a lack of margin progress at Inditex poses concerns, even if total shareholder returns have been given a boost, downgrading the shares to hold from buy and cutting its PT to EU27 from EU32.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 379.9 (23.6% Fibo); 382.5 (trend line)

- Support at 369.1 (200-DMA); 365.1 (38.2% Fibo)

- RSI: 56

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,422 (March high); 3,466 (23.6% Fibo)

- Support at 3,315 (38.2% Fibo); 3,277 (200-DMA)

- RSI: 53.3

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Barry Callebaut upgraded to buy at Goldman; PT 2,100 Francs

- Ferguson upgraded to overweight at JPMorgan; PT 59.50 Pounds

- Greencoat Renewables raised to outperform at RBC; PT 1.20 Euros

- Nordex upgraded to add at AlphaValue

- Pets at Home upgraded to buy at Citi

- Tecnicas Reunidas raised to overweight at JPMorgan

DOWNGRADES:

- Axa downgraded to add at AlphaValue

- Chr. Hansen cut to sell at DNB Markets; Price Target 670 Kroner

- EMS-Chemie downgraded to sell at Baader Helvea; PT 485 Francs

- EON downgraded to neutral at Oddo BHF; PT 10.70 Euros

- Enagas downgraded to sell at SocGen; PT 19.50 Euros

- Gem Diamonds downgraded to hold at Berenberg

- Inditex downgraded to hold at Jefferies; PT 27 Euros

INITIATIONS:

- Bureau Veritas rated new sector perform at RBC; PT 20 Euros

- Kering rated new outperform at Mediobanca SpA; PT 600 Euros

- Klingelnberg rated new neutral at MainFirst; PT 40 Francs

MARKETS:

- MSCI Asia Pacific up 1%, Nikkei 225 down 0.2%

- S&P 500 up 0.7%, Dow up 0.6%, Nasdaq up 0.7%

- Euro down 0.03% at $1.1263

- Dollar Index up 0.14% at 96.87

- Yen up 0.1% at 110.53

- Brent up 0.3% at $68.2/bbl, WTI up 0.1% to $60/bbl

- LME 3m Copper up 0.3% at $6347/MT

- Gold spot up 0.1% at $1316.7/oz

- US 10Yr yield down 2bps at 2.41%

MAIN MACRO DATA (all times CET):

- 8:45am: (FR) Feb. PPI MoM, prior 0.1%

- 8:45am: (FR) Feb. PPI YoY, prior 1.4%

- 8:45am: (FR) March Consumer Confidence, est. 96, prior 95

- 9am: (SP) Jan. House Mortgage Approvals YoY, prior 0.9%

- 9am: (SP) Jan. Total Mortgage Lending YoY, prior 23.1%

- 10am: (IT) March Consumer Confidence Index, est. 112.5, prior 112.4

- 10am: (IT) March Manufacturing Confidence, est. 101.4, prior 101.7

- 10am: (IT) March Economic Sentiment, prior 98.3

- 12pm: (UK) March CBI Retailing Reported Sales, est. 4, prior 0

- 12pm: (UK) March CBI Total Dist. Reported Sales, prior 14

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.