(Bloomberg Opinion) -- It was all looking so promising.

In September central banks in some key emerging markets were, for once, mostly in tune. Controlling inflation and offering stability were the order of the day. Currencies responded well, offering a positive return and a respite during a tough year. But that good performance is coming undone.

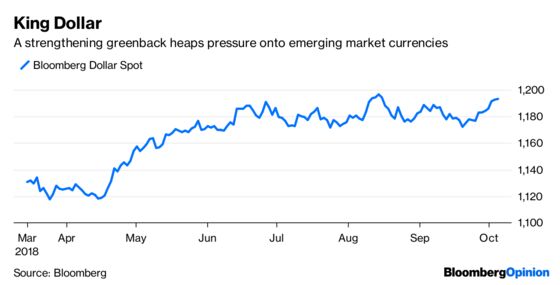

But that was all last month, and the dollar rules once again. The U.S. economy is powering ahead, so the momentum behind the greenback looks substantial.

U.S. unemployment, at 3.7 percent, is the lowest since 1969. Ten-year Treasury yields closed Friday at 3.23 percent, the highest since 2011.

And the upward march in oil prices is relentless — they’ve gained 25 percent so far this year.

These are powerful forces. And, compounding the problem, the domestic issues afflicting the some of these nations are getting worse.

Turkey’s September inflation data showed that the central bank has acted too late, and price gains are out of control. The core rate is at a record 24 percent, and producer prices are nearly double that. Policy makers will have to tighten further if they are to fulfill their mandate, it’s an open question whether President Recep Tayyip Erdogan will allow it. Meanwhile, the economy is imploding.

Russia’s spying and hacking raise the risk of further sanctions, particularly from the European Union. International condemnation of its activities abroad is increasingly offsetting the substantial benefit it should be receiving as a major oil exporter, a source of support many emerging economies don’t have.

The South African rand’s slump partly reflects investor fears of fiscal slippage at the medium-term budget statement on Oct. 24. It worsened Monday after Business Day reported that Finance Minister Nhlanhla Nene has asked to resign after he disclosed links to the Gupta family, who have been implicated in a corruption scandal involving former President Jacob Zuma.

Disappointingly, not all policy makers are getting the message. India’s central bank surprised on Friday by leaving rates unchanged in the face of investor expectations for an increase to support the currency and tame persistently high core inflation. The rupee sank to a record low against the dollar as a result.

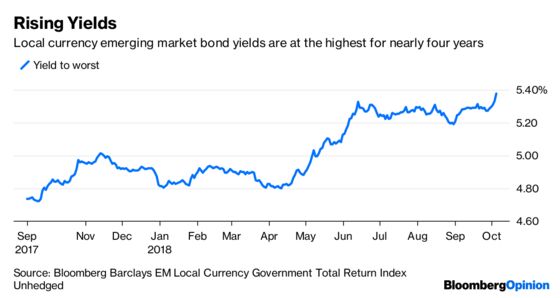

So, bond yields are rising across emerging markets as a whole.

Not all countries are looking so grim this month. Argentina’s peso is the best performer among major emerging markets so far, now that the International Monetary Fund has improved terms on its bailout. In second place is Brazil, but the outlook for the real is difficult to call since the country is in the midst of a presidential election that could produce a substantial change of policy direction.

Otherwise, it is hard to see how the weakest emerging market currencies this year can recover their glory days of September unless there is significant improvement in resolving domestic problems. And even then, with the U.S. economy roaring away, it’ll be a stretch.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2018 Bloomberg L.P.