Saudis See Need to Cut Oil Output by 1 Million Barrels a Day

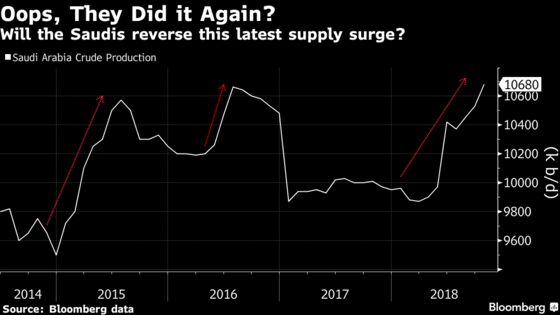

Saudi Arabia will export 500,000 fewer barrels a day in December than this month.

(Bloomberg) -- Saudi Arabia expressed the need for oil producers to cut 1 million barrels a day from October levels and announced fewer shipments from next month, as OPEC and its allies began laying the groundwork to reduce oil supply in 2019, reversing an almost year-long expansion.

Saudi Energy will export 500,000 fewer barrels a day in December than this month, taking the lead in OPEC to counter the price rout battering the finances of group members and energy companies alike. While a meeting with other producers on Sunday yielded no change in supply policy, OPEC+ warned in a statement that it might need “new strategies,” raising the prospect of a wider and coordinated cut in 2019.

“We are going to do everything we can to keep inventories and supply demand fundamentals within a reasonably narrow band around balance, and we believe markets will calm down,” Saudi Energy Minister Khalid Al-Falih said Monday in a speech at an industry event in Abu Dhabi. “We are not in the business of pinpointing a price going forward.”

Oil collapsed into a bear market in little more than a month, and pressure is mounting on the OPEC+ group to act sooner than their policy meeting in December. The producers need prices that are high enough to balance their budgets and low enough to stimulate demand and shield themselves from attacks from the White House, all while they contend with wild swings in supply as sanctions hit OPEC member Iran.

Although there are signs of a glut emerging in the U.S., the Saudi minister said Sunday it was too early to talk about coordinated production cuts within OPEC+. Counterparts from Russia and the United Arab Emirates echoed that sentiment. Oman, a smaller member of the group, had said earlier it would support a cut by consensus of 1 million barrels a day.

Iranian Losses

The group’s caution arises partly from the unpredictability of Iranian supply. The U.S. at first insisted it would seek to curtail all of the country’s exports, only to grant waivers to eight of its customers just as Washington reimposed sanctions this month. That confounded a market that was anticipating a stricter enforcement.

“With Iranian waivers coming in higher than anyone expected, Saudi Arabia is acting responsibly by reducing its production that it had earlier brought online to offset possible Iranian losses,” said Amrita Sen, chief oil analyst at Energy Aspects Ltd, a consultant in London.

The committee that oversees the 2016 OPEC+ agreement to manage supply met Sunday in Abu Dhabi. “The committee reviewed current oil supply and demand fundamentals and noted that 2019 prospects point to higher supply growth than global requirements,” it said in a statement. Weaker global economic growth “could lead to widening the gap between supply and demand.”

“OPEC+ nations sent a clear signal they are concerned rising supply and weaker demand may keep pushing oil prices down,” said Jason Bordoff, director of the Center on Global Energy Policy at Columbia University in New York. “While Saudi Arabia is cutting back output in December, the group may wait to see how Iranian supply and other variables play out before it is able to agree on collective action to prop up prices.”

Oil Prices

Brent crude, the global benchmark, rose 1.2 percent to $70.99 a barrel at 10:55 a.m. Singapore time. Futures are still down about 18 percent from a 2014 high reached early last month. West Texas Intermediate, the U.S. marker, climbed 0.9 percent to $60.75, paring its losses after falling into a bear market last week.

While current crude prices are still higher than a year ago, they’re well below what Saudi Arabia needs to balance its budget. Russia, by contrast, is in a more comfortable position, and Energy Minister Alexander Novak showed no sign he was ready to act immediately. The market should be balanced by the middle of next year, though there are forecasts for a surplus of 1 million to 1.4 million barrels a day, he said.

“I think it all comes down to Russia,” said Helima Croft, chief commodities strategist at RBC Capital Market LLC. “They seem to be sitting squarely on the fence about pulling the barrels back.”

Saudi Arabia may also struggle to convince other producers to follow its lead. Iraq has successfully boosted production to a record, and its more fragile economy may make it loathe to reverse course.

Al-Falih said that demand for Saudi crude was weaker for the first time since the kingdom started boosting production in the May-June period. If Riyadh reduces daily exports by 500,000 barrels next month, it would effectively wipe out most of the production increases of the last six months. Saudi Arabia will cut production as well as exports, he said.

“Ideally, we don’t like to cut,” Al-Falih said. “We will only cut if we see a persistent supply glut emerging, quite frankly. We’re seeing some signs of this coming out of the U.S. We have not seen the signs globally, nor can we predict that they will persist into 2019.”

Russia’s Novak said it’s “hard to say” if oil markets will be over-supplied next year. “We need to wait some time, to see how the market develops,” he told reporters. Russia is currently pumping about 10,000 to 20,000 barrels a day below October levels, and demand from customers is “fairly stable,” Novak said.

--With assistance from Manus Cranny, Hussein Slim, Giovanni Prati, Sarah Forster, Javier Blas and Elena Mazneva.

To contact the reporters on this story: Grant Smith in London at gsmith52@bloomberg.net;Anthony DiPaola in Dubai at adipaola@bloomberg.net;Mohammed Aly Sergie in Dubai at msergie@bloomberg.net;Mahmoud Habboush in Abu Dhabi at mhabboush@bloomberg.net

To contact the editors responsible for this story: Nayla Razzouk at nrazzouk2@bloomberg.net, Bruce Stanley, Shaji Mathew

©2018 Bloomberg L.P.